TRADE IDEAS: Long UKT 1T 37s into Tap w/Charts

Ø The UKT 1T 37s will be tapped Thursday for the last time this fiscal year. They will surely be tapped again in Q2 '18 but lots of wood to chop before then. o The issue has lagged the flattening move in the sector. o BoE holdings of the UKT 1T 37s are currently zero while UKT 4Q 32s holdings are 72% (ineligible now), 4T 38s 53% and 4H 42s 37%. One would assume the BoE will be targeting the 37s during the March APF UKT 5 18s reinvestments. o In this morning's MACROCOSM note entitled "Laying the Groundwork for UK Rates in 2018", we highlighted the risk that the start of 2018 will look a lot like H2 2017 - relatively low volatility with range trading, a general flattening curve bias and flat/long gilts directionally. Discussions with clients reveal flatteners are already popular trades and, while some may be looking to add if they can find an issue that has 'missed the boat', they'd also consider lightening up on their flatteners if a compelling steepener arose. So, at the risk of appearing indecisive, we'll take a look at both options below. These are 'micro' trades - if you prefer something more macro pls let me know.

Ø FLATTENERS: o Long UKT 1T 37 vs UKT 4Q 32 and UKT 4H 42 at +20.4bps, targeting 18bps, stop at 21.5bps. With the short leg around 22.4bps and the long leg 1.7bps, this butterfly is clearly a flattener in disguise. The reason we like the fly is it carries better than the naked flattener out of 32s into 37s (which looks interesting on its own). This is one of the few flatteners in the sector that hasn't made a new low since the start of '18.

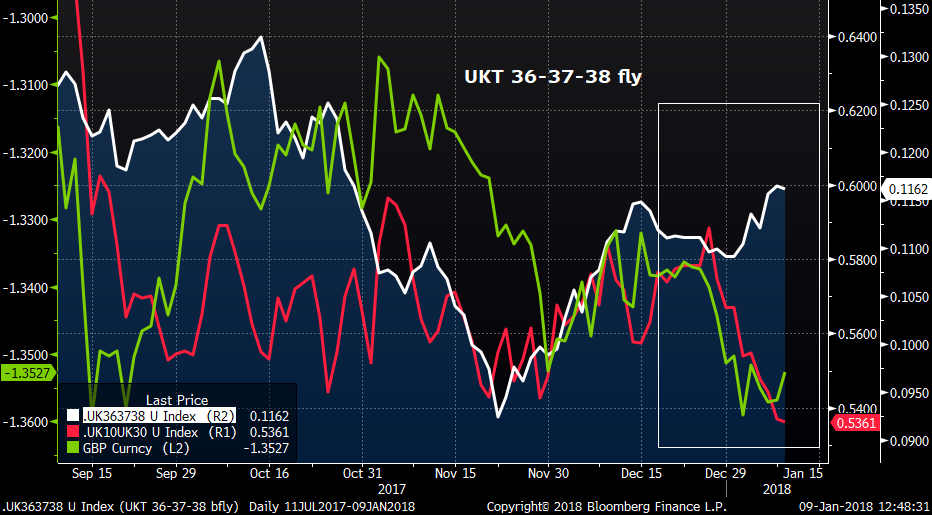

o Long UKT 1T 37 vs UKT 4Q 36 and UKT 4T 38 at +11.1bps, targeting 9bps, stop at 12bps. The 36-37s leg of this fly has lagged the move on the curve, still about .5bp steeper than the range lows. The 37-38s leg has flattened 2bps since early Dec, exaggerating the cheapening of the 37s on the fly. Carry and roll is a touch negative on the fly but the dislocation below looks compelling enough for us to live with that.

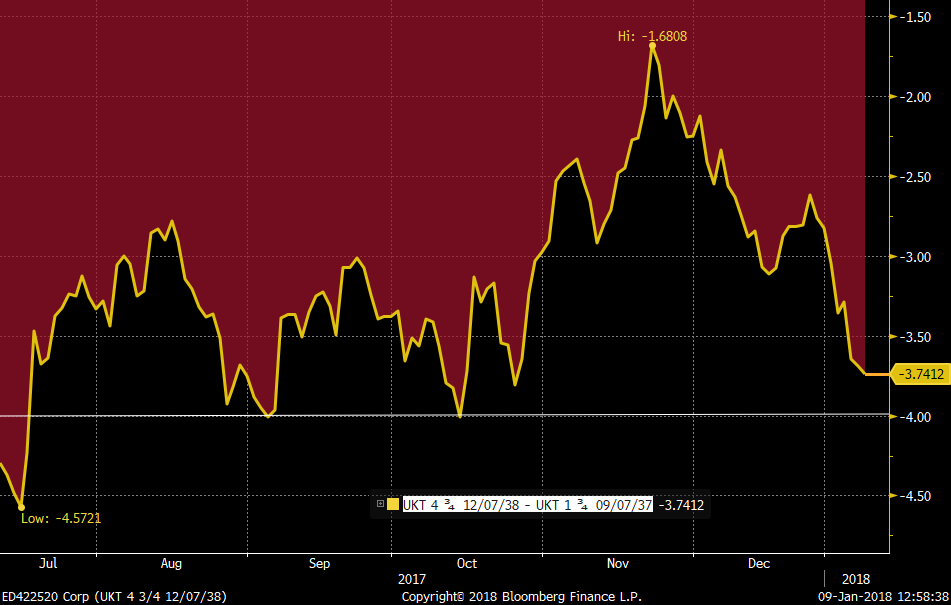

Ø STEEPENER: o Buy UKT 1T 37 vs UKT 4T 38s at +3.5bps, targeting +2bps, stop +4.5bps. This is a micro trade that has richened back near levels that have held since July on both yield and Z-spread. Carry and roll is flat.

I'll be in touch to discuss.

Thanks,

Mark

image009.jpg@01D28D1B.42BD95C0"/>

Mark Funsch

O: +44 (0) 207 - 002 - 1347 M: +44 (0) 789 - 996 - 4051 E: Mark.Funsch@AstorRidge.com<mailto:Mark.Funsch@AstorRidge.com> W: www.AstorRidge.com

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission's Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287 Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185 Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626 Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303 Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

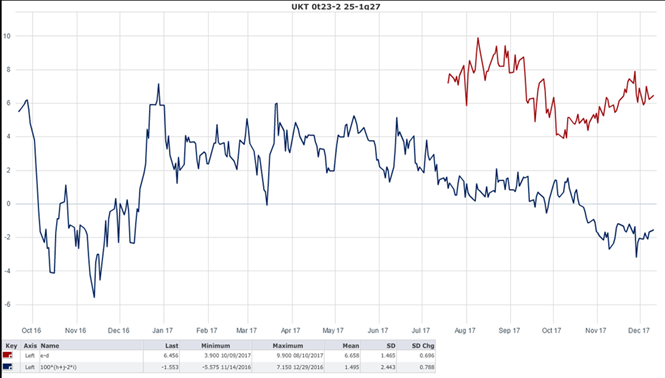

UKT T 23 - 2 25 - 1Q27 fly - Wings are cheap

Subject: UKT T 23 - 2 25 - 1Q27 fly - Wings are cheap

An interesting way to capture the benchmark premium on the UKT 0T23s and 1Q27 from John; this is achieved by hedging them with 7yr bullet (2% 2/25).

With a new 10yr benchmark in March, the 1Q27 should richen to the curve as it approaches its last official tap in January. Similarly, the 0T23, despite taps in Jan and March, should perform into the £35bn UKT 5 3/18 redemption on March 7th.

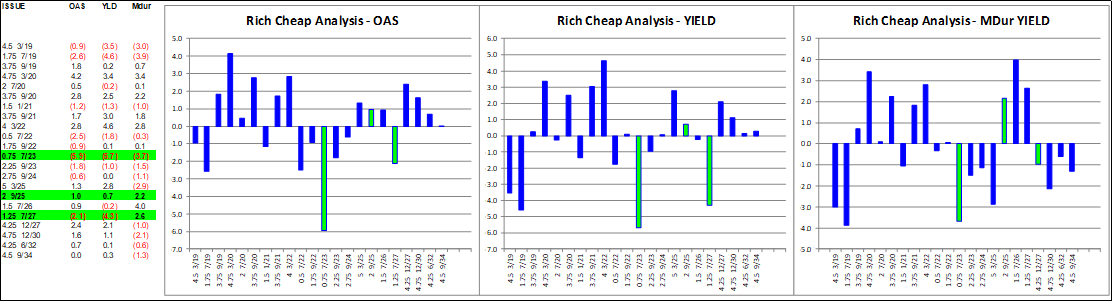

Note: John is quoting the fly via wings (not belly), i.e. to buy wings of 0T23-2’25-1Q27 @ +6.5 bps = Sell belly at -6.5 bps. This fly rolls to 0H22-2T24-1H26 = +2.3 bps (belly cheap), for total roll of 8.8 bps. Similarly, the UKT CMS 5s7s9s fly below is quoted vs wings, i.e. the belly is 2 bps cheap.

For those with dyslexia, please disregard note above 😊

==============================================================================================================================

I like buying the UKT current 5y and 10y verse the belly (it is the 5-7-9 fly): This is the kind of position we do 1/3 at 6.5bp, 1/3 at 7bp, and 1/3 at 7.5bp.

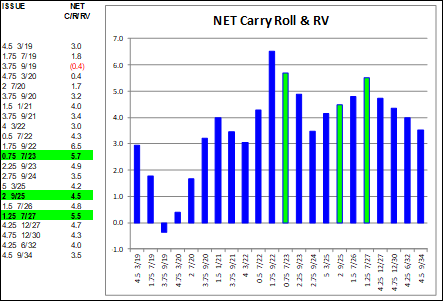

This is where it rolls to:

This is a graph of the current fly and the 1 year old fly. I like the location to get a position started, and I really like that it is cheaper now than the last fly has ever been.

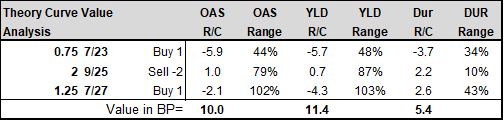

It looks very good on the Theoretical curve:

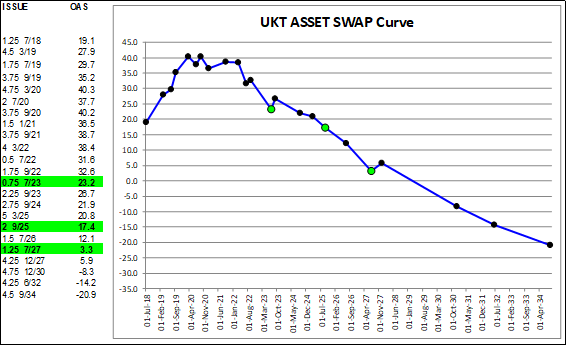

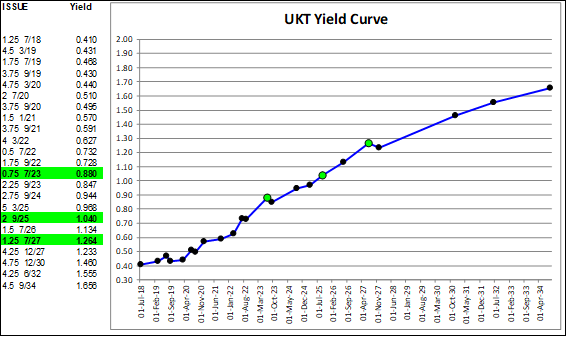

Here are the bonds highlighted on the Yield and OAS curves.

John Wentzell CEO / Founding Partner image009.jpg@01D28D1B.42BD95C0"/> O: +44 (0) 207 - 002 - 1344 M: +44 (0) 779 - 505 - 0313 E: John.Wentzell@AstorRidge.com<mailto:John.Wentzell@AstorRidge.com> W: www.AstorRidge.com UK: 60 Cannon Street, London, EC4N 6NP US: 245 Park Ave, 39th Floor, NY, NY, 10167

This marketing was prepared by John Wentzell. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a research recommendation. John is a Partner and CEO of Astor Ridge. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287 Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185 Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626 Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303 Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Trades for 2018: Long Bund spreads vs Buxls

Subject: Trades for 2018: Long Bund spreads vs Buxls

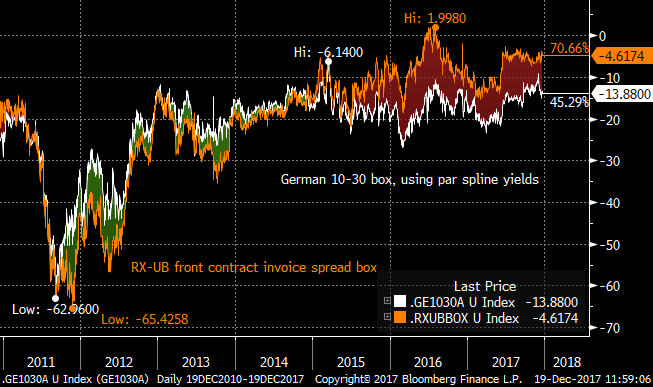

Re-send with improved PSPP2 buying chart (y-axis visibile!) Bottom line: German supply, and the stock available for PSPP2 purchasing should favour 10y over 30y and drive a steepening move in Bunds. At the same time, the 10-30 flattening in swaps has room to move further. Put together this suggests a 10y/30y box trade: buying 10y spreads vs 30y. Finally, being long RX spreads is something of an insurance play should either the Catalonia or Italian elections create uncertainty for the EU project.

Trade: Buy EUR 100k/bp RXH8 invoice spread Sell EUR 100k/bp UBH8 invoice spread Entry at -4.5 bp

Essentially flat carry/roll.

Rationale: Germany 30y paper is trading close to its richest levels vs 10y. The chart shows two expressions: the headline box of invoice spreads (RX vs UB) in orange, and the same box but using Bloomberg's par spline yields and 10y and 30y vanilla swap rates. This latter series takes out some of the roll anomalies as the contract CTD changes.

On these measures, Buxls are around 2-3bp off their richest levels of the past year. In January, the ECB cuts its PSPP2 purchasing amounts by 50% to 30bn. Comments from the "Northern European" block of ECB governors suggest that the extending new purchases beyond September (as opposed to principal reinvestment flows) will face stiff opposition. The PSPP2 programme has supported the long end of the curve, and allowed sovereigns to tap in that sector. The most recent German supply calendar is suggesting 16bn of 30y issuance in 2018, compared to 11bn in 2017, with the decision to tap the off-the-run 44s and 46s raising a few eyebrows.

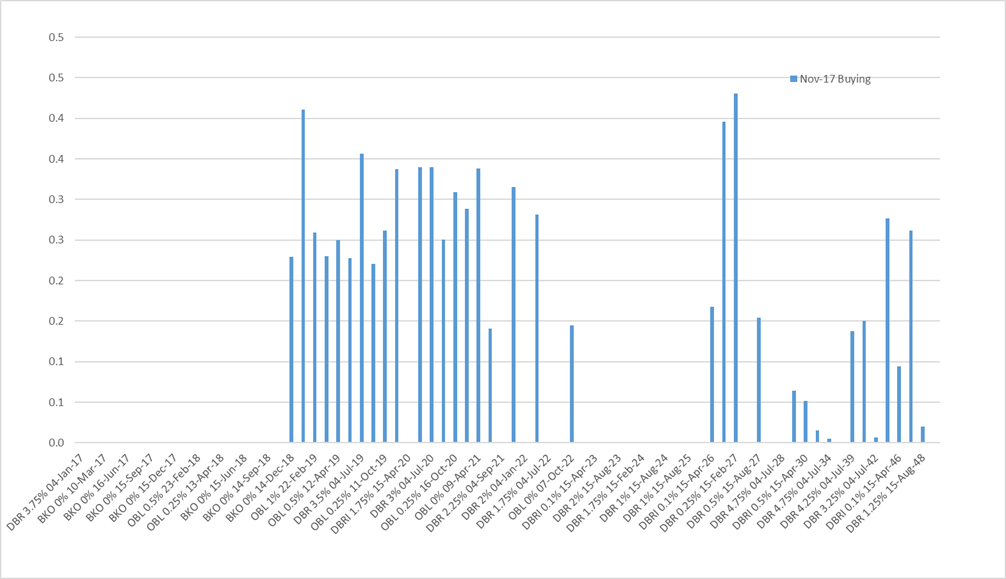

My PSPP2 model suggests that the Bundesbank has already purchased all, or nearly all of the 2042 paper available to it, so it is unclear that that particular issue (CTD in UBH8) can benefit much from purchasing for the next nine months. In contrast, I estimate the Buba bought 400mm of the Feb 2027 (CTD into RXH8) in November and still has over 6bn available for buying. Thus in the early months of 2018 I expect the 10y to receive greater support than the 30y CTD.

The PSPP2 estimate for November buying of Bunds:

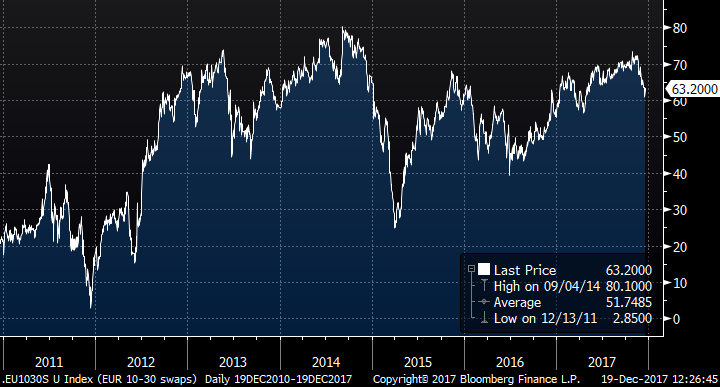

While I see potential for the 10y-30y curve in Germany to steepen (more long-end supply, more QE support in 10y), the EUR swap curve has the potential to flatten further. The apparent termination of the ESM long-end paying flows has been widely seen as one factor in this, though I favour bear-flattening moves in general across the swap curve as short-rate expectations (on a one-year horizon) become less well-anchored.

EUR 10y-30y in Swaps:

Finally, being long RX spread and short UB is a good insurance position should either the forthcoming Catalonia elections or next Spring's Italian elections create uncertainty around the political fortunes of the EU. In stressed times, 10y spreads have outperformed 30y as the increased risk premium steepens the ASW curve.

David Sansom

image001.jpg@01D21F13.B69A4950"/>

UK: 60 Cannon Street, London, EC4N 6NP US: 245 Park Ave, 39th Floor, NY, NY, 10167 Office: +44 (0) 207 002 1346 Mobile: +44 (0) 7976 204490 Email: david.sansom@astorridge.com<mailto:david.sansom@astorridge.com> Web: www.AstorRidge.com

This research was prepared by David Sansom. He is a consultant with Astor Ridge. A history of his research can be provided upon request in compliance with the European Commission's Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287 Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185 Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626 Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796