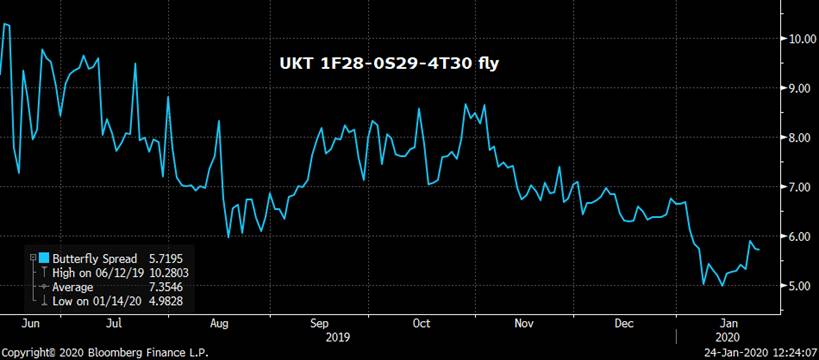

MICROCOSM: GILTS - Another 0S29s Tap Next Tuesday > RV Rundown/Ideas

- TRADE IDEAS:

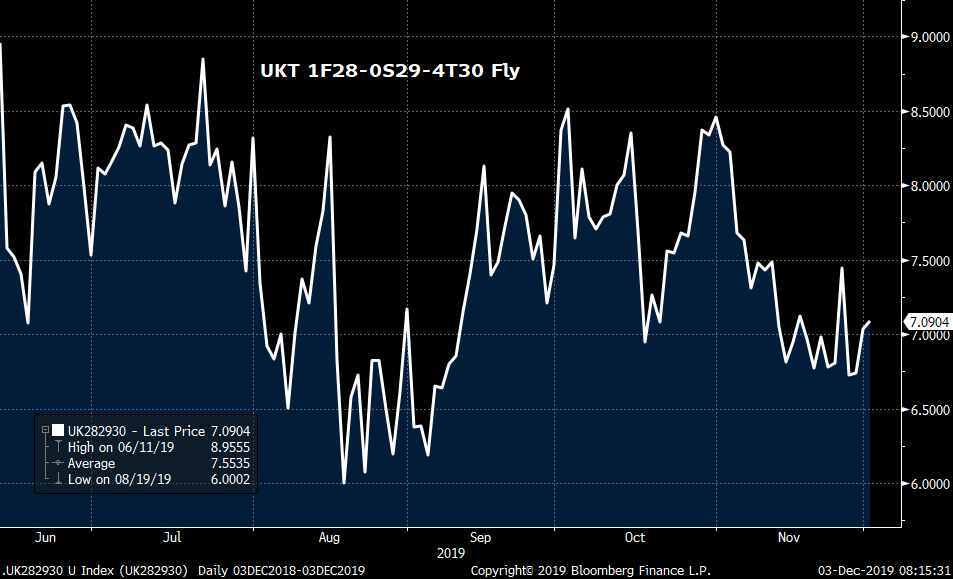

- Play the auction concession on either leg as it’s proven a buy at the last few auctions – 28-29s back to +8.5, 29-30s below 2.0bps.

- Or buy the belly of the 1F28-0S29-4T30 fly above 6.5bps.

GILTS... 0S29s Tap Tues

- We're closing in on the last few taps of these 29s before their successor is auctioned next fiscal year.

- Typically, this is the time in the cycle when benchmarks remove some/all of their new issue cushion vs the curve. We can see from the charts below that much of that convergence has already happened. The 28-29-30s fly tightened from +10.2 to +5.0bps before cheapening a touch to 5.7 this am. Much of that tightening happened post the Z9-H0 calendar sprd action and post- 1F28s delivery. Add to that a rather humble start for the 4T30s performance as CTD into G H0 and one could argue that for an issue that didn’t have a lot going for it (non-ctd sandwiched between the old and current CTDs) they’ve done well.

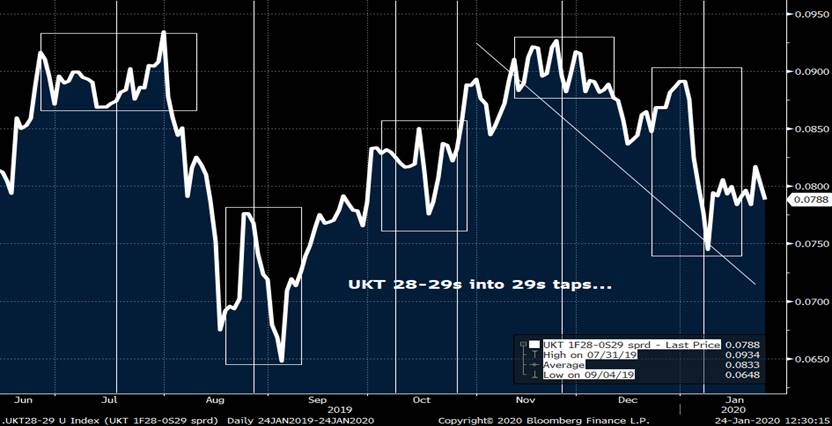

UKT 28-29s sprd… Over the last few months the trajectory has been flatter and modest steepening moves into taps were buying opportunities.

On the other side is the 29s-30s leg. Into the last tap on Jan 7th, the 29-30s sprd flattened to 1.7bps before steepening back to 2.7 by day’s end. Again, the steepening trajectory has reflected not only how poorly the 4T30s have traded but the progression of the auction cycle. A move through 2.0bps will attract buyers of 0S29s.

- After Tuesday’s tap, the 0S29s will be roughly £24.5bn and, barring a dramatic shift in gears at Javid’s budget announcement on Mar 11th, the Feb 25th tap will likely be its last as the issue will be ~£27bn, the same size as the 1F28s.

- While these 0S29s are unlikely to have much of a repo bid given their large float and non-CTD status, they’re still an important source of 10yr liquidity and with a 102 handle, they’re over 40 points cheaper to buy than their neighbour, the 4T30s, not to mention their higher duration and the same convexity.

- The March APF operation is set to begin on Monday March 9th. As you’ll have read in previous notes of ours, the surprise tap of the 4T30s announced for March 10th (£3.5bn in cash or ~£2.5bn notional at current prices) will make them eligible for the intermediates operations from March 18th onwards as the additional £2.5bln takes them back below the BoE’s 70% ownership threshold. Back at the last APF following the maturity of the UKT 3T19s, the 0S29s were still quite young at just ~£10bn which meant the BoE ignored them in favour of the 1Q27s, 1F28s and 4H34s. Going into March, we’re going to have the biggest intermediates bucket by issues and available liquidity for quite a while with the 1Q27s, 1F28s, 0S29s, 4T30s and 4H34s providing ample liquidity at an available notional of around ~£50bn. Good news for the BoE, not so good for the RV community who are keen to play the scarcity card. In an even playing field where there’s little repo value we’re supposed to buy the cheap stuff and sell the rich stuff with little regard for repo specials. This can change (we hope), but our assessment now is the belly of the curve could be a bit sleepy at the Mar APF…

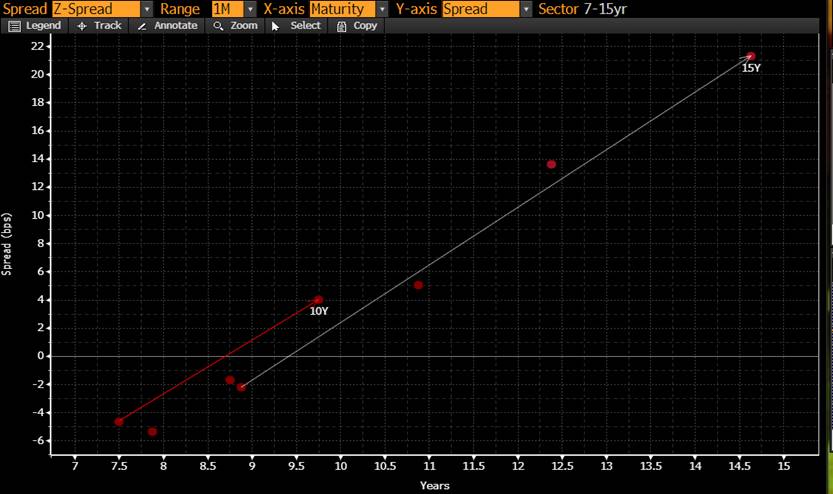

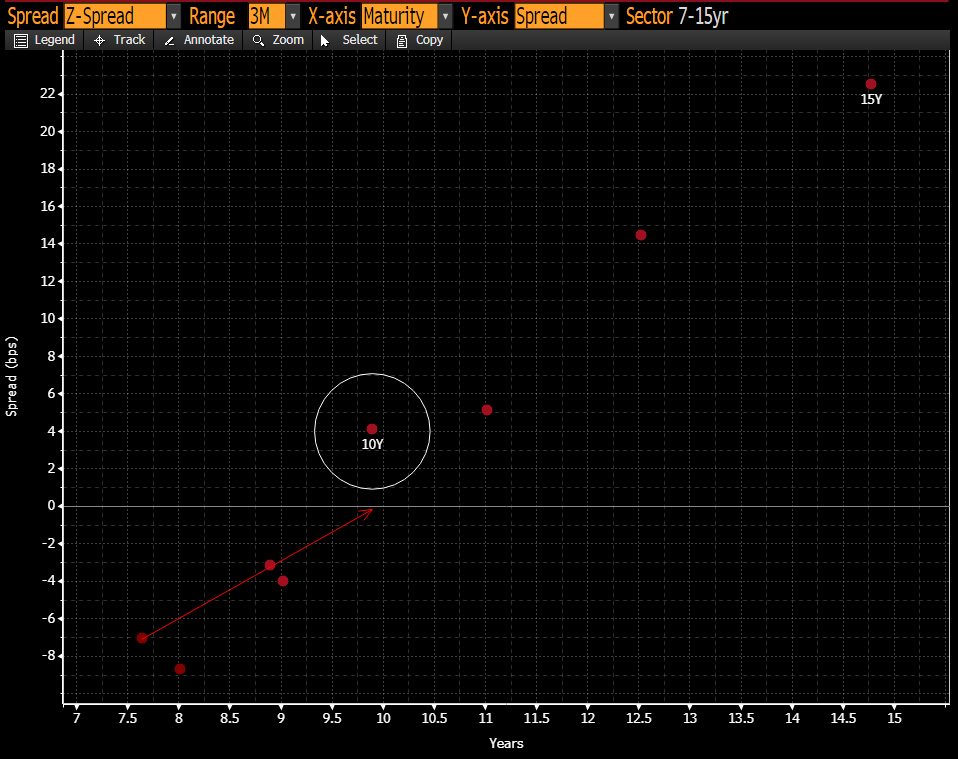

7-15yr Gilts Z-sprds – white line high cpns, red line low cpns…

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Bloomberg Bond News Summary > Thu Jan 23rd

Business Briefing

1) Stocks Slide on Virus-Impact Concerns; Bonds Rise: Markets Wrap

(Bloomberg) -- Stocks, crude oil prices and the yuan slumped on Thursday on concerns about the impact of the new China virus on corporate sales and economic growth. The yen edged up with Treasuries. On the last trading day in China before the nation’s epic travel season for the lunar new year holidays begins, the country’s stocks tumbled about 3%. With China moving to shut ...

2) Euro Can Look to Yuan to See Tariffs Mean Declines: Markets Live

3) Follow Bank Indonesia’s Rate Decision in TOPLive

(Bloomberg) -- Bank Indonesia is seen to leave its key interest rate unchanged. Of the 34 economists surveyed by Bloomberg, 29 predict the central bank will keep the key rate unchanged at 5%, with the rest forecasting a 25 basis-point cut.

- You can follow our TOPLive blog here

- For preview: Bank Indonesia Seen on Hold as Currency Rallies: Decision Guide

4) TOPLive Starts: Follow Bank Indonesia’s Monetary Policy Decision

5) China Virus Triggers Wuhan Travel Ban Ahead of Holiday (4)

(Bloomberg) -- Chinese officials halted travel from Wuhan, essentially locking down the city of 11 million people as they try to stop the spread of a new SARS-like virus that’s already killed 17 and infected hundreds. The coronavirus, which first appeared last month in the central China city of Wuhan, has spread from the mainland to places including Hong Kong and the U.S. ...

World News Briefing

6) Trump Is Portrayed as Danger to Democracy in Impeachment Trial

(Bloomberg) -- House Intelligence Chairman Adam Schiff presented the U.S. Senate with a dark portrait of a deeply flawed, even dangerous president as he argued that Donald Trump should be removed from office. Leading off the House prosecution of Trump on Wednesday, Schiff cited evidence at the heart of accusations in the articles of impeachment to describe a president who ...

7) China Bans Travel From City of 11 Million to Contain Virus

(Bloomberg) -- The Chinese city at the center of a widening respiratory-virus outbreak suspended outbound flights and rail service, as China ramps up efforts to contain an illness that’s killed at least 17 people and infected hundreds. The travel halt by the city of Wuhan was reported by state broadcaster CCTV. The city of 11 million people also suspended travel by bus, ...

8) Brexit Deal Clears Parliament, Paving U.K.’s Way to Leave the EU

(Bloomberg) -- Prime Minister Boris Johnson’s Brexit deal cleared its final hurdles in Parliament, bringing the crisis that paralyzed U.K. politics since the country voted to leave the European Union almost four years ago to a close. The passage of the law vindicates Johnson’s gamble to call an election last month in which he asked voters to back his blueprint for leaving ...

9) Bezos Hack Began With Saudi Goodwill Tour, Intimate Dinner

(Bloomberg) -- In the spring of 2018, Saudi Arabia’s crown prince, Mohammed Bin Salman, arrived in the U.S. for a three-week cross-country tour to pitch a progressive vision for his kingdom, including an economic plan less reliant on oil, and to charm America’s elite. He visited MIT and Harvard, talked space travel with Richard Branson and hobnobbed with celebrities, ...

10) Trump Weighs Plan to Expand Controversial Ban on Travel to U.S.

(Bloomberg) -- President Donald Trump is reviewing a Homeland Security Department recommendation that he expand one of the most controversial policies of his administration by banning people from an additional seven countries from traveling to the U.S. The department suggested the White House expand the travel restrictions to Tanzania, Belarus, Eritrea, Kyrgyzstan, Myanmar, ...

Bonds

11) Amateur Investors Risk Losing Everything in Hunt for Yields

(Bloomberg) -- After years of falling debt yields and new technologies enabling one-click purchases of complex financial products, mom and pop investors around the world are making bets that put them at danger of getting burned. In South Korea, regulators are investigating sales of derivative-linked products that caused individuals to lose almost all their invested money. Chinese savers ...

12) Japan Goes Looking for 6% Yields as Funds Buy Record Asian Bonds

(Bloomberg) -- Japanese investors bought the most emerging-Asian bonds on record last year, and their appetite is growing, money managers said. They snapped up almost 1 trillion yen ($9 billion) of Asian debt in the first 11 months of 2019, according to the latest balance-of-payments data. Even though it’s one month short of a year, that’s a record in data going back to ...

13) Bank CoCo Yields Hit Record Low After Plunging by Half: Chart

(Bloomberg) -- Yields on European lenders’ contingent convertible bonds, or CoCos, are at a record-low 3.76% after falling by about half since the start of last year, according to a mixed-currency Bloomberg Barclays bond index. Investors are flocking to the deeply subordinated notes because negative interest rates and enhanced bank capital buffers have bolstered the appeal of their high coupon payments. The ...

14) Trump Should Look Stateside for Buyers of Negative-Yielding Debt

(Bloomberg) -- U.S. President Donald Trump’s trip to Europe this week led him to wonder aloud just who’s buying the region’s negative-yielding debt. He might be surprised to hear that there’s plenty socked away in American retirement accounts. “I want to know who are these people that buy,” Trump said Wednesday in an interview on CNBC from Davos, Switzerland, where he was ...

15) Lebanon to Decide on March Bond Next Week, Finance Chief Says

(Bloomberg) -- Lebanon’s incoming Finance Minister Ghazi Wazni said the fate of a $1.2 billion Eurobond maturing March 9 will be the new government’s top priority when it meets next week, as investor concerns intensify that the country could default. “This is a priority and will be the first item to be discussed,” Wazni said Wednesday in his first interview with an ...

16) Aussie Gains on Jobs While Virus Fears Boost Yen: Inside G-10

(Bloomberg) -- Australia’s dollar gained against all major peers after better-than-expected jobs data damped expectations for a rate cut. The yen rose with Treasuries as deepening worries about a SARS-like virus from China spurred haven demand.

- AUD/USD climbed as much as 0.5% to 0.6879 before paring gains to trade at 0.6860

- Employment rose 28,900 in December, beating economists’ estimates of a 10,000 gain. The ...

Central Banks

17) Turkish Rate Guidance Intact After Five Cuts Went ‘Bit Deep’ (1)

(Bloomberg) -- Turkey’s central bank is standing by its promise of a positive real rate of return to investors despite five interest-rate cuts that Governor Murat Uysal conceded “were a bit deep.” Speaking Wednesday in interviews with Turkish TV at the World Economic Forum in Davos, Switzerland, Uysal said returns will run above zero based on the projected path of slowing ...

18) Pound Forecasters Tune Out BOE Rate-Cut Calls to Sound Upbeat

(Bloomberg) -- The risk of an interest-rate cut as early as this month seems no impediment to a stronger pound. The currency is predicted to steadily climb for most of 2020, ending the year 3% stronger than current levels against the dollar. That argument is based on a relatively smooth U.K. exit from the European Union, drawing capital inflows into sterling assets, and ...

Economic News

19) ECB Hopes Economic Calm Buys Reflection Time: Decision Day Guide

(Bloomberg) -- European Central Bank President Christine Lagarde can consider herself fortunate -- the euro-area economy has brightened just in time to allow her to focus on a strategic review that could last the rest of the year. The Governing Council’s policy decision on Thursday will be dominated by the announcement of the first appraisal of its inflation goal since ...

20) If Merkel Wants to Fix the German Economy, She Needs to Hurry Up

(Bloomberg) -- Angela Merkel is running out of time to reset the German economy before her era as chancellor draws to a close. The Group of Seven’s longest-serving leader weathered the financial crisis and Europe’s debt turmoil. But in the final full year of her tenure, as Germany’s economic problems fester, lawmakers are starting to ask if she has the vision and energy to ...

21) Circular Economy Lures BlackRock, Google as a Davos Darling

(Bloomberg) -- When British yachtswoman Ellen MacArthur was promoting the idea of the circular economy on the sidelines of Davos in 2012, the big attraction was curiosity about what she was up to after her sailing career. Eight years on, MacArthur’s vision is taking hold at the World Economic Forum’s annual gathering, and firms such ...

22) ECB’s Lagarde Finally to Air Scope of Strategy Review: Economics

(Bloomberg Economics) -- European Central Bank President Christine Lagarde will reveal today the most comprehensive outline yet of the monetary strategic review -- scheduled to be published in about a year. The broad guidelines will probably be scoured for hints on how monetary policy could potentially be changed, though we don’t expect enough detail to emerge to draw conclusions about future stimulus. ...

23) Three Perspectives On the Biggest Issues at Davos (Podcast)

These are the issues that are front-of-mind for attendees of this week’s World Economic Forum in Davos, Switzerland. On a special episode direct from the conference, Stephanie Flanders dives in with a leader from each field. ...

European Central Bank

24) Five Years of ECB Stimulus Stokes Relentless Credit Rally: Chart

(Bloomberg) -- Five years after the European Central Bank announced its historic quantitative easing program, the bull market in company debt is stronger than ever. Anyone who invested 100 euros in investment-grade bonds at the start of the stimulus cycle has netted a 12% gain -- no mean feat for what’s supposed to be a boring asset class.

25) TRANSLATION: Böersen-Zeitung: ECB criticizes institute protection

26) GERMANY DAYBOOK: ECB Strategic Review, Hochtief, Lufthansa Unit

(Bloomberg) -- Christine Lagarde kicks off the ECB’s strategic review today. Officials plan a two-part approach that breaks out inflation targeting, people familiar said. WHAT TO WATCH:

- Top News:

- ECB Hopes Economic Calm Buys Reflection Time: Decision Day Guide

- If Merkel Wants to Fix the German Economy, She Needs to Hurry Up

- Hochtief Sees Full Year Nominal Net EU660 Mln after unit CIMIC Exits Middle East and ...

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MICROCOSM: EGB Supply Barrage Resumes > 15bn from Spain and France this AM

FRTR and SPGBs THIS AM

- Another wave of bond supply kicks off this am with €15bn coming from Spain then France, their first auctions of 2020.

- Spain will come with up to €5.5bn of their SPGB 10/21s, 7/24s and 7/35s.

- As noted earlier this week, the Spanish curve from 10s-30s is remarkably flat and although the 7/35s trade a touch cheap on the curve, they're still just Eur 11.3bn so will be tapped several more times and will likely remain cheap this qtr. At a push, the 10/29-7/35-7/41 fly has cheapened 3.5bps to +19.5bps, near it's cheapest since mid-Oct which could be enough to attract a bit of demand.

- The SPGB 10/21s look cheap on a micro-basis which will attract domestic interest. The SPGB 7/21-10/21 sprd (yld and Z-sprd) has steepened nicely into this am's tap and the 1/21-10/21-10/22 fly is holding it's even yield resistance on the chart back to early 2019.

SPGB 7/21-10/21 sprd

SPGB 1/21-10/21-10/22 fly

- In a similar fashion to the SPGB 10/21s, the SPGB 7/24s have also cheapened on the curve of late. The SPGB 7/23-7/24 sprd has steepened back to the +11.5bps area from 5bps in Oct and the SPGB 10/22-7/24-4/26 fly is at its cheapest level in the past year. So, if one needed an excuse to lift these SPGBs, you’ve got one.

SPGB 7/23-7/24

SPGB 10/22-7/24-4/26 fly

- Spain has opened 2020 with a modest spread tightening vs most of the EGB universe so those looking for opportunities to add SPGB risk cheaply will struggle a bit. That said, carry and roll on the SPGB curve is still better than most of the OATs curve, especially in the front-end. Spreads like the FRTR 0 3/24 into SPGB 0.25 7/24 gain about 2.5bps in C&R over 3 mos and we’re ~6bps off the sprd lows we saw in Oct/Nov…

- France’s AFT will be issuing up to Eur 9.5bn of the FRTR 0 11/29, FRTR 1.25 5/36 and FRTR 1.5 5/50s, considerably more risk than Spain’s supply 20mins earlier. From our perspective, there don’t appear to be any glaringly obvious freebies among these 3 taps.

- The FRTR 0 11/29s are still a very young issue as this is only their second tap since their Oct introduction and, as such, they should trade with a bit of ‘juice’ in them. So far, however, they’ve held in well with the FRTR 5/29-11/29 sprd in a stable 4.0-4.5bps range since mid-Nov. Just beyond them, the FRTR 2.5 5/30s look a bit cheaper but again, we’re splitting hairs as these are micro sprds. More broadly, OATs yields have risen back above zero and we would agree with some of our dealers who assert that OATs look cheap to OLOs into this am’s supply.

BGB 6/29 v FRTR 11/29s > 5 mos of curve in there but should OATs should probably be closer to even yield at worst.

- More to come!

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MICROCOSM: UK> Quick Preview of Final MPC Meeting of 2019

BoE's MPC Meets Today at Noon London Time – no press conference scheduled.

- UK Base rates currently at 0.75%, O/N Sonia at 71bps with repo G/C right around there. Consensus is for NO CHANGE to base rates.

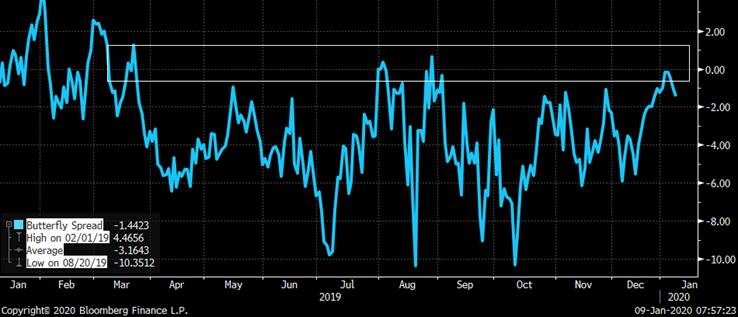

- The last meeting (Nov 7) was the first time since Jun '18 where there were two dissenters, 7 voting for no move, Haskel and Saunders arguing for a 25bps cut. This dissention coincided with a divergence between Cable and SONIA (as the chart below shows), Sonia staying put while Cable rallied.

Vertical lines are MPC meetings…

- Initial market reaction to the outcome of the UK election was justifiably bearish rates and bullish for Cable as it removed considerable political uncertainty. However, Johnson’s insistence that the UK-EU trade deal is completed by the end of 2020 has the market on edge again, even before Brexit’s official. The press jumped on a bandwagon with a ‘this ain’t gonna be easy’ message that sparked a reversal in GBP and a sticky SONIA curve that prices in a 30-40% chance of a 25bps rate cut from the MPC in the next 18mos.

- As you can see from this screen-grab, the market thinks the MPC is indeed ‘in-play’. What’s also worth pondering is whether Carney’s imminent departure opens the door for more dissension among MPC members. We should learn who the new Governor is by tomorrow evening (ahead of the Queen’s speech), however, while a rate cut is highly unlikely (especially with the FED and ECB on hold), another 7-2 or even 6-3 vote will keep the SONIA curve richer than one would have expected given recent events.

- To be frank, the gilts curve has been all over the place since the end of November. The combination of a ‘pancake-flat’ Z-sprd curve from 2023s to 2028s, the richness of the 1F28s and 0S29s into G Z9-G H0 sprd activity and the whipsaw in the long-end into and out of the election has made curve RV a tad treacherous. We maintain the view that while the threat of a No-Deal Brexit is certainly real, especially in light of Johnson’s remarkable majority in Parliament, there is a great deal of wood to chop before we need to panic about the post-Brexit outlook.

- Into today, we’re watching the 1.310 level in Cable, the 0.82% level in UKT 0S29s and SONIA’s Dec 20 MPC level…

Stay tuned!

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

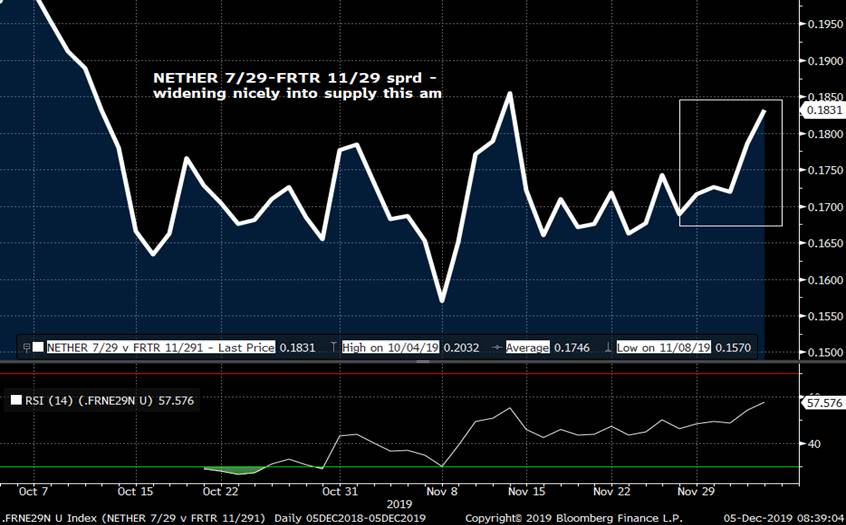

MICROCOSM: Quick Preview - SPGBs and FRTRs supply this morning...

- BUSY morning for EGBs supply with the following on tap:

- SPAIN taps their SPGB 0.25% 7/24, SPGB 0.6% 10/29 and SPGB 2.7% 10/48s for a modest Eur 3bn combined (about 29k RXH0s)

- FRANCE taps the FRTR 0.75% 5/28, FRTR 5.5% 4/29 and FRTR 4.0% 4/60s, also a modest 4.0-5.0bn for France (about 75k RXH0s)

- Broadly speaking, the aggregate risk we’re getting this morning is on the light side, however, it is Dec 5th and risk appetites are on the lighter side of normal. Add that to quiet Dec PSPP demand and spreads that were at/close to the year’s tightest to DBRs and we’re looking at a bit of a juggling act. Not sure whether the AFT’s decision to tap some more obscure off the run issues is much help, either, especially the high cpn FRTR 5.5% 4/29s.

- As you’ll have read by now, there’s a seasonality to OATs spreads to DBRs/NETHER, widening in December after bullish Oct/Nov cash flows drive a spread narrowing. January tends to be a busy month for OATs supply too, encouraging dealers and leveraged players to unwind OATs longs. We’ve seen a nice little widening of the NETHER 7/29-FRTR 11/29 spread into this morning’s supply – which will likely prompt a bit of short covering in OATs.

- We’ve seen a nice steepening in the belly of the SPGBs curve, the SPGB 4/26-4/28 sprd (boxed vs swaps) 6bps wider since the start of Nov. Looks a bit overdone to us.

We’ve also seen a nice cheapening of the SPGB 4/26-4/28-7/30 fly…

More to come…

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

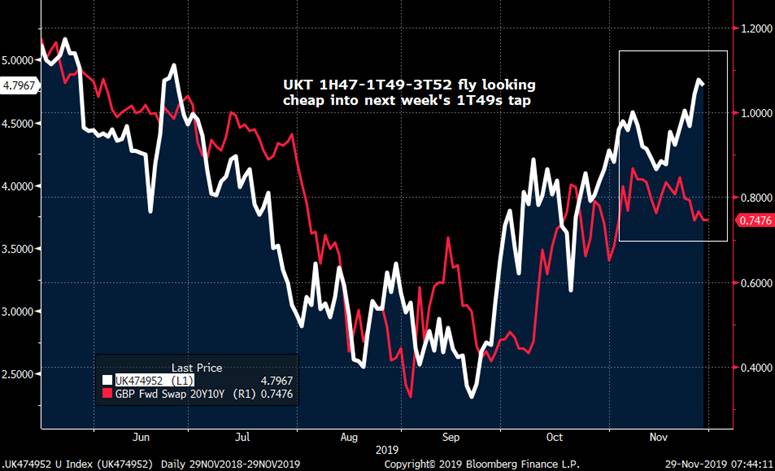

MICROCOSM: GILTS - 1T49s TAP - TRADES WE LIKE

- DMO Taps the UKT 1T49s this morning at 10:30 in £2bn, the last scheduled tap until March 17, 2020 (barring a revision to the current borrowing levels).

- Today’s tap takes the issue just above ~£15bn, which is about 2/3 through their auction cycle based on the size of the 1H47s (£24.4bn).

- If you’ve been reading our GILTS updates over the past couple weeks, you’ll know that we like these 1T49s here. The issue looks cheap on the curve to us (see charts below) and with a new UKT 2041 coming on Jan 21st, followed by a ultra-long conventional tap in mid-February, there will be ample RV motivation to overweight the 30yr point.

- From a more macro perspective, the 10-30s spread remains a fairly directional trade, steepening in a rally, however, the December 7th coupon payments are tilted towards the 15-30yr sector which has real money extending out the curve a tad early, front-running their cash flows. Of the £2,515bn in cash hitting the market, 53% of the cash (£1,343bn) will be paid to June and December gilts. While this cash flow is supportive, it’s market impact will be well behind us when the Brits hit the polls on Dec 12th, which is more than likely the reason these 1T49s continue to trade cheap on the curve.

- From a tactical perspective, there are two ways to play this – short-term and medium-term. From a short-term perspective, we’d advocate a more micro approach, buying the 1T49s vs 1H47s and 3T52s. Or, maintain a modest steepening bias - long 1T49 vs 3T52. Medium-term, the above-mentioned supply calendar suggests a long 1T49s vs 4Q40 and 1T57 fly makes a lot of sense and, as we can see from the chart below, we’re at a level that has proven a great entry level for this fly over the last year.

- Charts:

Inverse correlation of the sprd vs 4T30 yields was very high until breaking down in Aug/Sep. Correlation resuming now it seems…

UKT 1H47-1T49-3T52 fly looks cheaper than where 49s yields say it should be. Looks to be turning now…

UKT 4Q40-1T49-1T57 fly is back to a key entry level to get long 49s…

More to come…

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Bloomberg Bond News Summary > Thus Dec 5th

Business Briefing

1) RBI Governor Das Sees Some Green Shoots in Investments: TOPLive

2) Stocks Mixed as Trade Talks Mulled; Yields Dip: Markets Wrap

(Bloomberg) -- U.S. and European stock futures were little changed after a mostly positive session in Asia as investors monitor prospects for removing a scheduled American tariff hike on China later this month. Treasuries advanced, clawing back some of their losses from Wednesday, when a report indicated the U.S. and China were closer to a deal that would avoid the next ...

3) GM to Start Battery Venture With LG in Ohio, Reuters Says (1)

(Bloomberg) -- General Motors Co. and LG Chem Ltd. are starting a joint venture in Ohio to make batteries for electric cars, Reuters reported, citing people familiar with the matter. The 50-50 joint venture is set to be announced Thursday, Reuters said. The U.S. carmaker and the South Korean battery giant will each invest more than $1 billion in the planned facility in ...

4) South African Airways to Enter Into Bankruptcy Protection (3)

(Bloomberg) -- South Africa’s government will place the national airline under a local form of bankruptcy protection as a last-ditch measure to try and prevent its total collapse. State-owned South African Airways is entering a business-rescue process to allow a “radical restructuring” under which the carrier will receive 4 billion rand ($274 million) in funding, Public ...

World News Briefing

5) U.S., China Move Closer to Trade Deal Despite Harsh Rhetoric

(Bloomberg) -- The U.S. and China are moving closer to agreeing on the amount of tariffs that would be rolled back in a phase-one trade deal despite tensions over Hong Kong and Xinjiang, people familiar with the talks said. The people, who asked not to be identified, said that U.S. President Donald Trump’s comments Tuesday downplaying the urgency of a deal shouldn’t be ...

6) Senate Defies China Threat, Smoothing Path for Human Rights Bill

(Bloomberg) -- The U.S. Senate is rushing to approve a bill to punish China for the oppression of a Muslim ethnic group, with a bipartisan pair of senators maneuvering to get the measure to President Donald Trump as soon as possible. Republican Senator John Cornyn and Democrat Mark Warner introduced legislation Wednesday that would control exports to China of surveillance ...

7) Warren Is Drafting U.S. Legislation to Reverse ‘Mega Mergers’

(Bloomberg) -- U.S. Senator Elizabeth Warren is drafting a bill that would call on regulators to retroactively review about two decades of “mega mergers” and ban such deals going forward. Warren’s staff recently circulated a proposal for sweeping anti-monopoly legislation, which would deliver on a presidential campaign promise to check the power of Big Tech and other ...

8) Merkel’s Survival Hinges on Election Threat of Greens, Far-Right

(Bloomberg) -- If Angela Merkel sees out her fourth term as German chancellor, fear may likely play a greater role than political skill. Merkel’s Christian Democrats have been plagued by a fierce leadership struggle and the Social Democrats, her junior coalition partner, are toying with the idea of exiting the coalition. Yet with the surge in popularity of the Greens and ...

9) Macron Faces Dreaded Test of French Presidents as Unions Strike

(Bloomberg) -- Emmanuel Macron’s push to transform France’s sclerotic economy is facing the ultimate test of presidents past: “la greve.” In what has been the undoing of previous French governments, unions representing everyone from transport workers to lawyers, doctors, teachers and students are going on an indefinite “greve,” or strike, starting Thursday. The strike will ...

Bonds

10) Asia Dollar Bond Sales Hit Record as Deals Keep Coming: Chart

(Bloomberg) -- Sales of Asian dollar bonds have hit an annual record of almost $322 billion as companies leap at cheaper money on offer from yield-starved investors. A handful of issuers are in the market Thursday, which should add to yearly totals. Returns on Asian dollar bonds are on track for their best year in five. Debates are heating up on the outlook for next year, as concerns about defaults in China and ...

11) End of Imaginary Stimulus May Be a Real Risk to Markets in 2020

(Bloomberg) -- The Federal Reserve may be inadvertently setting the stage for more market turmoil in 2020 because it can’t persuade investors to ignore its multitrillion-dollar balance sheet. The Fed’s withdrawal from “non-QE” is the biggest risk facing investors next year, according to strategists from John Hancock Investment Management. They say the central bank’s ...

12) Kiwi Rises as Rate-Cut Bets Fall, Data Hits Aussie: Inside G-10

(Bloomberg) -- New Zealand’s dollar climbed to a four-month high as investors trimmed bets on interest-rate cuts after the central bank gave local lenders more time to meet capital requirements. The Australian dollar fell after weak retail sales data.

- Kiwi gained for a sixth day after Reserve Bank of New Zealand Governor Adrian Orr said monetary policy was currently in a ...

13) Bond Rout That Didn’t Happen in Japan Casts Stimulus Doubt

(Bloomberg) -- A stimulus package worth more than $200 billion would have led to a bond rout in any market. Not in Japan, where the yield curve held at its flattest level in three months. The reason? Traders don’t expect Prime Minister Shinzo Abe’s government to actually spend the headline figure of 26 trillion yen ($239 billion), which means there won’t be massive debt ...

14) Time for Unconventional RBI Measures, Bond Manager Says

(Bloomberg) -- It’s time for the Reserve Bank of India to take unconventional policy measures as rate cuts are failing to stimulate the economy, according to the head of fixed income at IDFC Asset Management Co. The central bank, which reviews policy on Thursday, should look to pull down long-term yields by selling short-tenor bonds and reinvesting in longer-term ones, said ...

15) The Utility Behind Fukushima Disaster Is Mulling Green Debt

(Bloomberg) -- A new subsidiary of the Japanese power company behind the worst nuclear disaster since Chernobyl is considering funding hydro and wind energy projects with green or sustainable bonds. Almost nine years since a major earthquake and tsunami crippled Tokyo Electric Power Co. Holdings Inc.’s Fukushima plant, Japan’s biggest utility is shifting its renewable ...

Central Banks

16) TOPLive Starts: Follow RBI's Monetary Policy Decision, Briefing

17) India Stocks Fall as RBI Cuts Growth Forecast, Holds Rate

(Bloomberg) -- The S&P BSE Sensex declined as much as 0.3% after Reserve Bank of India cut its forecast for economic growth while unexpectedly keeping its key policy rate unchanged.

- HDFC Bank contributed the most to the Sensex decline, falling 0.8%, while Yes Bank had the largest drop, decreasing 2.3%

- Fourteen of 19 sector sub-indexes compiled by BSE Ltd. fell, led by a gauge of telecom ...

18) India’s Central Bank Unexpectedly Holds Rate as Inflation Spikes

(Bloomberg) -- India’s central bank unexpectedly kept its benchmark interest rate unchanged as headline inflation breached its medium-term target for the first time in more than a year. The repurchase rate was left at 5.15%, the Reserve Bank of India said in a statement on Thursday. None of the 43 economists surveyed by Bloomberg predicted the move, with all expecting a ...

Economic News

19) Japan Leans on Fiscal Stimulus to Keep Recession at Bay

(Bloomberg) -- Japan’s Prime Minister Shinzo Abe announced stimulus measures to support growth in an economy contending with an export slump, natural disasters and the fallout from a recent sales tax increase. The total stimulus package amounts to around 26 trillion yen ($239 billion) spread over the coming years, with fiscal measures around half that figure, according to a ...

20) India’s RBI Unexpectedly Holds Key Rate as Inflation Spikes

(Bloomberg) -- India’s central bank unexpectedly kept its benchmark interest rate unchanged as headline inflation breached its medium-term target for the first time in more than a year. The repurchase rate was left at 5.15% in a unanimous decision, the Reserve Bank of India said in a statement on Thursday. None of the 43 economists surveyed by Bloomberg predicted the move, ...

21) ECB Resolve on Negative Interest Rates Is Waning Under Lagarde

(Bloomberg) -- Five weeks since Mario Draghi retired from running the European Central Bank, finding an outright fan of his legacy of negative interest rates has become a lot harder. Governing Council members, who collectively lowered the key rate to minus 0.5% shortly before Draghi’s term ended, are increasingly portraying it as a necessary evil that shouldn’t be ...

22) France’s Prospects Rest on Working Smarter Not Longer: Economics

(Bloomberg Economics) -- President Emmanuel Macron has vowed to reform the French pension system where many of his predecessors have failed in the face of fierce public resistance. Again, unions plan a series of strikes this winter. His reforms aim to make the pension system financially sustainable. They would also mean gradually raising the retirement age, supporting GDP growth for decades to come. That’s a help, but our ...

23) The Making of the Man Europe Picked to Confront Trump on Trade

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here. When Phil Hogan was fighting for his political life, he knew just who to turn to: his enemy. Battling a party rebellion before Ireland’s 2011 election, Hogan reached out to an old contact among the plotters, one of the ...

European Central Bank

24) The ECB's Already Acting Against Negative Rates: Marcus Ashworth

(Bloomberg Opinion) -- Euro zone finance minsters are pushing back against the negative rate regime of the European Central Bank just as Christine Lagarde takes the reins from Mario Draghi. This is yet another rerun of the battle between the economically strongest (essentially northern) European nations and their weaker partners over who should shoulder the burden for maintaining ...

25) ECB Says It May Need Own Digital Euro If Payment Drive Fails (1)

(Bloomberg) -- The European Central Bank is willing to develop its own digital currency if the private sector can’t make cross-border payments faster and cheaper. In an internal document obtained by Bloomberg on Wednesday, the ECB argues that technological innovation is quickly transforming the way retail payments are made, including a decline in the use of cash. The ...

26) Knot Says Inflation Goal Always First as ECB Mulls Climate Risks

(Bloomberg) -- Dutch governor Klaas Knot joined his European Central Bank colleagues in arguing that efforts to fight climate change can’t come at the expense of the institution’s main focus on inflation. Speaking in Amsterdam on Wednesday, Knot said transitioning away from environment-polluting energy sources is the most important challenge for euro-area economies. While ...

27) ECB’s Visco Charts Italian Compromise on Europe’s Debt Conundrum

(Bloomberg) -- Bank of Italy Governor Ignazio Visco on Wednesday sketched out a possible compromise that could help complete a long-delayed drive to shore up the European Union’s financial system. Visco signaled his willingness to agree to limits on how much sovereign debt banks can hold without provisions -- something that Italy, with Europe’s largest debt burden, has so ...

Federal Reserve

28) Quarles Concedes Fed Might Be Part of the Problem in Repo Crunch

(Bloomberg) -- The Federal Reserve’s banking regulation chief granted that Wall Street may have been right that the agency shares blame in September’s alarming strain in money markets. Vice Chairman Randal Quarles agreed Wednesday that Fed supervisors have potentially created an impression that banks should prize cash reserves over stockpiled Treasuries when the firms try ...

29) Quarles Cites Liquidity Stress Tests for Adding To Repo Strain

(Bloomberg) -- Federal Reserve Vice Chairman for Supervision Randal Quarles says stricter post-crisis banking rules might have contributed to money-market strain in September, though they were probably not the prime cause of the turmoil.

- “There were a complex set of factors that contributed to those events in September. Not all of them were related to our regulatory ...

30) Fed Watch: Summary of Recent Remarks by Fed Policy Makers

(Bloomberg) -- This is Fed Watch, a summary of remarks since the Oct. 29-30 policy meeting:

- Next rate decision: Dec. 11

- Federal Open Market Committee portal, click HERE

- For upcoming events, click HERE

31) Fed partly blames stress tests for spike in borrowing costs

Preview text not available for this story.

First Word FX News Foreign Exchange

32) Tories Pledge Brexit and Budget in 100 Days: U.K. Campaign Trail

(Bloomberg) -- U.K. Prime Minister Boris Johnson pledged to deliver Brexit and a budget within 100 days if he wins the Dec. 12 election, and contrasted that with the “gridlock and uncertainty” that would result from the “very real possibility” of a hung Parliament. With a week to go until the vote, the Tories said their first 100 days would include a defense review, more ...

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MICROCOSM: GILTS > UKT 0S29 Tap at 10:30am

GILTS > UKT 0S29s @ 10:30

> Real mixed bag for this one.

> 0S29 yields have risen about 9bps in the past week but these 29s have richened 2.4bps to swaps and just 1bp off their richest ever.

0S29s vs swaps

> The 0S29s have done well on the curve in Nov, quietly outperforming 1F28s and 4T30s on the fly (+8.8 to +6.6 before late move to 7.2bps) as the mkt focused on the Z9-H0 calendar sprd. After today’s tap there are two more scheduled next year (Jan 7 and Feb 25) which will likely open the door for a new benchmark in Mar/Apr. So, we’re closing in on the end of their cycle and although they won’t be CTD, they’re cheap enough that they should grind richer over the next quarter.

7-15yr sector Z-sprd curve… If we take a linear approach to the low cpn issues, one could argue these 0S29s are still ~3bps too cheap.

> UKT 29s-49s has flattened sharply over the last week (from +56.5 to 51.4 this am) which reflects not just the back up in gilts yields but anticipated cpn flows Dec 7th that favour Dec maturities from 15yr+ (£666mm 7-15yr but £1.343bn 15-30yrs).

> Cable has been knocking on 1.30 since mid-Oct which is looking like formidable resistance with the election looming next week. Moody’s is out with some cautious remarks on the UK’s outlook this morning:

{GB} Reuters: MOODY'S SAYS UK BANKING OUTLOOK CHANGES TO NEGATIVE FROM STABLE AS OPERATING ENVIRONMENT WEAKENS

- MOODY'S -PERSISTENTLY LOW INTEREST RATES & INCREASED MORTGAGE MARKET COMPETITION ARE ERODING NET INTEREST MARGINS OF MOST UK LENDERS

- MOODY'S SAYS UK'S ECONOMY IS WEAKENING, MAKING IT MORE SUSCEPTIBLE TO SHOCKS, PROLONGED UNCERTAINTY OVER BREXIT HAS REDUCED GROWTH PROSPECTS

> Net-net, this isn't a slam-dunk for us risk-wise so we're playing this one from the cautious side, especially as it feels the market’s been in risk-reduction mode. We may get another crack at this supply at cheaper levels.

More to come…

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MICROCOSM: GILTS > Q4 2019/20 Supply Calendar Announced!

GILTS> Q4 FY '19-20 SUPPLY ANNOUNCED!

> Jan 7 - 0S29 Tap

> Jan 9 - Linker 28 Tap

> Jan 14 - 0F25 Tap

> Jan 21 - NEW 10/41 BENCHMARK (Finally!)

> Feb 4 - Linker 36 tap

- Feb 20 week - long conventionals syndication (likely an ultra - 54s, 71s, etc)

> Feb 25 - 0S29 Tap (perhaps its last)

> Mar 4 - 0F25 Tap

> Mar 12 - Linker 28 Tap

> Mar 17 - 1T49 Tap

Comments:

> These are roughly what we were expecting, especially the new 2041s. We've seen a nice steepening of 37s-42s into this announcement which could get another nudge wider in response. That said, 37-42-49s was looking on the cheap side.

> Big gap between taps of the 1T49s - after next Thursday's 49s it'll be over 3 months due to the ultras syndic. The 1T49s are worth a look if they cheapen further into next week's tap

Charts:

More to come!

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

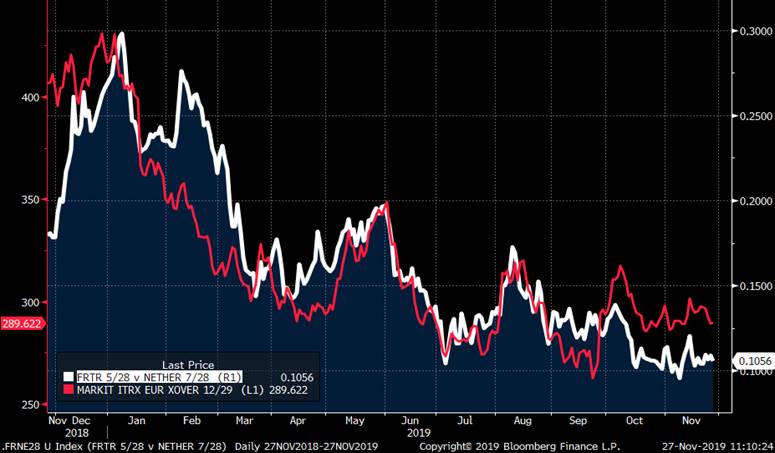

MICROCOSM: OATs - 'Bearish Dec Seasonals' Note Update

OATS... 'Bearish Dec Seasonals' Note Update

> Last Friday's note highlighted the seasonal bias for wider OATs sprds vs DBRs/NETHER for most of the last 10yrs (attached).

> With the end of Nov looming and spreads still at compressed levels, we still think the theme/bias still makes sense from both a profit-taking stance for OATs longs and/or a tactical short into year-end.

> The FRTR 5/26-11/28 sprd has flattened in both yield and Z-sprd, the box back close to 2019 lows. (chart)

> FRETR 5/28-NETHER 7/28 sprd continues to hover at/near the 2019 lows at 10.5bps and the FRTR 5/27-NETHER 7/27s version is off it's tightest but is still just +8.9bps.

> Broadly speaking, these low-beta credit spreads reflect overall credit biases (like ITRX XOVER) so a broader widening would certainly help, however, OATs issuance in January tends to be substantial which is often the impetus for the Dec widening.

More to come…

Mark

![]() image003.jpg@01D58404.6834BD00">

image003.jpg@01D58404.6834BD00">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796