EGB conventional supply for the week to the 4th, November.

Thanks Creo…

From: Stephen Creaturo <stephen.creaturo@astorridge.com>;

Sent: 04 November 2019 07:58

To: Peter Joos <Peter.Joos@astorridge.com>;; Chris Williams <Chris.Williams@astorridge.com>;; George Whitehead <George.Whitehead@astorridge.com>;; David Sansom <David.Sansom@astorridge.com>;; Mark Funsch <mark.funsch@astorridge.com>;; Gareth Edwards <gareth.edwards@astorridge.com>;; James Rice <James.Rice@astorridge.com>;; Robert Baida <robert.baida@astorridge.com>;; Mike Ohr <Mike.ohr@astorridge.com>;; Jim Lockard <Jim.lockard@astorridge.com>;; John Wentzell <John.wentzell@astorridge.com>;; Chris_Brighton <chris.brighton@astorridge.com>;; Brice Janney <Brice.Janney@astorridge-na.com>;

Cc: Research <research@astorridge.com>;

Subject: EGB conventional supply for the week to the 4th, November.

Tues: Finland taps 15y - 4/34s, 30y - 4/47s Total 1bl euros

Wed: Austria taps 5y - 10/24s, 10y - 2/29s Total 1bl euro

Thur: Spain taps 5y - 7/24s, 10y - 10/29s, 15y -7/35s Total 3.5bl euros

France taps 10y - 11/29, 15y - 5/34s, 30y - 5/50s, 50y - 5/2066s Total - up to 10bl euros

UK tap 10y - 0.875% 2029 total - approx. £3bl

Of the 5 lines of supply, most compelling - 15y Finland within the broader Finnish curve - either 10/15y both in YLD and ZCM, 10/15/30y curve, 15y Finland vs Germany

- 30y Finland in ASW at at a multi-year cheap level vs swaps

- 15y France vs 15y Belgium has value but my preference is for 10/15y ASW box which I struggle to see why the Belgium curve is flatter than France(ex-supply dynamic)

Generally supply points in smaller and much less liquid markets such as Finland and Austria, give one good opportunities to reduce friction cost for one side of the entry/exit cost.

As for the other markets, I see little in the way of RV trades at the moment. Lack of volatility and range trade mentality persist for the time being and offers up fewer distortions on the curve. That may change as

we get closer to year end.

So for what is worth, here is my take:

France: One big duration event for the day - historical pattern into and out of supply for large duration events well documented, but apart from duration event - not much to do on the micro RV side.

10yrs - roll has moved out to +8.5bps(1bps wider) vs 11/28s(ctd) - part directional, but in ASW terms very stable at +2.4bps - maybe 1bps in the trade vs Futures

15y - Fair value on the french curve at the moment - middle of tight ranges - only consideration for myself - 10/15y ASW box vs Belgium(chart below) - not sure Belgium curve should trade rich in this metric v France

30y - nothing to do, tight range in YLD and ASW locally.

50y - with the exception of one spike higher in ASW terms 30y/50y, the 50y in ZCM towards the higher end of a 3bps range.(chart below)

Spain: 5y - marginally expensive locally, and mid-range on wider flys

10y - marginally expensive locally, expensive vs France, cheap vs larger credit trade German/Italy blend vs Spain - possibly look for risk off trade into year?

15y - 10/15/30 fly in Spain - middle of the range - locally cheap vs other High Coupons taking into account duration differential

Austria: 5y - has come back quite quickly from cheap valuation to slightly through Fair Value, looks at the expensive of the range vs Germany.

10y - Nothing to do -mid range on all metrics.

Finland: 15y - cheap in 10/15/30 Finnish Curve, 10/15y both Yld and ZCM, cheaper end of range vs Germany in an environment whereby semi-core has been compressed into low and tight range generically.(chart below)

30y - cheap in ASW(chart below)

UK: 10y - we see good value in the 10y roll in LC UK gilts and as we get closer to expiry of the DEC futures(our thoughts on performance of new ctd 2030s) and the lead up to a new 10y in early 2020, seasonally the

issue is nearer its cheaper end of cycle range.

France/ Belgium ASW Box 29s vs 34s (34 Belgium Expensive vs France)

30/50y France 5/50 vs 5/66 - ZCM

Finland 10/15/30y Fly - 15y back to the cheaper end of the range

15y Finland vs Germany - 34s - spikes wider for supply announcement

10y/15y Finland 29s vs 34s Yield - possible directional bias - but relatively all curves in EGB space looking even flatter relative to the back up in yields of late

Finland 10/15 ASW Box rarely seen the side of positive in 2019

30y Finland ASW YY - back to multi year cheaper end of the range.

![]()

Stephen Creaturo

O: +44 (0) 203 - 143 – 4175

M: +44 (0) 7 809 575 890

E: stephen.creaturo@AstorRidge.com

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This marketing was prepared by Stephen Creaturo, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

EGB conventional supply for the week to the 4th, November.

Of the 5 lines of supply, most compelling - 15y Finland within the broader Finnish curve - either 10/15y both in YLD and ZCM, 10/15/30y curve, 15y Finland vs Germany

- 30y Finland in ASW at at a multi-year cheap level vs swaps

- 15y France vs 15y Belgium has value but my preference is for 10/15y ASW box which I struggle to see why the Belgium curve is flatter than France(ex-supply dynamic)

Generally supply points in smaller and much less liquid markets such as Finland and Austria, give one good opportunities to reduce friction cost for one side of the entry/exit cost.

As for the other markets, I see little in the way of RV trades at the moment. Lack of volatility and range trade mentality persist for the time being and offers up fewer distortions on the curve. That may change as

we get closer to year end.

So for what is worth, here is my take:

France: One big duration event for the day - historical pattern into and out of supply for large duration events well documented, but apart from duration event - not much to do on the micro RV side.

10yrs - roll has moved out to +8.5bps(1bps wider) vs 11/28s(ctd) - part directional, but in ASW terms very stable at +2.4bps - maybe 1bps in the trade vs Futures

15y - Fair value on the french curve at the moment - middle of tight ranges - only consideration for myself - 10/15y ASW box vs Belgium(chart below) - not sure Belgium curve should trade rich in this metric v France

30y - nothing to do, tight range in YLD and ASW locally.

50y - with the exception of one spike higher in ASW terms 30y/50y, the 50y in ZCM towards the higher end of a 3bps range.(chart below)

Spain: 5y - marginally expensive locally, and mid-range on wider flys

10y - marginally expensive locally, expensive vs France, cheap vs larger credit trade German/Italy blend vs Spain - possibly look for risk off trade into year?

15y - 10/15/30 fly in Spain - middle of the range - locally cheap vs other High Coupons taking into account duration differential

Austria: 5y - has come back quite quickly from cheap valuation to slightly through Fair Value, looks at the expensive of the range vs Germany.

10y - Nothing to do -mid range on all metrics.

Finland: 15y - cheap in 10/15/30 Finnish Curve, 10/15y both Yld and ZCM, cheaper end of range vs Germany in an environment whereby semi-core has been compressed into low and tight range generically.(chart below)

30y - cheap in ASW(chart below)

UK: 10y - we see good value in the 10y roll in LC UK gilts and as we get closer to expiry of the DEC futures(our thoughts on performance of new ctd 2030s) and the lead up to a new 10y in early 2020, seasonally the

issue is nearer its cheaper end of cycle range.

France/ Belgium ASW Box 29s vs 34s (34 Belgium Expensive vs France)

30/50y France 5/50 vs 5/66 - ZCM

Finland 10/15/30y Fly - 15y back to the cheaper end of the range

15y Finland vs Germany - 34s - spikes wider for supply announcement

10y/15y Finland 29s vs 34s Yield - possible directional bias - but relatively all curves in EGB space looking even flatter relative to the back up in yields of late

Finland 10/15 ASW Box rarely seen the side of positive in 2019

30y Finland ASW YY - back to multi year cheaper end of the range.

![]()

Stephen Creaturo

O: +44 (0) 203 - 143 – 4175

M: +44 (0) 7 809 575 890

E: stephen.creaturo@AstorRidge.com

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This marketing was prepared by Stephen Creaturo, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MACROCOSM: UK's OBR to publish NEW FORECASTS on NOV 7th > THOUGHTS

Report shows fiscal deterioration from the OBR budgetary projections made last year; paradoxically Gilt ASW spreads have not reflected this due to FTQ bid on heightened Brexit uncertainty….

*OBR SAYS IT PLANS TO PUBLISH NEW U.K. FORECASTS ON NOV. 7

Comments from our colleague George Whitehead…

To Me Public Finances look around £31.6bn worse than a year ago so new forecast have to show increased borrowing going forward....FWIW...

UK OBR 7th November New UK Forecasts:

• Borrowing (public sector net borrowing excluding public sector banks) in September 2019 was £9.2 billion, £0.4 billion more than in September 2018; this is the first September year-on-year borrowing increase for five years.

• Borrowing in the current financial year-to-date (April 2019 to September 2019) was £39.0 billion, £5.9 billion more than in the same period last year; this is the first April-to-September borrowing increase for five years.

• Debt (public sector net debt excluding public sector banks) at the end of September 2019 was £1,790.9 billion (or 80.3% of gross domestic product (GDP)), an increase of £27.3 billion, or a decrease of 1.2 percentage points, on September 2018.

• Debt at the end of September 2019 excluding the Bank of England (mainly quantitative easing) was £1,611.1 billion or 72.2% of GDP; this is an increase of £38.6 billion, or a decrease of 0.5 percentage points on September 2018.

• Central government net cash requirement was £32.9 billion in the current financial year-to-date; this is £13.5 billion more than in the same period in the previous year.

• Central government net cash requirement excluding both UK Asset Resolution Ltd and Network Rail was £32.7 billion in the current financial year-to-date; this is £12.2 billion more than in the same period last year.

Link to release: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/842880/PSF_bulletin_September_2019_corrected_HMT_V2.pdf

Jim Lockard

Founder / Managing Partner

![]()

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 12 EAST 49th Street, New York NY 10017

Office: +44 (0) 203 -143 - 4172

Mobile: +44 (0) 7795-027-865

Email: jim.lockard@astorridge.com

Website: www.astorridge.com

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MACROCOSM: US/UK/EUR Rates Supply > Quick Rundown w/Comments

Happy Monday…

- Please find attached our weekly rundown of upcoming US, UK and EUR supply. You’ll see that this week’s supply is very light across the board with a handful of auctions in Europe and some linkers in the UK.

- We’ve added a new table at the bottom which highlights the coupon and redemption flows due this week. As the US is in a league of it’s own in terms of the size and scope of coupon and redemption flows we’ve lumped them together for simplicity’s sake. European issuers’ C&Rs are less frequent and, generally speaking, has a less pronounced impact on short-term RV and month-end index extension levels.

- The cash flow ‘champion’ this week is clearly SPAIN where Bonos investors will have a whopping Eur 28.4bn in cash hitting their coffers on Halloween. Since the cash flows hit their accounts for settlement of tomorrow’s trades we’d expect Bonos holders with a windfall will be inclined to spend them tomorrow/Wed, even if the complexities of index creation may mean that the index extension in Spain doesn’t fully reflect this negative net supply (depending upon your provider).

- Let’s use BAML’s month-end numbers as a reference:

Country Extension New Eff Dur Closest EGB

Germany +0.12yrs 8.27yrs DBR .5 2/28

France +0.26yrs* 8.98yrs FRTR .75 11/28

Italy +.09yrs 7.28yrs BTPS 2.05 8/27

Spain +.06yrs ** 8.22yrs SPGB 1.4 7/28

Netherlands +.07yrs 8.92yrs NETHER .75 7/28

Belgium +.04yrs 10.38yrs BGB 4.0% 3/32

- French cash flows will help drive a large extension into month-end. Long-end supply resumes next week, however, so we’re looking to sell into the late-week bid as the monthly ‘cushion’ on the curve/spreads is built in to take down the duration.

- We can see that the index move in Spain is rather small given the cash flows which is due to the timing of the payment – too late for inclusion in October. Either way, however, we’d expect Spain to be well supported this week.

- ECB’s QE resumes on Friday. There’s been a great deal of strategist coverage discussing the viability, duration, distribution and net market impact of the buying. We’ve sifted through a substantial amount of it and the conclusions we come to can be distilled down into a handful of bullet points:

- Of the Eur 20bn per month of buying, the market expect 14bn of it to be spent on EGBs.

- With the usual December lull already scheduled, the ECB is likely to front-load their purchases in Nov to cover the gap in December.

- The capital key was adjusted in late 2018 to reflect smaller net purchases of BTPS, SPGBs and FRTRs but even with these changes, the proportion of BTPS and FRTRs will remain high, especially when liquidity in the smaller issuers (RFGB, PGB, etc) is scarce.

- Lagarde has her hands full with the ECB’s hawkish contingent who have been challenging both the need for additional stimulus (both monetary and fiscal), suggesting heightened sensitivity to any signs of an improvement in the economy outlook and a shorter QE lifespan than expected. (Most dealers see at least 1year of operations.)

- With a handful of exceptions (JPM and MS this am) most pundits see renewed QE as a ‘sell vol, stay long flatteners and periphs’ trade. Question then becomes, how much is already priced in? (More on this soon)

More to come…

Mark

![]()

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Bloomberg Bond News Summary > Thu Oct 24th

Business Briefing

1) Daimler Zeroes in on Costs, Diesel Risk After Earnings Beat (1)

(Bloomberg) -- Daimler AG said it will intensify efforts to cut costs to manage the industry’s shift to electric vehicles after third-quarter earnings exceeded forecasts, despite weaker profitability from the Mercedes-Benz cars unit.

- The world’s biggest luxury-car maker -- reeling from two profit warnings this year partly related to diesel-emissions investigations -- also ...

2) Big Eurodollar Blocks Bet Fed Goes Small on Cuts: Markets Live

3) Nokia Cuts Earnings Outlook and Pauses Dividend to Invest in 5G

(Bloomberg) -- Nokia Oyj lowered its earnings guidance for this year and next and halted dividend payments as the rollout of 5G mobile networks is turning out to be more expensive and competitive than previously expected.

- The Finnish equipment company took down its earnings and margin expectations and said it won’t distribute dividends for the third and fourth quarters of ...

4) Stocks Rise in Asia With Nasdaq Futures on Profits: Markets Wrap

(Bloomberg) -- Stocks in Asia were mostly higher as investors took solace from a raft of earnings that provided some optimism against a background of concern that global economic growth lacks momentum. Treasury yields and the dollar were flat. Shares edged up in Hong Kong, Tokyo and Sydney, though gains fizzled in Seoul and Shanghai. The S&P 500 Index earlier climbed to ...

5) Aramco Said to Explore Incentives to Reward Loyal IPO Buyers (1)

(Bloomberg) -- Saudi Aramco is exploring ways to reward loyal investors in its initial public offering to ensure the record share sale isn’t followed by a wave of selling, people with knowledge of the matter said. One potential measure that Aramco has discussed with Saudi regulators is whether it could offer bonus shares to retail stock buyers who keep their holdings for ...

World News Briefing

6) Trump-Sanctioned GOP Protest Disrupts Impeachment Hearing

(Bloomberg) -- A group of Republicans disrupted a hearing of the Democrats’ impeachment inquiry Wednesday by storming into a secure room at the Capitol in a protest carried out with the blessing of President Donald Trump. The two dozen or so GOP House members are among some of Trump’s staunchest defenders in Congress, and at least some of them met with the president Tuesday ...

7) Californians Go Dark in Blackout That May Affect 1.5 Million

(Bloomberg) -- Parts of Northern California have gone dark in the first stage of a mass blackout that could eventually leave more than a million people across the state without power. PG&E Corp. has cut service to customers in counties near Sacramento and Napa Valley in an attempt to keep its power lines from sparking wildfires amid high winds. The blackout is set to ...

8) China’s Information War on Taiwan Ramps Up as Election Nears

(Bloomberg Businessweek) -- Holger Chen cuts a fierce profile with his skull-tattooed biceps, each bigger than a human head, and the oft-broken nose of a fighter. A mixed martial arts fighter, ex-Marine, former gangster, and owner of a chain of fitness clubs in Taiwan named after Genghis Khan, Chen has become an emblem of what he calls “defensive democracy” against disinformation from China. In his YouTube broadcasts, ...

9) Pompeo Cornered as Ukraine Envoy’s Testimony Forces Hard Choice

(Bloomberg) -- The acting U.S. envoy to Ukraine said he was told President Donald Trump wanted Ukraine’s president “in a public box” in order to get him to investigate Joe Biden’s son in exchange for military aid. Instead, it was Secretary of State Michael Pompeo who got boxed in. After the White House disparaged the testimony Tuesday by Ambassador William Taylor as the ...

10) EU Keeps Johnson Waiting for Brexit Extension He Doesn’t Want

(Bloomberg) -- The European Union left Boris Johnson hanging on Wednesday night as officials in Brussels debated whether to grant him a third extension to the Brexit process. EU ambassadors meeting in the Belgian capital agreed that they should accept the British prime minister’s request for more time but couldn’t settle on how long he will get, according to officials ...

Bonds

11) Sizzling Bond Demand Boosts Deals From Philippines to China

(Bloomberg) -- The Asian dollar bond market is sizzling as yield-starved investors load up on offerings including from the Philippines’ oldest conglomerate and a Chinese investment holding firm. The region’s credit markets have been rallying as global central banks keep interest rates low and some optimism has emerged on U.S.-China trade talks. ...

12) Huawei Defies Trade War Angst with Strong Yuan Bond Debut

(Bloomberg) -- Huawei Investment & Holding Co. sold its first bond in China at the year’s lowest coupon for a Chinese private firm’s note with the same tenor, reflecting strong domestic support for the company caught in the country’s trade crossfire with the U.S. The parent of tech giant Huawei Technologies Co. priced a 3 billion yuan ($425 million) three-year bond at ...

13) Top Fund Manager Builds Credit Portfolio to Bear Recession

(Bloomberg) -- Joshua Lohmeier’s debt fund at Aviva Investors has outperformed 94% of peers over the past year. With signs that a recession is nearing, he is playing those concerns by investing in bonds better insulated from a downturn, while keeping some riskier debt. “We prefer to have more BBB rated securities in shorter maturities and more defensive, higher-quality ...

14) Bond Defaults Are Highest on Record as India’s Economy Slows

(Bloomberg) -- Indian companies have defaulted on a record 76 billion rupees ($1.1 billion) of local-currency and international bonds so far this year after the shadow bank crisis triggered a credit squeeze, and it doesn’t look like the worst is over. Those firms that delayed or missed debt payments in 2019 still have the equivalent of $17 billion of notes and loans ...

15) Yen Rises as Weak Manufacturing Stokes Growth Fears: Inside G-10

(Bloomberg) -- The yen edged higher as a slew of weak manufacturing data underscored the slowing momentum in global growth.

- Yen rose as manufacturing indexes in Australia and Japan slumped to the lowest in three years and traders awaited a speech by U.S. Vice President Mike Pence which could reignite tensions with China

- The greenback slipped while other currencies were range-bound with investors on watch for ...

16) Asia Bond Issues to Stay High - Indonesia in a Sweet Spot: BoS

(Bloomberg) -- Dollar bond issues from Asia will remain high as many companies will look to refinance their debt to benefit from lower borrowing costs, according to Bank of Singapore Ltd.

- “Indonesia is in a sweet spot as the new government aims to boost infrastructure spending, while we also expect bond issues from Chinese property developers and energy companies and banks ...

Central Banks

17) Facebook’s Libra Shows Banks Can Do More, Singapore MAS Says (1)

(Bloomberg) -- Facebook Inc.’s embattled bid to create its own digital currency has laid bare shortcomings in cross-border payments and financial inclusion that banks and regulators must address, according to Singapore’s top central banker. Central banks “need to answer” the challenge posed by Facebook’s attempt to create a faster and more affordable payments network via ...

18) Japan Authorities Are Said to Team Up on Bank Stress Tests

(Bloomberg) -- Japan’s central bank and financial regulator are teaming up to test major banks’ resilience to mounting risks at home and abroad, people with knowledge of the matter said. The first-ever joint stress tests by the Bank of Japan and Financial Services Agency will require five lenders to measure their ability to withstand shocks such as a sharp economic ...

19) Singapore Central Bank Sees Small Inflows Amid Hong Kong Unrest

(Bloomberg) -- Hong Kong’s political turmoil has prompted some capital to move to Singapore though there hasn’t been a flood of inflows from the former British colony, according to Singapore’s central bank. The city state’s banks have seen an uptick in those inquiring about how to re-allocate assets, which is reasonable to expect, Ravi Menon, managing director of the ...

Economic News

20) Draghi Reaches End of His Fight to Save Euro: Decision Day Guide

(Bloomberg) -- European Central Bank President Mario Draghi will hold his final policy meeting and press conference on Thursday, after eight years of leading the fight to stave off a euro-zone breakup and the threat of deflation. For all his successes, it’s likely to be a day in which any congratulations are mixed with tough questions about the region’s brittle economy. ...

21) ECB’s Draghi to Call for Fiscal Review Before Exiting: Economics

(Bloomberg Economics) -- Mario Draghi’s tenure as president of the European Central Bank has been undeniably successful -- saying he saved the euro from collapse isn’t much of a stretch. However, inflation continues to languish well below target. And with monetary policy reaching the limits of its efficacy, we expect him to make a final plea today for help from Europe’s governments. ...

22) With U.S. Help, Global Growth in 2020 May Be Up From Dismal 2019

(Bloomberg Businessweek) -- To avoid a recession in the U.S. in 2020, households need to keep spending, peace needs to break out in global trade wars, and investors can’t get spooked—by the U.S. presidential election or anything else. It would also help if policymakers in Europe and China did their part to shore up growth, even though the tools they have to do so are limited. It’s likely that all these things will happen. That’s why Bloomberg Economics is ...

23) ECB Gets Chance for German Reset With Lagarde-Schnabel Dual Act

(Bloomberg) -- The European Central Bank and Germany finally have a window of opportunity to start repairing their fractured relationship -- for the first time in years. The German cabinet’s proposal of Isabel Schnabel to join the ECB’s Executive Board will give the institution an academic economist with a track record of defending its monetary stimulus against attacks by ...

24) Singapore’s Central Bank Chief Sees Slow Economic Recovery

(Bloomberg) -- Singapore’s economy may be a few quarters away from a recovery as the decline in trade and manufacturing this year hasn’t really spread to other sectors, the central bank’s chief said. The Monetary Authority of Singapore’s baseline view is that “the current cycle should be bottoming out toward the end of the year and into next year,” Managing Director Ravi Menon ...

European Central Bank

25) Final Countdown to Draghi Features Five Rate Decisions in Region

(Bloomberg) -- Mario Draghi’s farewell press conference as European Central Bank president will cap a morning of monetary action across the region that illustrates the struggle for policy makers in coping with a worsening global outlook. The five decisions due on Thursday start with Sweden’s Riksbank, whose efforts in exiting the twilight zone of negative interest rates are ...

26) PRECIOUS: Gold Holds Advance Ahead of Draghi’s Final ECB Meeting

(Bloomberg) -- Gold held a gain as investors await European Central Bank President Mario Draghi’s final policy meeting and press conference on Thursday. Traders were also weighing the latest Brexit developments as well as a raft of earnings. About 80% of companies on the S&P 500 have topped expectations for profits, though Texas Instruments and Caterpillar both showed ...

Federal Reserve

27) Fed to increase repo market interventions again ahead of month-end

Preview text not available for this story.

28) Federal Reserve of New York: Statement Regarding Repurchase Operations

29) Fed New York: Statement Regarding Repurchase Operations Oct 23, 2019

Statements and Operating Policies Statements announcing changes to the operating polices for conducting open market operations. Oct 23, 2019 Statement Regarding Repurchase Operations END

30) Trump Fed Nominees Still Work in Progress: Senate Banking Chair

(Bloomberg) -- President Trump’s picks to serve in two slots at the Federal Reserve remain a “work in progress,” and it’s not certain when they will be formally nominated and sent to Capitol Hill, Senate Banking Committee Chairman Mike Crapo says.

- “I don’t have any update,” Crapo says in an interview when asked about the status of Trump’s Fed picks made last July

- “I would ...

First Word FX News Foreign Exchange

31) ANZ Is Constructive on Rupiah Bonds in Near Term Amid Low Rates

(Bloomberg) -- ANZ Bank is “constructive” on Indonesian bonds in the near term amid low rates globally, which help ease concerns of the nation’s structural issues, Jennifer Kusuma, co.’s senior rates strategist in Singapore, writes in a note.

President Jokowi’s cabinet choices have rekindled hopes for economic reform and the sale of the $1b of 30-year dollar bonds reduced ...

![]()

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

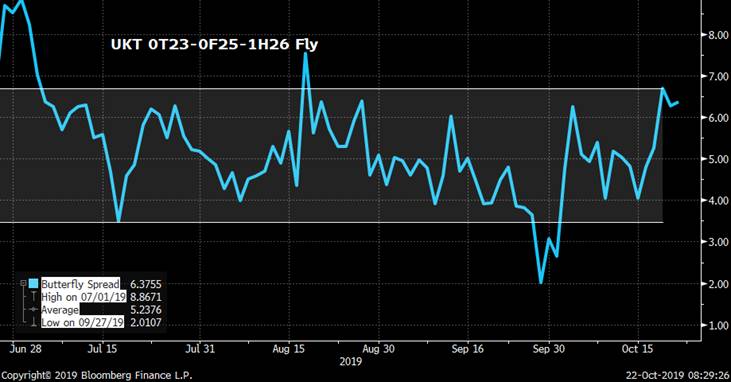

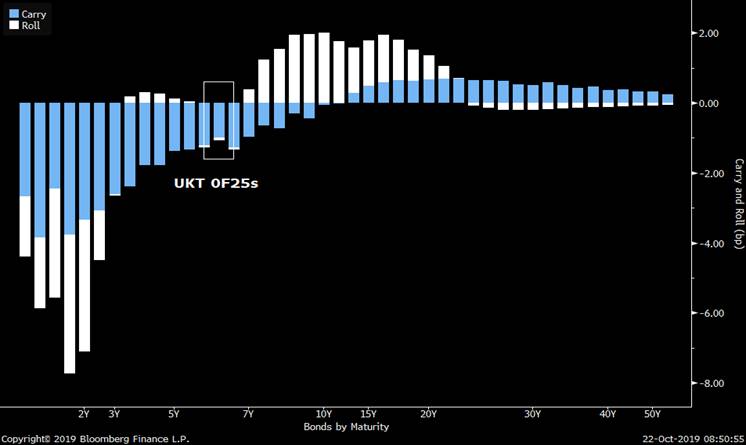

MICROCOSM: GILTS > Steepeners Into UKT 0F25s Tap This AM...

GILTS > 0F25s Tap @ 10:30

TRADES > STEEPENERS – 0F25 vs 225, 0F25 vs 1H26 and 0F25 vs 1Q27 – see below.

> Third tap of the issue takes them to £12.4bn, about 1/2 way through their cycle.

> 0F25s have cheapened almost 5bps vs SONIA since early Oct and the 0T23- 0F25-1H26 fly is +6.2bps mid, about .5bps richer than this time yesterday.

> Broadly speaking, we like steepeners in the 3-7yr sector, not just because it's still remarkably flat but with Brexit's outcome now between either a deal or an extension, rather than a deal or no-deal, the medium term bias for GBP/UKT rates should be higher which should steepen the curve. Add to that the easing in 225 and 1H26 repo over the last 2 weeks and shorting these issues isn't as punitive, opening the door for a normalization of the curve. Coming into this morning , 0F25 vs 225s is 6.9bps inverted and 0F25 vs 1H26s is 2.8bps inverted – both a reflection of the repo differentials. As we can see from the BBG CCS page below, a repo differential of 25bps (borrowing 225s at 0.50% vs lending 0F25s at 0.75%) costs .3bps over a month and .66bps until Dec 31st. Punitive, yes, but given the volatility we’ve seen in SONIA (4y1y cheapening over 30bps since Oct 10th) we’re willing to bet we won’t have time to worry about carry and roll. If you’d prefer to play it safe, sell the 1Q27s instead – also flat vs 0F25s on Z-sprd and close enough to the 1F28s (G Z9) to be dragged cheaper in a sell-off.

Gilts curve carry and roll…

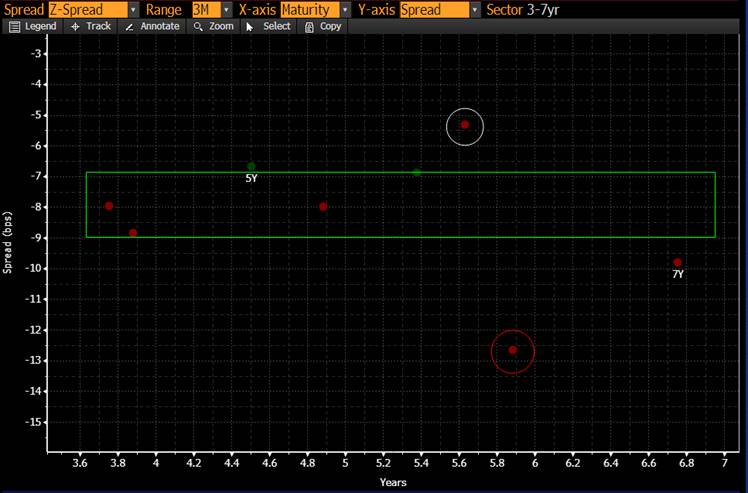

3-7yr sector Z-sprds – 0F25s circled in white, 225s circled in red.

![]()

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Bloomberg Bond News Summary > Tues Oct 22

Business Briefing

1) Trudeau Claims `Clear Mandate' Despite Losing Majority: TOPLive

2) Facebook, Amazon Set Lobbying Records Amid Washington Scrutiny

(Bloomberg) -- Facebook Inc. and Amazon.com Inc. set federal lobbying records in the third quarter as Washington ramps up oversight of the tech giants’ business practices. Facebook spent $4.8 million, an increase of almost 70% from the same period the year before. The world’s largest social-media company is grappling with a mushrooming list of challenges, including federal ...

3) China’s Central Bank Boosts Liquidity Ahead of Tax Payment Surge

(Bloomberg) -- China’s central bank used open-market operations to inject the largest amount of cash into the banking system since May, as upcoming corporate tax payments tighten liquidity conditions. The People’s Bank of China on Tuesday net injected 250 billion yuan ($35 billion) via seven-day reverse repurchase agreements, according to a statement. There were no ...

4) Climate Change ‘Defining Issue of Our Times,’ Singapore Says

(Bloomberg) -- Land-scarce, low-lying and increasingly hot Singapore is going to have to find room for more than a quarter of a million new trees and shrubs as the city-state steps up measures to respond to climate change. “Citizens around the world have come to recognize climate change for what it is -- the defining issue of our times,” Masagos Zulkifli, minister for the ...

5) Infosys Dives Most in 6 Years as Whistle-Blowers Target CEO

(Bloomberg) -- Infosys Ltd.’s shares plunged to a 10-month low after whistle-blowers accused Chief Executive Officer Salil Parekh of leading an effort to shore up profits through irregular accounting, turning up the heat on an IT services giant that endured internal turmoil just two years ago. The stock fell as much as 16% Tuesday, wiping out 2019’s gains via its biggest intraday ...

World News Briefing

6) Boris Johnson Finally Gets to Put His Brexit Deal to the Vote

(Bloomberg) -- Prime Minister Boris Johnson will find out Tuesday evening whether he has any chance of getting his Brexit deal through Parliament -- and whether he can do it ahead of his Oct. 31 deadline. Having twice been denied a vote on whether members of Parliament support his deal, Johnson has introduced the Withdrawal Agreement Bill, which would implement the deal in ...

7) Trudeau Overcomes Scandals to Win Second Term in Canada Election

(Bloomberg) -- Canadian Prime Minister Justin Trudeau won a second term in national elections, displaying once again a remarkable ability to overcome scandal and controversy to remain in power. Trudeau’s Liberal Party won or was leading in 155 of Canada’s 338 electoral districts, losing his majority in parliament but gaining enough seats to secure a stable government with ...

8) Democrats Seek Insider Trading Probe After ‘Trump Chaos’ Article

(Bloomberg) -- Democratic lawmakers are increasingly demanding that U.S. authorities investigate allegations raised in a recent magazine article that traders might be using non-public government information to reap huge illegal profits, even as the exchange where the transactions purportedly took place called the story “patently false.” In a Monday letter, 14 Democratic senators urged the heads of the Justice Department, FBI, ...

9) Latin American ‘Oasis’ Shaken by Worst Unrest Since Dictatorship

(Bloomberg) -- Just weeks before the worst civil unrest since Chile returned to democracy 29 years ago, President Sebastian Pinera described the country as “a true oasis” amid Latin American turmoil. The billionaire investor-turned-politician isn’t alone in his glowing assessment of a country that regularly tops regional prosperity metrics. However, the deadly upheaval of ...

10) Juul Spent Record $1.2 Million Lobbying as Regulators Stepped Up

(Bloomberg) -- Juul Labs Inc. spent a record $1.2 million on federal lobbying during the third quarter as the largest U.S. e-cigarette maker faced threats that many of its products would be banned following an increase in lung illnesses linked to vaping. The company’s lobbying spending during the three months ending Sept. 30 more than doubled from $560,000 in the same ...

Bonds

11) Chinese Luxury Giant’s Troubled Bonds Rally on Debt Cut Plan

(Bloomberg) -- Dollar bonds of Chinese luxury clothing giant Shandong Ruyi Technology Group Co. extended a rally amid plans by the company to reduce some of its debt burden. Shandong Ruyi plans to buy back some of its dollar bonds at an “appropriate time”, Su Xiao, president of Ruyi Holding Group, a shareholder, said at an investor meeting held in Hong Kong on Monday. This ...

12) Treasury Futures Steady, Cash Markets Closed For Japan Holiday

(Bloomberg) -- Treasury futures flat from the open after sliding on Monday on weakness in gilts and with S&P 500 hitting 3,000 amid positive signs on trade talks. Cash USTs and JGB markets closed in Asia due to holiday in Japan. Large Aussie government bonds redemption may continue to support front-end.

- Cash USTs to open at 7am London. U.S. supply kicks off Tuesday with new 2-year for $40b ...

13) Citadel Securities Hires Citigroup’s Wang for Treasuries

(Bloomberg) -- Citadel Securities hired Citigroup Inc.’s Kelly Wang to spearhead fixed-income sales from Hong Kong as billionaire Ken Griffin’s market-making behemoth further expands its Treasuries trading reach in Asia. Wang spent over six years as Citigroup, most recently as head of greater China investor foreign-exchange sales in Hong Kong. Prior to that she worked at ...

14) JPMorgan Warns U.S. Money-Market Stress to Get Much Worse

(Bloomberg) -- JPMorgan Chase & Co. says the money-market stress that sent short-term borrowing rates surging last month is likely to get much worse despite the Federal Reserve’s attempts to inject billions of dollars into the financial system. The Fed has offered overnight loans and started buying up to $60 billion of U.S. Treasury bills a month in an effort to ease ...

15) Currencies Mixed as Trump Trade Comments Weighed: Inside Asia

(Bloomberg) -- Emerging Asian currencies consolidated after recent gains as investors wait on details from U.S.-China trade talks.

- President Donald Trump said China has indicated that negotiations over an initial trade deal are advancing, raising expectations the nations’ leaders could sign an agreement at a meeting next month in Chile

- China’s central bank added 250 billion yuan ($35 billion) into the banking system, the ...

16) Emerging Markets Are Next ‘Asset Bubble’ Amid Yield Hunt, Debt

(Bloomberg) -- A look at the price action and you’d be forgiven for thinking all was well in emerging markets. Far from it. While indexes of stocks, bonds and currencies hover around their strongest levels since early August, political crises from Ecuador and Argentina to Turkey, South Africa and -- most recently -- Chile and Lebanon ...

Central Banks

17) PBOC Injects Largest Amount in Open Market Operation Since May

(Bloomberg) -- The People’s Bank of China will inject 250b yuan into the banking system using 7-day reverse repurchase agreements, according two traders at primary dealers.

- The net injection of 250b yuan in open market operation is the largest amount since May 29: Bloomberg calculation

- PBOC gauges demand for 7-day, 14-day, 28-day and 63-day reverse repos for Oct. 23, ...

18) Bonds at Risk as Central Banks Eye End to Easing: Markets Live

19) Hungary to Hold Policy in Wait for CPI Trend: Decision Day Guide

(Bloomberg) -- Hungary’s central bank will probably stay put after a modest easing step last month, as a slowing world economy tempers the impact of a tight labor market. The Monetary Council is set to keep its overnight-deposit interest rate and the base rate at -0.05% and 0.9% respectively, according to a Bloomberg survey. With rate setters in a self-defined “data-driven” ...

20) Three Words, 11 Million Jobs: Draghi’s Euro-Area Economic Legacy

(Bloomberg) -- Three words -- whatever it takes -- defined Mario Draghi’s time as European Central Bank president, but he’s prouder of another number: 11 million jobs. Hardly a public appearance goes by without Draghi mentioning employment growth in the euro zone as a justification for the extraordinary monetary stimulus he’s pushed through since 2011. ...

21) GERMANY INSIGHT: Trouble Ahead as Economy Skirts With Recession

(Bloomberg Economics) -- Growth has slumped in Germany reflecting a turn in the global investment cycle, a lack of clarity over global trade and turmoil in the autos industry. Leading indicators suggest 2020 will begin on a weak footing and the risk is of a deeper downturn. If U.S.-EU trade negotiations flounder, Germany would take a big hit -- a recession worthy of the name could be unavoidable. ...

22) [Delayed] European Daily Focus: Tuesday, 15th October 2019

Abstract: TOP STORIES COCA-COLA EUROPEAN PARTNERS (CCEP.N) - Proving growth is sustainable Andrea Pistacchi: Tgt EUR62.00 to EUR65.00. Last Close EUR56.51, Buy. The soft drinks space in Europe is vibrant and innovation in the Coke ...

Economic News

23) Political Risk Revived in Latin America as Protests Spread

(Bloomberg) -- Latin America, the traditional poster child for political risk in financial markets, is back as a source of concern for investors. Chilean President Sebastian Pinera on Saturday became the second leader this month to declare a state of emergency, his hand forced by violent protests in South America’s wealthiest country after an increase in transportation ...

24) RBI Easing, Tax Cuts to Bring India’s 2020 Recovery : Economics

(Bloomberg Economics) -- India’s growth recovery, which has been a long time coming, finally seems to be around the corner. By next year, the economy should see rising rural incomes, better transmission of central bank’s easing, and higher post-tax corporate profit. Combined, these should aid a revival of consumer and investor sentiment. The turnaround in the economy is likely to show up from the October-December quarter, ...

25) Taxing the Rich to Fund Welfare Is Nobel Winner’s Growth Mantra

(Bloomberg) -- How do you spur demand in an economy? By raising taxes, not cutting them, says this year’s winner of the Nobel prize for economics. Reducing taxes to boost investment is a myth spread by businesses, says Abhijit Banerjee, who won the prize along with Esther Duflo of the Massachusetts Institute of Technology and Michael Kremer of Harvard University for their ...

26) Riksbank to Cling to Hiking Plan in Bet Recession Will Be Dodged

(Bloomberg) -- Swedish central bank policy makers are intent on leaving negative interest rates behind after almost half a decade. But faced with a barrage of bad economic data, Governor Stefan Ingves and his colleagues will on Thursday likely delay a plan to tighten at the turn of the year further into 2020. They’re betting the largest Nordic economy will avoid an outright recession as the Federal ...

27) GM Workers at Tennessee Plant Narrowly Reject UAW Contract Deal

(Bloomberg) -- United Auto Workers members at a General Motors Co. plant near Nashville, Tennessee narrowly gave a thumbs down on a proposed contract to end a more than five-week old strike — an early indication that rank-and-file approval of the tentative deal could be close. In one of the first votes by a major union local, the Spring Hill assembly’s 3,300 unionized ...

European Central Bank

28) 11 Million Jobs May Be Draghi’s Euro-Area Economic Legacy: Chart

(Bloomberg) -- Three words -- whatever it takes -- defined Mario Draghi’s time as European Central Bank president, but he’s prouder of another number: 11 million jobs. Hardly a public appearance goes by without Draghi mentioning employment growth in the euro zone as a justification for the extraordinary monetary stimulus he’s pushed through since 2011. The focus on jobs might be understandable given that, ...

29) ECB Added Three New Securities to CSPP Last Week

(Bloomberg) -- The ECB added three new securities to its CSPP program during the week ended Oct. 18, according to central bank data analyzed by Bloomberg.

- Four securities were removed and the value of the CSPP portfolio decreased by EU6m, at amortized cost

New Holdings Removed Holdings

- CSPP ISINs as determined by Bloomberg using ECB website data at 2:45am London on October ...

30) Draghi’s Homeland Among Worst on Growth During His Term: Map

(Bloomberg) -- When analyzing the economic successes and failures of Mario Draghi’s eight-year term as European Central Bank president, regional differences are striking. Aside from Greece and Cyprus -- both deeply scarred after years of austerity and a near-collapse of their financial system -- no country has done worse than Draghi’s native Italy in terms of total output per head.

31) Draghi: the Words and Actions Which Defined His Tenure (Video)

32) ECB's QE Restart to Require More Private Debt Buying

(Bloomberg Intelligence) -- The European Central Bank is running low on sovereign bonds to buy -- that undermines the credibility of its pledge to keep going until inflation picks up. The easiest way to ensure the program can run without changing its self-imposed guidelines is to lean more heavily on private debt. If inflation takes two years to firm, the ECB could face a shortage of about 60 billion euros in debt during the ...

Federal Reserve

33) Federal Reserve ‘the Largest Driver’ of Mortgage Weakness: Pimco

(Bloomberg) -- The Federal Reserve is ‘the largest driver” of weakness in the MBS market, Pimco’s Mike Cudzil and Dan Hyman wrote in a blog post.

- Since October 2017 the central bank has been allowing MBS on its balance sheet to run off at a maximum of $20b/month

- Should it end this process and reinvest the roll off proceeds back into MBS, it would benefit homeowners, buyers ...

34) Fed’s Bowman Says Central Banks Should Lead Push for Diversity

(Bloomberg) -- Federal Reserve Governor Michelle Bowman says central banks have a responsibility to be leaders in increasing diversity and inclusion in the fields of economics and finance.

- Bowman delivers pre-recorded closing remarks to a joint Bank of England, Federal Reserve Board and European Central Bank conference on gender and career progression in Frankfurt

- Bowman doesn’t comment on monetary policy or her outlook for the U.S. economy in the ...

(Business Insider)

- Money market stress isn't likely to be calmed by recent Federal Reserve capital injections, and will likely get worse through the end of the year, JPMorgan Chase analysts wrote.

- The Federal Reserve began monthly purchases of $60 billion worth of Treasurys, but the capital will likely remain with primary lenders when non-primary firms are the ones that need it most, the ...

36) U.S. Prime-Age Worker Wage Growth Is Welcome Sign for Fed: Chart

(Bloomberg) -- The American consumer remains king of an economy that received another piece of bad news last week on the manufacturing front. A look at full-time prime-age workers’ earnings helps explain why. The labor market’s tightening is generating faster wage growth, with minorities enjoying the largest year-over-year pay improvements. Such increases are likely to be welcomed by Federal Reserve policy ...

First Word FX News Foreign Exchange

37) Hedge Funds Use Brexit Delay to Top Up Option Cover, Traders Say

(Bloomberg) -- Hedge funds have been using the delay in a planned Brexit vote by the U.K. parliament to load up on topside cover as their conviction that there will be a deal increases, Asia-based FX traders say.

- Many funds are carrying large long gamma positions via call spreads and outright calls should spot GBP/USD rise between 1.31 and 1.34

- GBP/USD options with a combined notional face value of GBP2.46b at strike 1.3150 expire ...

38) Benchmark Bonds Decline on RBI Stock Switch: Inside India

(Bloomberg) -- Benchmark sovereign bonds drop as govt is set to switch 200b rupees of shorter debt to longer tenor paper via an auction. Rupee gains most among Asian peers after an extended weekend.

- Govt to switch 200b rupees of bonds to 6.45% 2029 debt via auction on Oct. 24

- RBI’s monetary policy minutes released late Friday was unanimous in keeping rates lower for longer ...

39) Cautious Optimism Supports Holiday-Thinned Stocks: Macro Squawk

(Bloomberg) -- S&P futures inch 0.2% higher as most Asian indexes gain; Kospi jumps 1.2%, ASX 200 index 0.4% stronger. T-note futures flatline with cash Treasuries closed for Japan holiday; Aussie curve bear steepens after 10-year yield adds 3bps. Bloomberg dollar index hovers near three-month low; kiwi extends recent outperformance, loonie little changed after Canada election. Yuan marginally softer after PBOC injects 250b yuan ...

![]()

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

BOND AND BREAKEVEN : YIELDS TO HEAD HIGHER! WE ARE VERY CLOSE TO A FULL ON YIELD RALLY.

BOND AND BREAKEVEN : YIELDS TO HEAD HIGHER! WE ARE VERY CLOSE TO A FULL ON YIELD RALLY. WE ARE NOW TESTING MANY 100 DAY MOVING AVERAGES WHICH IF BREACHED WILL COMFIRM A MAJOR YIELD HIGHER CALL.

IT DOES APPEAR WE WILL HEAD HIGHER IN YIELD FOR SOME PERIOD OF TIME.

BONDS :

IT IS NOW LOOKING LIKE A REASONABLE YIELD BASE HAS GONE IN AIDED BY THE BREAKEVEN SECTOR.

US BREAKEVENS AND USGGT :

GIVEN THE NATURAL CORRELATION WITH CORE YIELDS THE MARKET SHOULD BOUNCE ALONG WITH YIELDS.

ASTOR RIDGE : Independent Ideas, Research, Liquidity, Anonymity and Trusted Experience.

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

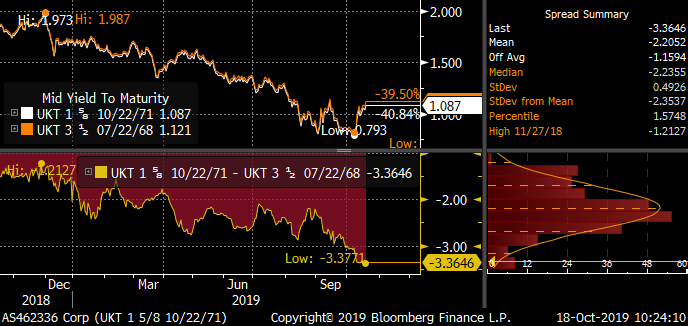

UKT 65s68s71s fly - dislocated belly cheapening

Here’s a stable RV trade with low VAR/beta to Brexit risks:

TRADE: Buy $50k/01 of UKT 65s68s71s at +3.75 bps

TARGET: 1.75 bps (+2bp)

STOP: 4.75 bps (-1bp)

This micro fly 65s68s71s is at extreme levels, and has decoupled from the 30s50s curve (magenta):

Carry is flat vs a 5bp repo spread; £38.75k ($50k/01) position consumes only £31.2mm gross / £3.6mm net notional balance sheet:

The next fly in the curve, 60s65s68s, trades over 5bps richer:

The dislocation is being driven by the 68s71s leg, which has been bull flattening:

Whereas the 65s68s curve (blue) has recently steepened:

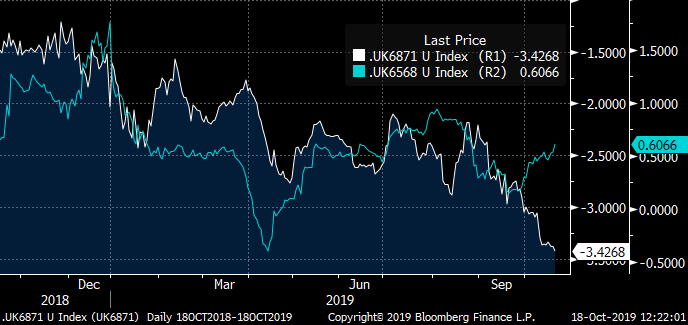

71s stand out as very rich on the Sonia ASW curve – they are richer than UKT 1.75 9/37 which are 34 years shorter:

The last time UKT long end micro RV was this dislocated was in 2016, when the 55s60s65s fly traded -4bps, only to correct 4 bps within the year:

Why is the trade there?

- UKT 71s pay a coupon on 10/22, much of which will be reinvested in same issue for passive managers (coupon payment total = £92mm = £411k/01 in risk terms)

- Convexity – we’ve just had a 30bps back up in ultras; the 65s68s71s would have lost 0.3bp in rehedging cost over this move (i.e. 0.1bp per 10bp move in yields)

- There have been several corporate pension buy-ins in (where pensions sell their LDI portfolio to an insurer in exchange for a guaranteed annuity). De-risking activity has picked up in front of Brexit. This is because Insurers are allowed to take more risk than pensions to hedge their liabilities. Last night Walmart/ASDA announced the completion of a £3.8bn deal:

The American owner of Asda has struck a deal to offload nearly £4bn of the UK-based supermarket chain's pension liabilities, removing a hurdle to a standalone stock market listing.

Sky News has learnt that Walmart and Asda's pension trustees have agreed a £3.8bn pension buy-in with Rothesay Life, a specialist insurer of corporate retirement schemes.

https://news.sky.com/story/asda-owner-walmart-clears-path-to-float-with-4bn-pension-deal-11837972

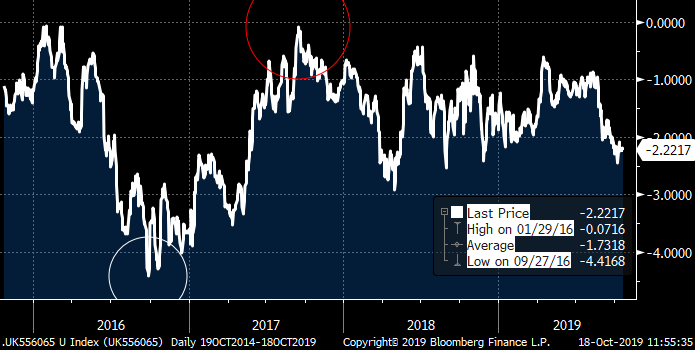

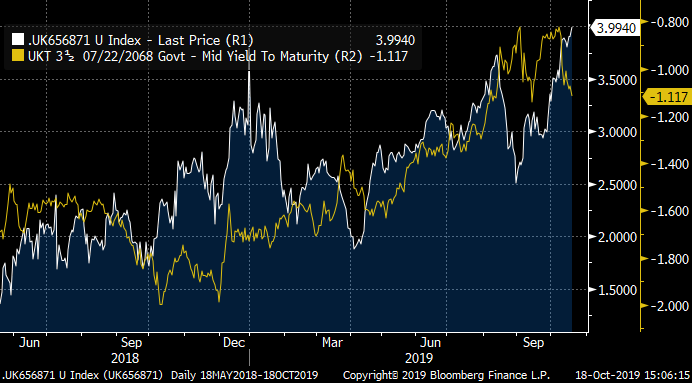

When insurers (who are not required to hedge inflation) take over DB pension assets (who are required), they often sell out of long linkers (which trade at ridiculous real yields near -2%) and replace them with nominals; this could explain the recent narrowing of long end break-evens:

UKT 68s Break-evens

When ultra long nominals are bought, the 71s tend to outperform given they are the current 50yr benchmark and the only 50+ yr Gilt.

Moreover, the 68s might be passed over in LDI programs given their high price and coupon, which makes them more attractive to income investors.

What catalyst will correct the trade?

Either 1) Income investors will come in at month end, recognising the historical cheapness of 68s, or

2) 71s will get sold into the market over time, cleaning up dealer shorts, as LDI needs move toward the 25-40yr sweet spot with the ongoing shift towards DB and flexible drawdown pensions

What happens to the trade in a no deal Brexit?

The fly has bull cheapened, but did not richen in the recent sell-off due to recent LDI activity:

Yellow – UKT 68s yield (inverted)

The fly cheapened 0.7 bps during the Nov 2018 Brexit flareup but then richened 0.85 bps during the March 2019 Brexit countdown, so there doesn’t seem to be a strong correlation to Brexit risk.

The UKT 68s yield bottomed recently at 0.80, near the current base rate; while a no deal Brexit could see ultra rates test 0.50, the curve would likely bull steepen due to the inflation shock caused by GBP weakness, which would cheapen ultras in general and the 71s (50yr benchmark) in particular, arresting further cheapening in the 65s68s71s fly.

Jim Lockard

Founder / Managing Partner

![]()

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 12 EAST 49th Street, New York NY 10017

Office: +44 (0) 203 -143 - 4172

Mobile: +44 (0) 7795-027-865

Email: jim.lockard@astorridge.com

Website: www.astorridge.com

This commentary was prepared by Jim Lockard, a Managing Partner at Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and it should be treated as a marketing communication even if it contains a research recommendation. A history of his commentary can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge does not engage in market making or proprietary trading, and has no position in any security discussed in this e-mail. The views in this e-mail are those of the author(s) and are subject to change.. Any recommendations contained herein reflect solely those of the author and were prepared independently of Astor Ridge or its affiliates. This publication does not constitute personal investment advice and may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate recommendations discussed herein. Actual investment returns may fluctuate as a result of changes in economic and market conditions (including market liquidity). Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by us is owned by us.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796