Today's BREXIT BARRAGE! Quid Pro Quo?

FT: Boris Johnson widens breach in Tory Eurosceptic ranks

FT: FT readers: which Brexit option do you think the UK should take?

FT: Business leaders back ‘Common Market 2.0’ deal after Brexit

TEL: The people’s day of jubilation has been hijacked by spineless pirates

TEL: Sadly, I must abandon my heart for my head and vote for this accursed Withdrawal Agreement

TEL: Eurosceptics ready to throw their support behind May’s deal to avoid ‘losing Brexit’

TEL: Theresa May warned 20 Remain ministers will quit unless she gives them free votes on softer Brexit

TEL: Why should Tory MPs stick to their manifesto? Theresa May hasn’t

BBG: May’s Brexit Deal Wins Support – But the Price Might Be Her Job

BBG: Meet the Revolutionaries Upending Theresa May’s Brexit Plans

BBG: Here’s How Parliament Plans to Take Control of Brexit

BBG: These Are the Brexit Options That British MPs Are Suggesting

BBG: A Boycott Is the Underpriced Risk of a Second Brexit Vote

BBC: MPs prepare for votes in bid to break deadlock

BBC: The lowdown on MPs’ alternative plans

BBC: MPs set out plan to consider alternatives to PM’s deal

More to come!

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

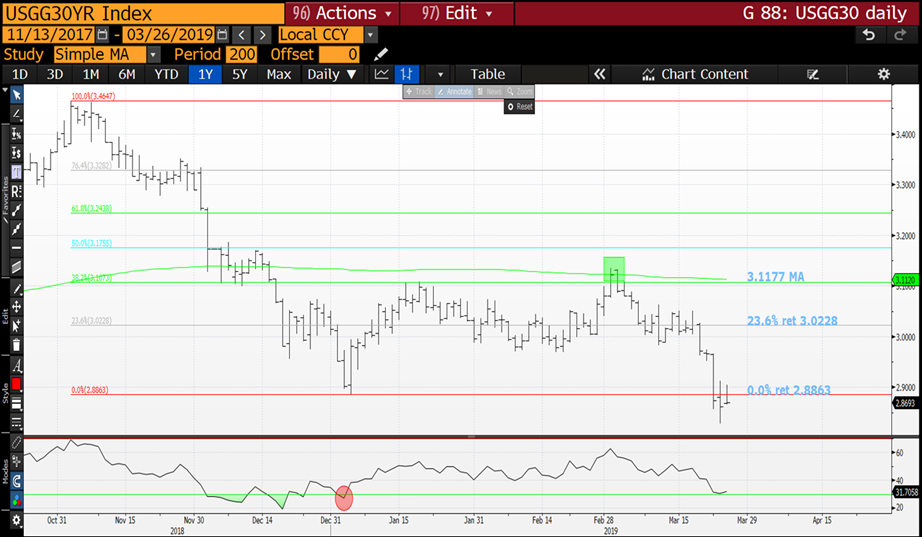

BOND YIELD (SHORT-TERM) UPDATE : There has been a decent run lower in yields but for those more short-term players the daily RSI’s are oversold.

BOND YIELD (SHORT-TERM) UPDATE : There has been a decent run lower in yields but for those more short-term players the daily RSI’s are oversold.

We also have supply this week and stocks seem very reluctant to join yields. The LONGTERM charts remain unaffected.

**REMEMBER CTAs KEEP buying for their trend-momentum returns irrespective of yield levels.**

The long-term quarterly-monthly charts continue to forecast MUCH lower yields and little obstacles in their path!

On paper the quarterly and monthly charts are obvious, its MUCH lower yields. We are failing MANY RARE 50 and 100 period moving averages aided by RSI dislocations that date back to 1980’s. The formations are staggering given the previous upsets in and around 2000 - 2007.

It seems from a chart perspective everyone is convinced rates are going MUCH HIGHER based on the HISTORICAL RSI dislocations. Expectation and positioning is way too optimistic.

The weekly charts are more optimistic for a HOLD but daily negate that almost instantly.

Daily charts have persisted in remaining sub numerous 200 day moving averages, so ideally its all a matter of time.

Germany and UK also point to lower yields, whilst Italy is pausing at a recent low.

ASTOR RIDGE : Independent Ideas, Research, Liquidity, Anonymity and Trusted Experience.

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

EQUITIES SPECIAL AKEY WEEK! : EUROPE HAS TOPPED NICELY WHILST THE US MARKET CURRENTLY STRUGGLES TO FOLLOW SUIT.

EQUITIES SPECIAL A KEY WEEK! : EUROPE HAS TOPPED NICELY WHILST THE US MARKET CURRENTLY STRUGGLES TO FOLLOW SUIT. THIS IS A VERY SIGNIFICANT QUARTERLY CLOSE, HOPEFULLY AT LOWER LEVELS THAN THESE.

THE US EQUITIES REMAIN SUB MOST IMPORTANT LEVELS, THUS SOME HOPE. WE NEED A WEAK CLOSE INTO QUARTER END.

THE US MARKET IS IN A VULNERABLE SITUATION, ACROSS ALL DAILY CHARTS THE RSI IS HEAVILY DISLOCATED AND FAILING NUMEROUS 200 DAY MOVING AVERAGES.

ONE THING STRIKES ME IS NO ONE IS DISCUSSING A MULTI YEAR TOP NOR DARE MENTION THE WORD “BEAR MARKET”. PERCEPTION IS WE SURVIVE AND THE LATEST BOUNCE ENDORSES THAT. THE PROBLEM IS THE LATEST BOUNCE WAS TOO FAST AND OF LITTLE SUBSTANCE.

THE RUSSELL IS ONE OF THE WEAKEST US MARKETS OUT THERE AND NASDAQ MUST ALSO BE ON THE RADAR.

ASTOR RIDGE : Independent Ideas, Research, Liquidity, Anonymity and Trusted Experience.

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

MICROCOSM: Brexit, the Long-End APF and Some Gilts Laggards

Quick recap of this am’s BBG chat for those who never read our chat… 😉

EARLY GBP Rates...

> It's a stretch to say the events of last night are a 'positive' for the Brexit outcome but at least something is happening that could hasten an outcome before Friday.

> SONIA for the Mar '20 MPC meeting closed at .658% last night, 9.2bps through the current base rate and 4.7 through O/N Sonia, which ostensibly prices in about 20% odds of a rate cut. We've sold off about 2bp this am on a seller of 4k L H0 just after the open on what we'd assume to be profit taking.

> Needless to say, the market's still in 'deer in the headlights' mode given Brexit and sister mkt performance. Perhaps it's foolhardy to suggest a meaningful directional short here, however, G-7 rates have A LOT of bad news built into the market right now, leaving little room for a positive shift in Brexit, stocks or data

UKT 124-4Q27 sprd nosedived in this rally…

APF Roulette

> So, the first long-end APF operation this cycle was on Mar 12th where the BoE bought a huge chunk of UKT 4H34s. Not a big shock considering their M.O. has been to buy the shortest issue in the basket in previous ops.

> Last week. however, they lifted ~1.1bn UKT 1T57s, about £1.5mm/01 more risk than the week before which also coincided with a 2.5bps flattening of UKT 47-57s in the ensuing week. Sure, there were other factors at work too but it's plain to see that if something's cheap, they'll buy them (assuming someone offers them) and the market’s left to deal with the consequences.

> It’s also relevant from a pure risk standpoint. In G M9 terms, £1.1bn UKT 1T57s is 30.1k equivalents, a lot different than the 16.9k G M9 the week before.

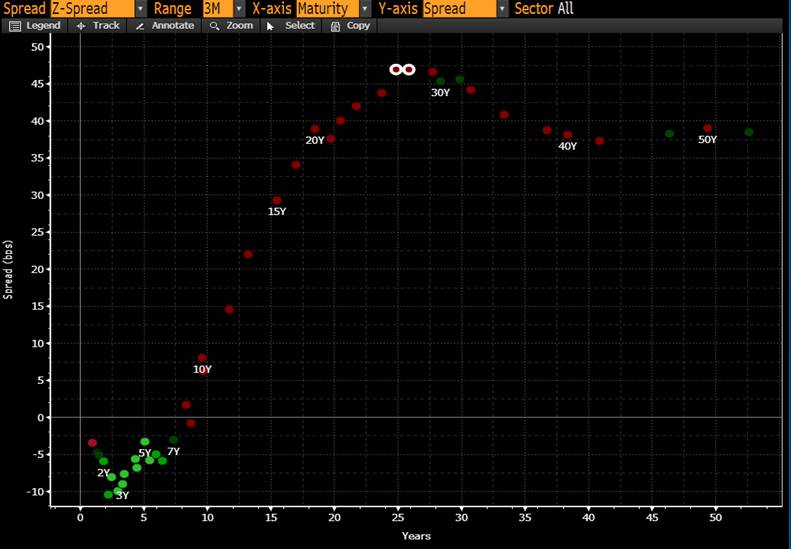

> From an RV perspective in the 15yr+ basket, the UKT 44-49s sector trades cheapest to the curve into this am. We've been buyers of this sector in the last week or so, not necessarily trying to game the APF but just in light of where they trade on the Z-sprd curve after the recent move in ultras.

UKT Z-Sprd curve… 44s and 45s circled in white

The Laggards…

- The gilts curve is all over the map right now as the market tries to balance APF flows with macro demands. That creates dislocations that we think are worth investigating, particularly since liquidity is still ample to enter/exit these positions efficiently. Here are some that stand out:

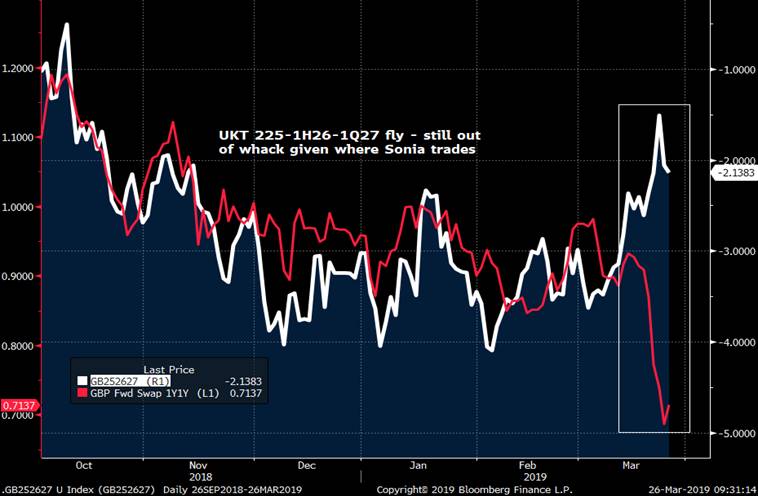

UKT 1H26s have cheapened up significantly over the last week as highlighted in yesterday AM’s note. The rally in SONIA exacerbates this dislocation and with the APF tomorrow we think the 26s are still too cheap, even after yesterday’s bounce.

UKT 124 v UKT 225 sprd came within .5bps of inverting yesterday, now just +.8bp. APF influence is obvious here with the BoE lifting a big chunk of them every week now. This will fade over the next couple weeks though.

More to come…

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Today's BREXIT BARRAGE... Will She Stay or Will She Go?

One million marched and MPs met – so many outcomes, so little time. At the very least it should be another in a long line of interesting weeks!

TEL: David Lidington and Michael Gove deny they will replace Theresa May in coup over Brexit

TEL: Cabinet told to oust Theresa May in order to rescue Brexit

TEL: Theresa May’s Government is ‘chicken’ and has ‘bottled it’ over Brexit, Boris Johnson says

TEL: How Theresa May rebuffed calls to set resignation date over ‘frank’ Chequers summit over Brexit

TEL: Why Norway plus gives Britain the time it needs to get out of its Brexit mess (Varoufakis)

TEL: Philip Hammond says second Brexit referendum ‘deserves to be considered’

TEL: Public confidence in the Conservatives must be in free-fall

TEL: So much for ‘taking back control of our borders’ – most immigrants come from outside the EU

TEL: We need a new leader who will believe in the UK – not embarrass it

BBC: Cabinet to meet amid pressure on May

BBG: May Faces Endgame as U.K. Leader Is Losing Control of Brexit

BBG: ECB’s Rehn Says Brexit Poses Biggest Short-Term Risk

BBG: Revoke Brexit? Don’t Hold Your Breath

BBG: Varadkar Confident of Keeping Border Invisible in No-Deal Brexit

BBG: Brexit Housing Crash Fears Stay in London as Regions Catch Up

FT: Finance sector hopes for smooth Brexit, plans for the worst

FT: Why DUP’s hardline Brexit stance is popular with voters

FT: Brexit fears set alarm bells ringing for financial services

FT: Theresa May survives but struggles to win over Tory Brexit rebels

FT: What next for Theresa May and her Brexit deal?

Stay tuned!

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Bloomberg Bond News Summary > Mon Mar 25th

Business Briefing

1) Trump Claims Vindication as Mueller Finds No Russia Collusion

Attorney General William Barr handed Donald Trump the biggest political victory of his presidency with an assessment that there was no collusion with Russia during the 2016 campaign and that there wasn’t enough evidence to find he obstructed justice. Trump celebrated Sunday’s news with relish, tweeting “Complete and Total EXONERATION” and telling reporters that Special Counsel Robert Mueller’s ...

2) Stock Sell-Off Roils Asia, Yields Slide Further: Markets Wrap

The stock sell-off that gripped markets Friday rolled into Asia Monday, with a gauge of the region’s shares heading for its biggest decline of 2019 and U.S. futures suggesting further losses on Wall Street. Bond yields plumbed fresh lows. Shares fell more than 2 percent in Tokyo, the biggest slide since December. Equities were down more than 1 percent in Hong Kong, Shanghai and Seoul, while European futures were lower. Australia’s 10-year bond yield recorded ...

3) May Faces Endgame as U.K. Leader Is Losing Control of Brexit

Theresa May will face up to her own desperately weak political position on Monday as the U.K.’s elected lawmakers move to take over Brexit policy and her own ministers plot to oust her. The prime minister is under pressure from colleagues inside her Cabinet to name a date when she will step down, with some arguing this would help her win support for her Brexit deal, people familiar with the matter said. May is hoping for one ...

4) One by One, Global Bond Markets Are Flashing the Same Warning

Just months after rising bond yields spooked markets, they’re now tumbling to the lowest levels in years to underscore concerns about slowing global growth. Yields in Australia and New Zealand dropped to record lows, after a closely-watched part of the U.S. curve inverted on Friday as investors wager that a recession is coming. Trading volumes in Treasury future were more than double the norm in the Asian morning, while Japan’s 10-year ...

5) Investors See More Pain Ahead as Global Stock Rout Gathers Pace

As the sell-off that struck the U.S. and Europe on Friday ripped through Asian stock markets, investors said that more pain is yet to come. Indexes in Australia, Hong Kong and China tumbled on Monday, with Japan’s Topix index and a gauge of regional equities heading for their steepest declines this year. The moves came after U.S. shares notched their worst day in 11 weeks on Friday as a gauge of Treasuries inverted for the first time ...

World News Briefing

6) Thai Military Party Leads Vote, Prayuth Set to Keep Power

A political party created by Thailand’s ruling military government was leading in the first election since a 2014 coup, putting junta chief Prayuth Chan-Ocha in position to return as prime minister. Palang Pracharath won 7.7 million votes with 94 percent counted, according to unofficial results posted on the Election Commission’s Facebook page. Pheu Thai, a political party linked to former premier Thaksin Shinawatra, came ...

7) Patriots’ Gronkowski Says He’s Retiring From NFL Football

Rob Gronkowski, the New England Patriots tight end and three-time Super Bowl champion, is retiring from football immediately, he told his 3.1 million Instagram followers on Sunday. The 29-year-old Gronkowski, nicknamed "Gronk", has been with the Patriots since they drafted him from the University of Arizona in 2010. He played in the NFL’s Pro Bowl five times. "I will be retiring from the game of football today," Gronkowski said on Instagram. "It was truly ...

8) Uber Is Said to Seal $3.1 Billion Deal to Buy Careem This Week

Uber Technologies Inc. is set to announce a $3.1 billion cash-and-share deal to acquire its Dubai-based rival Careem Networks FZ as early as this week, according to people with knowledge of the matter. The U.S. ride-hailing giant will pay $1.4 billion in cash and $1.7 billion in convertible notes for Careem, the people said, asking not to identified because the talks are private. The notes will be convertible into Uber shares at a ...

Bonds

9) CoCo Call Expectations Come With Safety Warnings After Santander

Barclays Plc and Banco Bilbao Vizcaya Argentaria SA may be planning to redeem some of their riskiest notes, even as the memory of Banco Santander SA’s skipped call leaves a question market in investors’ minds. The two lenders both issued new additional Tier 1 notes, or CoCos, last week that could replace older bonds approaching first call dates -- particularly as both banks had sufficient regulatory capital at the end of last year. Still, ...

10) Traders Gorge on Treasury Futures as Bonds Rally on Growth Fears

U.S. Treasuries are shaping up to be this year’s hottest long trade, reversing their status as the big short for most of 2018. Open interest, a measure of outstanding positions across Treasury bond futures, jumped Friday while 10-year yields slid as investors piled into haven assets amid mounting concerns about the global growth outlook. Positions in total bond futures climbed $19 million per basis point, equivalent to $21.5 billion of 10-year cash bonds. ...

11) Stressed Chinese Oil Firm Sweetens Bond Offer Ahead of Maturity

Chinese oil exploration company MIE Holdings Corp. extended the deadline of its bond exchange offer and added incentives for investors to participate as it struggles to repay a dollar bond next month. The Beijing-based firm pushed back the expiration date on the exchange offer for its $315.9 million senior notes by one week to March 29, according to a company filing. It also agreed to purchase as much as $30 million of the new notes after it ...

12) Yen, Dollar Advance as Global Bond Yields Tumble: Inside G-10

The yen and dollar climbed while bonds rallied as investors sought haven assets on rising concerns over global economic growth. * The Japanese currency rose against all its Group-of-10 peers while the 10-year yields of Australia and New Zealand dropped to record lows * “It is timely that markets have a reality check, and the bond market is leading the way in terms of growth risks,” said Philip Wee, a foreign-exchange strategist at DBS Group ...

13) Santander No-Call Surprise Places Investors on CoCo Bond Watch

The market for bank capital debt was shaken last month when Banco Santander SA defied precedent and declined the option to call a bond. Keep an eye on the next securities due to be called. Santander skipped an option to call 1.5 billion euros ($1.7 billion) of perpetual contingent-convertible notes, or CoCos. The rationale was that current market-funding costs meant it could be cheaper to extend the existing notes than redeem them and sell new ones. ...

14) Russia Battens Down Hatches With $7.2 Billion Borrowing Spree

The technocrats who run Vladimir Putin’s Finance Ministry know well that the next geopolitical crisis could be just around the corner. This year they’re preparing early for potential turbulence, stockpiling cash while times are good. The ministry borrowed more than $7.2 billion so far in March through local-currency and Eurobond sales, almost four times the monthly average in 2018, capitalizing on a recovery in demand among foreign investors. Finance ...

Central Banks

15) Volatility Is Back, With Turkey Leading Flash Flood of EM Risks

Emerging-market assets are headed for more tumult amid fresh signs that the global economy is weakening. Expected swings in emerging-market currencies on Friday jumped the most since Aug. 10, when Turkey’s lira posted its worst day of losses since 2001 and sparked fears it would drag other developing-nation assets down with it. The currency’s one- week implied volatility surged by the most since October 2004 despite a surprise tightening ...

16) S. Africa’s Mboweni Questions Need to Hold Onto State Assets

South African Finance Minister Tito Mboweni said a discussion must begin on whether the government needs to retain control of all the assets it owns given the poor state of the national finances. Mboweni has asked Minister of Public Enterprises Pravin Gordhan for a list of non-core state assets and has been provided with an “extensive list,” he said while being interviewed and answering questions from callers on Power FM radio. ...

17) Bruised Euro Area Seen Getting Biggest Fiscal Boost in a Decade

The euro-area economy, looks poised to get some lift from what once helped to push it into crisis: government spending. The bloc, at risk of splintering half a decade ago due to over-indebtedness, is now battling the headwinds including trade protectionism at a time when the European Central Bank has little room to lend a hand. With more and more reason to worry about the economy, a prop from additional public spending provides some ...

18) Evans Says Fed May Have to Ease If Downside Risks Become Reality

The Federal Reserve may have to put interest-rate increases on hold or even ease monetary policy if economic forecasts for 2019 disappoint, Chicago Fed President Charles Evans said. “At the moment, the risks from the downside scenarios loom larger than those from the upside ones,” Evans said in remarks prepared for a speech Monday in Hong Kong. “If activity softens more than expected or if inflation and inflation expectations run too low, then policy ...

19) Evans Says Risks From the Downside Loom Larger than Upside Ones

“Recent data on U.S. economic activity generally have been softer than anticipated,” says Federal Reserve Bank of Chicago President Charles Evans. * “At the moment, the risks from the downside scenarios loom larger than those from the upside ones,” he says. * Evans remarks in text of speech prepared for delivery in Hong Kong on Monday. * “If growth runs close to its potential and inflation builds momentum, then some further rate increases may be ...

20) China Has a Lot of Financial Opening Up to Do, Says Central Bank

The openness of China’s financial markets to the rest of the world isn’t high, so there’s a lot of room for increased access, according to People’s Bank of China Governor Yi Gang. Yi said foreign financial services institutions should be treated the same as domestic ones in terms of shareholding proportions, scope of business and licenses. Speaking at a forum in Beijing on Sunday, he said the central bank will focus on providing more hedging tools in ...

Economic News

21) Brexit Housing Crash Fears Stay in London as Regions Catch Up

The Brexit-inspired decline in London’s property values has yet to cause any serious ripples in other areas of the U.K. While price-growth and activity may be slowing amid the uncertainty, almost every other major urban area in the country is still experiencing a rising market, according to Acadata. It’s a national divide that’s all too apparent to real estate agents in northern England who aren’t too worried about the U.K.’s departure ...

22) THAILAND INSIGHT: Election Done, But Uncertainty to Persist

Thailand’s long-awaited election took place on Sunday, but political uncertainty could persist well after the official announcement of the victor, expected later Monday. * Victory for the military, with a low voter turnout and delayed posting of results, could spark protests. * A weak coalition government may lead to a policy logjam. * Prolonged uncertainty would likely continue to damp investment, which has been lackluster since a ...

23) Look to East EU for Movement as Monetary-Policy World Hits Pause

As major central banks scale back plans to raise interest rates amid signs of a weaker economic expansion, some parts of eastern Europe are set to push for measures to cool price growth. Hungary will kick off the deliberations Tuesday by starting to unwind its monetary stimulus. Two days later, the Czech Republic will debate whether to resume raising interest rates. While Poland and Romania are both likely to hold rates the following week, talk of rate hikes is ...

24) GLOBAL INSIGHT: How Much of World Economy Is Run by Populists?

As the share of G-20 GDP controlled by populists and non-democratic regimes rises, there are increasing signs that bad policies are hurting growth. A risk going forward: if global growth falls more sharply than we anticipate, antagonistic and inward-looking leaders of major economies will be ill-placed to coordinate a response. Who’s in Charge? G-20 GDP by Governance * Based on our classification, ...

25) ASIA WEEK AHEAD: Japan Output; China Profits; RBNZ to Hold

Japan’s output and jobs data will be a focus in a relatively quiet week ahead in Asia. Factory production may have contracted for a fourth straight month in February as weak external demand weighs on exports. We’ll also be watching for signs of slackening in the tight labor market. * In China, industrial profits likely continued to shrink -- with sluggish producer prices and a slowdown in industrial production both exerting downward pressure. ...

European Central Bank

26) ECB’s Rehn Says Brexit Poses Biggest Short-Term Risk: Welt

The possible Brexit fallout poses the biggest short-term danger for the economy and financial markets appear to “underestimate the risk,” European Central Bank Governing Council member Olli Rehn said in an interview with Die Welt published on Monday. The central bank must ensure there is “no bigger turbulence” even if the U.K. does leave the European Union without a deal, Rehn told the German newspaper, adding he hopes the no-deal Brexit scenario ...

27) Daily FX: ASEAN FX at Risk to US Recession Fears & Sentiment on Brexit, ECB

Your Forecast Is Headed to Your Inbox But don't just read our analysis - put it to the rest. Your forecast comes with a free demo account from our provider, IG, so you can try out trading with zero risk. Trade all the major global economic data live and interactive at the DailyFX Webinars. We’d love to have you along. Most ASEAN currencies appreciated against the US dollar this past week, owing to a surprisingly more-dovish-than-expected Fed rate decision. In addition, sentiment generally recovered ...

28) Aastocks.com: ECB: Mkt Underestimates No-Deal Brexit Risks

Finnish Central Bank Chief Olli Rehn, as well as a member at the European Central Bank’s rate-setting Governing Council, told Germany’s Die Welt that Brexit without deal is posing the biggest threat to the Eurozone economy in the short term, and the market seems to have been too relaxed and underestimated such risks. Related NewsEU Reportedly to Approve Brexit Delay this Week AAStocks Financial News Web Site: www.aastocks.com

29) Interest.co.nz: Global gloom following signs of falling EU and US growth drives NZ swap rate to record low

Ominous signs of a global economic slowdown and international events late last week have seen New Zealand’s two year swap rate hit an all-time low of 1.78%. An interest rate swap is where two people, or parties, agree to exchange two different types of interest rate for a specified period of time. NZ interest rate swap rates are determined by the rates on NZ government bonds and the demand for paying or receiving the fixed rate. A gauge of the level of demand is the difference between the NZ ...

30) National Herald: Schaeuble Says Greece Needed 10-Year Eurozone Break

Former German finance minister Wolfgang Schaeuble, the driving force behind brutal austerity measures imposed on Greece by international creditors – including his country’s banks – said the country should have taken a 10-year timeout from the Eurozone. Three bailouts of 326 billion euros ($369.05 billion) from the Troika of the European Union-International Monetary Fund-European Central Bank (EU-IMF-ECB) and the European Stability Mechanism ended on Aug. 20, 2018 but Greece still hasn’t been ...

Federal Reserve

31) Swift Pushback on Stephen Moore, Trump’s Latest Pick for the Fed

Stephen Moore drew swift and unusually pointed criticism after President Donald Trump picked him to be a governor of the U.S. Federal Reserve, with at least one prominent Republican economist calling on the Senate to block the appointment. “He does not have the intellectual gravitas for this important job,” Greg Mankiw, a Harvard professor who was chairman of the White House Council of Economic Advisers under President George W. Bush, wrote in a blog post ...

32) Get used to lower growth, Chicago Fed president warns

Hong Kong | The President of the Federal Reserve Bank of Chicago has warned that markets must come to grips with the idea that economic growth below 2 per cent is likely to be the new normal. Speaking at the Credit Suisse Asian Investment Conference in Hong Kong on Monday, Chicago Fed president Charles Evans also said the Federal Reserve's decision to pause before hiking US interest rates again was prudent, given the current setting was ...

33) Chart on TV: The Fed's Preferred Yield Curve Inverts

This chart was shown on Bloomberg TV. Visit TV on your terminal to see this chart discussed during the broadcast.

34) SCMP: The Federal Reserve has halted policy normalisation. Now, other central banks should follow suit

The Fed’s decision to stop interest rate rises and the shrinking of its balance sheet this year should be a cue for central banks in Europe, Japan and particularly China to take steps to bolster economic activity

35) Business Day.za: WATCH: Why Donald Trump blames the Fed for stunting US growth

The US Federal Reserve kept interest rates unchanged last week and intimated that there will be no increases in 2019. What does this tell us about the state of the US economy, emerging markets, and currency and investment strategies? London Capital Group’s head of research, Jasper Lawler, joined Business Day TV to talk about the US economy and its chances of going into a recession.

First Word FX News Foreign Exchange

36) TWD Falls First Time in 4 Days on Growth Concerns: Inside Taiwan

The Taiwan dollar falls for the first time in four sessions amid concerns that global economic growth is slowing. Markets * TWD drops 0.1% to 30.83 per dollar as of 2:26pm in Taipei * Taiex slips 1.5% to 10,479.48 at the close, marking the biggest drop since Jan. 2; TSMC was the biggest drag on the gauge with a 2.8% loss * 10-year government bond yield falls 2bps to 0.7690% at the close, lowest since October 2016 Key News * Taiwan Lawmaker Tseng Proposes ...

37) Indonesia’s Widodo Leads Poll, Subianto Narrows Gap: Charta

Joko Widodo-Ma’ruf Amin still leads Prabowo Subianto-Sandiaga Uno pair, but with a narrowing gap, according a survey by Charta Politika. * Widodo, known as Jokowi, gets 53.6% votes in latest survey in March, rising slightly from 53.2% in Jan. * Subianto narrows electability gap with 35.4% votes in March, up from 34.1% in Jan. * Jokowi’s approval rating seen at 65.9% in March vs 65.8% in Jan. * Survey conducted on 2,000 respondents in 34 provinces on March 1-9, ...

38) Conte Says Local Vote Result No Threat to Government: Stampa

Last year’s national elections were a case of Italians turning the page on politics of the past and the results in various local votes since then -- with most favoring the League over the Five Star Movement -- don’t suggest a return to national elections is necessary, Prime Minister Giuseppe Conte says in an interview with La Stampa. * Recent local elections did not show a “brilliant performance” from Five Star * “For sure” there will not be corrective ...

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Astor Ridge Data/Supply/Events Calendars for Mar 25-29

Highlights…

Busy week for data across US/UK/EUR…

Supply calendar modest with US busy but UK and Europe lighter than usual.

LOTS of speakers from FOMC and ECB…

And the final countdown for Brexit votes – or not – will dominate…

Please see attached.

Best,

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

BOND YIELD UPDATE : THE YIELD DROP ISNT OVER, ITS ONLY JUST BEGUN! Soon people will REALISE they NEED yield, it will be a “MAD RUSH” into month-quarter end.

BOND YIELD UPDATE : THE YIELD DROP ISNT OVER, ITS ONLY JUST BEGUN! Soon people will REALISE they NEED yield, it will be a “MAD RUSH” into month-quarter end. Post the FED we have finally ENDORSED the MANY historical moving average rejections, that setting us on a path for lower yields. Many ranges are also too small and will probably end up replicating that of 4th quarter 2018, ITS GONNA GET MESSY.

REMEMBER CTAs KEEP buying for their trend-momentum returns irrespective of yield levels.

Real money has already been buying EM to lock in more attractive yields, am sure soon to ADD.

The long-term quarterly-monthly charts continue to forecast MUCH lower yields and little obstacles in their path!

On paper the quarterly and monthly charts are obvious, its MUCH lower yields. We are failing MANY RARE 50 and 100 period moving averages aided by RSI dislocations that date back to 1980’s. The formations are staggering given the previous upsets in and around 2000 - 2007.

It seems from a chart perspective everyone is convinced rates are going MUCH HIGHER based on the HISTORICAL RSI dislocations. Expectation and positioning is way too optimistic.

The weekly charts are more optimistic for a HOLD but daily negate that almost instantly.

Daily charts have persisted in remaining sub numerous 200 day moving averages, so ideally its all a matter of time.

Germany and UK also point to lower yields, whilst Italy is pausing at a recent low.

ASTOR RIDGE : Independent Ideas, Research, Liquidity, Anonymity and Trusted Experience.

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Today's BREXIT BARRAGE... "Once more, with feeling...'

BBG: EU Gives Theresa May Two Weeks to Avoid a No-Deal Brexit

BBG: Brexit Cliff Edge Is Already Real for Some People

BBG: Stop Brexit Petition Passes Two Million Names as Delay Looms

BBG: Brexit Bulletin: One Last Chance

FT: EU imposes new Brexit timetable allowing May last chance for deal

FT: Pound firms after EU leaders allow May more time on Brexit

FT: UK gilts rally most in four months on Brexit angst, dovish Fed

FT: How the EU leaders reached a decision on Brexit

FT: Could Brexit break the Union?

FT: Brexit: polls that show how Britain cannot make up its mind

FT: Chastened May seeks to make amends for ‘cataclysmic’ 24 hours

BBC: Theresa May to urge MPs to back deal as delay agreed

BBC: Brexit: What could happen next?

BBC: Brexit: Three moments that raised a smile

TEL: EU leaders offer UK delay to May 22 – if MPs back Theresa May’s deal

TEL: ‘Silent assassin’ about to strike: Why Michael Gove is tipped to replace Theresa May

TEL: Can Article 50 be revoked and what would it mean to cancel Brexit?

TEL: No deal Brexit: the five big warnings vs the reality

TEL: Brexit: What will MPs vote on in Parliament next week?

The Telegraph has a TON of material on Brexit this am – this just scratches the surface…

Best,

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796