MACROCOSM: Preview of a Busy Week & Highlight on BTPS/SPGBs Long-End w/charts

Interesting week lined up...

Highlights:

> Today's month-end index extensions are significant in Europe (+.12yrs) while the US (+.04yrs) and UK's (+.01yrs) moves are below avg.

> Europe's +.012yr aggregate move (BAML's #s) is one of the year's highest, highlighted by +.24yrs in FRA, +.11yrs in GER, +.08yrs in ITA, BEL, and FIN and +.07yrs in SPA. IRE's +.27yrs must be a record although market impact will be subdued given IRE's small share of the EG00 index.

> Flows/liquidity this week could be more sporadic than usual as it's Golden Week in Japan, tomorrow is May Day across Europe, Wed is Independence Day in Spain and there's a long-weekend in the UK coming up. This could impair the market's ability to take down some OBLs Wed and a pretty chunky amount of SPGB and FRTR duration Thurs. (see below)

> Add to this the FOMC meeting Wed and US's NFP release on Friday, coming after a handful of other info (Pers income, PCE & Chic PMI today, ISM tomorrow). With CFTC data reporting RECORD shorts in TY/UXY futures and 3% 10yr yields still a sneeze away, technicals could have a lopsided impact on s/term biases.

BTPS and SPGBs...

> Our bearish BTPS 48-67s flattener position is opening at 18.3bps, about where it closed Friday. On the one hand, the bearish tone of EGBs on the open is helpful (see 5 Star's Di Maio's comments over the weekend) but the surprise announcement Friday of Spain's tap of their SPGB 66s this Thursday didn't do our BTPS 67s any favours and I suspect that until that supply is out of the way, there will be pressure on 50yr EGBs across the board.

> The SPGB 46-66s sprd has steepened about 2.75bps since the tap announcement, the biggest steepening of this spread since the last tap was announced in Nov last year. We can see from the last two taps that the avg pre-tap concession has been about 4bps which, given how little time we have to set up for the tap, seems about right this week too. A spike 4bps steeper was a buying opportunity the last couple times and given the tone of the market last week, a move like that is likely to provide a similar opportunity this week. (see chart below)

> Last Thursday we called for a corrective bounce in EGBs post-ECB and into today's index moves which has worked nicely as the 157.75 fibo support in RXM8 provided a floor for a bounce to within a couple ticks of first key resistance (20 Day MA at 158.87 area). (see attached) We're opening with a modest bearish bias which reiterates the importance of this resistance (followed by 159.00 breakdown level). First support is 158.18 (5 day MA). We expect that once this index event is done the tailwinds EGBs enjoyed in April will have passed, opening the door for a more symmetrical trading bias but for the time being the market’s likely to be trading from a buy the dip mentality today.

RXM8

SPGB 46-66 vs BTPS 48-67

More to come…

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

The Week Ahead Euro Govts - James Rice, Astor Ridge - a quick look, more today!

Good morning, apologies for sending this again. Just some quick thoughts as we come into May and the long Weekend ahead

I’ll update with some of the Model P/F trades and what we’re thinking

Week: Monday, 30th April – Friday 4th April

Supply

Wednesday 2nd May

- German 5y, €3Bln

Thursday 3rd May

- France 8y, 10y, ‘15y’, 30y (26s, 28s, 34s, 48s) €7,5 – 8,5 Bln

- Spain – 3y, 10y & 50y

- UK 5y 2023 £3 Bln

Risk Relationships / Events

- It/Ge spread on the narrows

- See Peripherals as historically rich (yields low)

- See U.S. as historically cheap (yields high)

- Better receiver bullets vs wings in major butterfly structures; 5s10s30s & 2s5s10s

- See semi core (France) as rich vs Blend of Core and Germany, just starting to cheapen

- Nonfarm payrolls – May 4th

Ideas

FRANCE 15YR TO CHEAPEN FURTHER as a tactical trade into supply

- 15yr sector generally trades rich in all the main Euro issuers

– on a swap and vol. adjusted basis the BGB 31s, Italy 32s appear richest with the new French 34s following shortly after

- The Frtr 5/28 issuance next Thursday is a cheap tap point (28.6bln issues size) and this tap would make it consistent with old and double old French 10yrs issue sizes (31.5bln & 30.2Bln respectively). Hence this could be the last tap of the 5/28 and the time for it roll to the rich 8y, index duration sector

- The low coupons of the French 12y to 15y sector bely an absence of cash flow value relative to their wider neighbours

- Sell French 15y to buy French 10y vs +RX/-UB

100 * ((YIELD[FRTR 1.25 5/34 Corp] - YIELD[FRTR 0.75 5/28 Corp]) - 0.6 * (YIELD[DBR 3.25 7/42 Corp] - YIELD[DBR 0.25 2/27 Corp]))

This relationship could move higher as the French 34s soften to absorb supply -as we go into next week’s auction

Spain 1/21 vs 4/22 too flat vs Germany

- The tap point 1/21 looks super cheap on z-spread relative to local bonds and also the same points in Germany, indeed it’s approx. as flat as the German Curve in Z-Spread terms, which would be a boundary condition for a credit issue relative to Germany

- Coupled with a bearish view on peripherals this is a really soft play on spread wideners – Spain vs Germany

- As always for liquidity, I prefer expressing the trade vs a reduced wider spread of two German contracts (ctds used)!

100 * ((YIELD[SPGB 0.4 4/22 Corp] - YIELD[SPGB 0.05 1/21 Corp]) - 0.5 * (YIELD[DBR 1.5 2/23 Corp] - YIELD[BKO 0 3/20 Corp]))

Looking for this relationship to head BACK TO 0

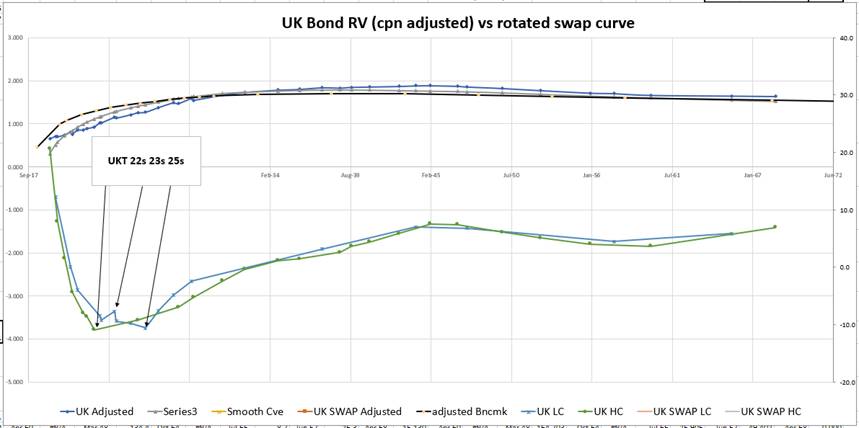

RADAR TRADE – supply trade in UKT 23s – not yet at target

- One of the challenges with supply in Govt F.I. markets at the moment is to try and ‘call’ the cheap levels at which RV might take down a re-tapped issue

- One such issue is UKT 23s, to be tapped next Thursday – this issue first came in Jul 2017 and has been tapped 8 times since and will indeed be tapped again on 6th June

- The swap curve and bond curves are slightly different shapes – by applying a shift and a magnification to the swap curve vs the we can get another perspective on Gilt RV… one that is more empathetic to the gradient and initial point differences between swaps and bonds – (UK bond curve ≈ 1.65* uk swap – 1.03%)

- So the structure that is on my radar is

200 * (YIELD[UKT 0.75 23 Corp] - 0.5 * YIELD[UKT 4 3/22 Corp] - 0.5 * YIELD[UKT 2 25 Corp])

Looking for > +15bp – let’s see what next week brings

Best

James

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

MICROCOSM: UKT 37-47-68 Fly At Attractive Levels (Amended)

(Small amendment to the fly-weighting below)

- May and June will be big months for UK gilts supply. Here’s the calendar:

- May 3rd UKT 0T 7/23

- May 9th UKT 2.0 2/28

- May 18th (street consensus) 2073 Ultras syndication

- May 24th UKTi .128 36

- Jun 6th UKT 0T 7/23

- Jun 20th New UKTi 10yr

- Jun 26th UKT 1T 9/37

- May 3rd UKT 0T 7/23

- The conspicuous absence in the list of auctions above is the 30yr benchmark. This means a few things to us:

- The absence of 30yr supply means the sector should out-perform the 20yr and 50yr, in the 1-2 weeks before their auctions.

- With the UKT 1H 7/47s already £24bn+, there is a strong likelihood in our view that we will get a new 30yr benchmark in the next couple quarters via auction.

- If a new benchmark is indeed on tap, the UKT 1H 7/47s should richen to the curve, removing some of the cheapness that we’ve seen in the issue since it’s launch, much like the recent normalization of the UKT 1Q 7/27s.

- The absence of 30yr supply means the sector should out-perform the 20yr and 50yr, in the 1-2 weeks before their auctions.

- As an offshoot of the above, we like owning the UKT 1H 7/47s, either has a flattener vs the UKT 1T 37s or on butterfly versus the UKT 3H 7/68s. The timing looks good to us, here’s why:

- UKT 1T 37 vs UKT 1H 47s sprd is climbing to resistance levels that have held over the last year.

- A May hike from the MPC appears to be off the table as data has disappointed and Carney’s comments leaning dovish. That has pushed the first hike out to Nov and reduced the rate rises to just 44bps over the next 18 months. This has reduced the bear flattening by about 17bps (5-30s) since late March and we would suggest much of the short base in the front-end.

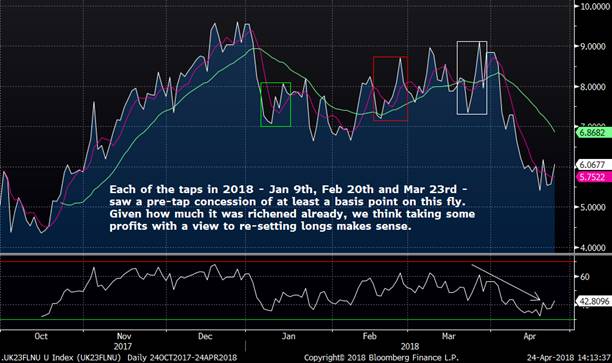

- The syndicated ultra issue will be a TON of risk, our back of the envelope calculation says somewhere around £20mm a bp. LDI players, who dominate these syndications, are very yield sensitive, particularly when we are trading a stone’s throw from historic lows. So, we were pleased to see UKT 68s cheapen from 1.50% to 1.75% during April, hoping that the move would ensure strong demand in mid-May. Well, 1.75% was breached briefly on Apr 23rd, triggering a flood of demand that has richened the 68s 10bps, taking them from cheap back to fair. (see chart) We think the market will be incentivised to build that concession back into ultras before the syndication is formally announced, either on the curve or in outright yield space.

- UKT 1T 37 vs UKT 1H 47s sprd is climbing to resistance levels that have held over the last year.

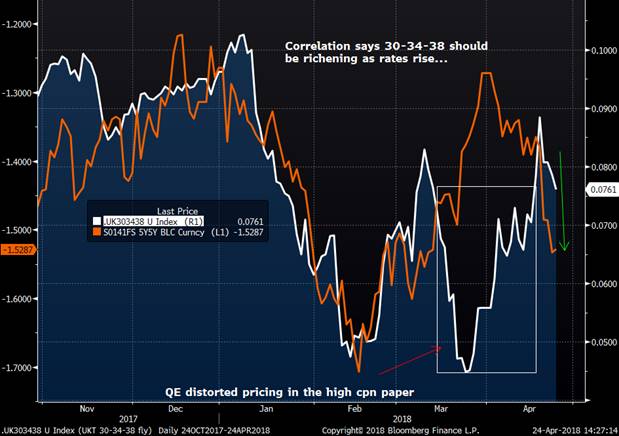

- This UKT 1T 37 – UKT 1H 47 – UKT 3H 68 fly is a bit lopsided, the short leg around +1.9bps and the longer leg around -20bps. Some might be inclined to look at the absolute levels of each of the wings and use a ratio that reflects the inherent risk in the fly. In this case, however, what makes more sense to us is to consider the trading range of the wings of the past year to determine how volatile they are and vs each other. Over the past year, the range in the UKT 37-47 spread has been 4.8bps, the UKT 47-68 sprd 10bps, which looks like the short leg is about half as volatile as the longer leg. So, we’ll shift half the risk in the long-leg to the short leg, giving us a 67-100-33 weighting. We can see that this changes the absolute level of the ‘fly’ and, interestingly enough, it improves the location of it while tightening up the trading range of the last year to about 3bps. Clearly, if you prefer the 1-2-1 approach and want to bet on a more dramatic shift in the ultras leg then, by all means, that remains an option.

In light of the timing of the syndication relative to the tap of the 37s, we may be inclined to unwind the 47-68s leg first and let the 37-47s leg ride.

L U8 has rebounded nicely

UKT 37-47s sprd

UKT 37-47-68 1-2-1 fly vs 1y1y Sonia.

UKT 37-47-68 fly with a 67%-100%-33% weighting… Changes profile – perhaps for the better.

I’ll call to discuss.

Thanks

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

The Week Ahead Euro Govts - James Rice, Astor Ridge - a quick look, more on Monday

Week: Monday, 30th April – Friday 4th April

Supply

Wednesday 2nd May

- German 5y, €3Bln

Thursday 3rd May

- France 8y, 10y, ‘15y’, 30y (26s, 28s, 34s, 48s) €7,5 – 8,5 Bln

- Spain – 3y, 10y & 50y

- UK 5y 2023 £3 Bln

Risk Relationships / Events

- It/Ge spread on the narrows

- See Peripherals as historically rich (yields low)

- See U.S. as historically cheap (yields high)

- Better receiver bullets vs wings in major butterfly structures; 5s10s30s & 2s5s10s

- See semi core (France) as rich vs Blend of Core and Germany, just starting to cheapen

- Nonfarm payrolls – May 4th

Ideas

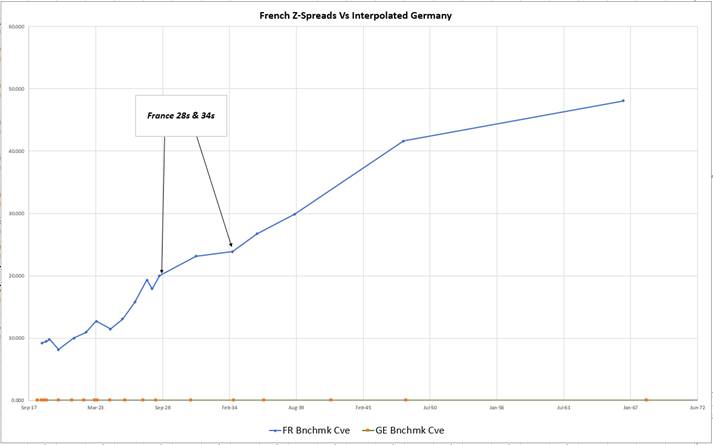

FRANCE 15YR TO CHEAPEN FURTHER as a tactical trade into supply

- 15yr sector generally trades rich in all the main Euro issuers

– on a swap and vol. adjusted basis the BGB 31s, Italy 32s appear richest with the new French 34s following shortly after

- The Frtr 5/28 issuance next Thursday is a cheap tap point (28.6bln issues size) and this tap would make it consistent with old and double old French 10yrs issue sizes (31.5bln & 30.2Bln respectively). Hence this could be the last tap of the 5/28 and the time for it roll to the rich 8y, index duration sector

- The low coupons of the French 12y to 15y sector bely an absence of cash flow value relative to their wider neighbours

- Sell French 15y to buy French 10y vs +RX/-UB

100 * ((YIELD[FRTR 1.25 5/34 Corp] - YIELD[FRTR 0.75 5/28 Corp]) - 0.6 * (YIELD[DBR 3.25 7/42 Corp] - YIELD[DBR 0.25 2/27 Corp]))

This relationship could move higher as the French 34s soften to absorb supply -as we go into next week’s auction

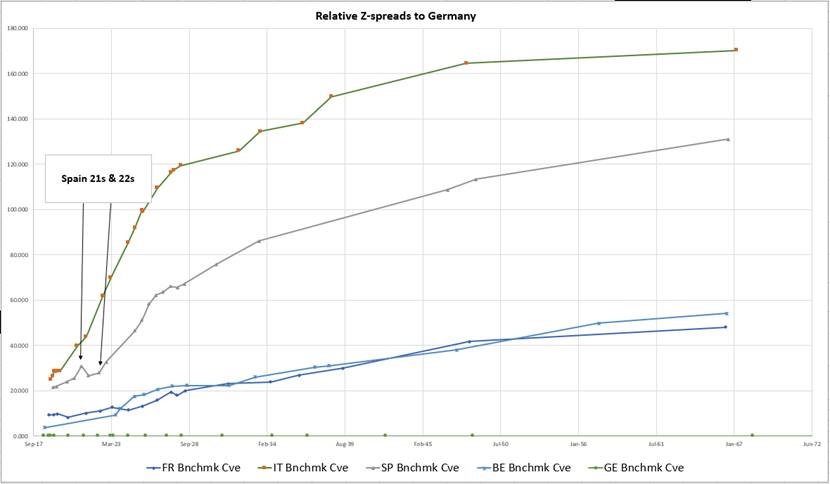

Spain 1/21 vs 4/22 too flat vs Germany

- The tap point 1/21 looks super cheap on z-spread relative to local bonds and also the same points in Germany, indeed it’s approx. as flat as the German Curve in Z-Spread terms, which would be a boundary condition for a credit issue relative to Germany

- Coupled with a bearish view on peripherals this is a really soft play on spread wideners – Spain vs Germany

- As always for liquidity, I prefer expressing the trade vs a reduced wider spread of two German contracts (ctds used)!

100 * ((YIELD[SPGB 0.4 4/22 Corp] - YIELD[SPGB 0.05 1/21 Corp]) - 0.5 * (YIELD[DBR 1.5 2/23 Corp] - YIELD[BKO 0 3/20 Corp]))

Looking for this relationship to head BACK TO 0

RADAR TRADE – supply trade in UKT 23s – not yet at target

- One of the challenges with supply in Govt F.I. markets at the moment is to try and ‘call’ the cheap levels at which RV might take down a re-tapped issue

- One such issue is UKT 23s, to be tapped next Thursday – this issue first came in Jul 2017 and has been tapped 8 times since and will indeed be tapped again on 6th June

- The swap curve and bond curves are slightly different shapes – by applying a shift and a magnification to the swap curve vs the we can get another perspective on Gilt RV… one that is more empathetic to the gradient and initial point differences between swaps and bonds – (UK bond curve ≈ 1.65* uk swap – 1.03%)

- So the structure that is on my radar is

200 * (YIELD[UKT 0.75 23 Corp] - 0.5 * YIELD[UKT 4 3/22 Corp] - 0.5 * YIELD[UKT 2 25 Corp])

Looking for > +15bp – let’s see what next week brings

Best

James

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

BONDS UPDATE ....BONDS PRICES now appear to be holding, in GERMANY especially!. 26.04.2018.

BONDS UPDATE : BONDS now appear to be holding, in GERMANY especially! A lot to play for as MONTH END approaches.

Many daily RSI’s in Germany and US are now VERY OVERSOLD so looking for a recovery into the remainder of the week.

MOST quarterly and monthly BOND YIELD charts are close to confirming a LONGTERM YIELD failure, in a similar fashion to some EQUITY markets.

- **German 10yr yields could soon confirm a MAJOR STALL see page 15 & 16.**

- Although we have revisited the YIELD highs in many cases the RSI should draw yields lower today.

- (US 5yr and UK 10yr). ALL durations are stretched, quarterly, monthly, weekly and daily… this is RARE!

- Germany 46’s HOLDING previous lows.

- UK yields have a LOFTY RSI and UKTI POISED to bounce. UK 10yr all eyes on a continued breach of 1.489 (10yr Gilts).

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

MICROCOSM: Tactical Bullish EGB Trades Into ECB & April Month-End

- We’ve been trading the European govt bond and UK gilts markets from the bearish side for about the last 10 sessions which has worked out well on balance. Our bearish bias was driven largely by the realization that fears of a trade-war were overblown (for now), April coupon and redemption flows in EGBs were largely priced in, price action deteriorated as positioning grew longer and a steady climb in oil prices awoke fears of a bounce in inflation. In addition, seasonals in EGB rates and spreads return to a more neutral/bearish outlook from May until July (especially in France). Add to that a grind towards the psychological 3.00% level and the bearish bias made sense.

- While some of the concerns noted above will likely hang over the rates markets for the next 3-4 weeks at least (positioning, oil and supply for starters), it looks to us like we could be in for a tactical bounce in EGBs between now and Monday. Here’s why:

- RXM8 charts show the 38.2% retracement level – 157.75 – has proven significant support this week, the market ‘building value’ around this level. This has coincided with oversold RSIs bottoming out. This morning’s rally to 158.00 confirms this support.

- OIL’s over bought technicals have stalled, consolidating just below the highs, momentum slowing.

- As this morning’s WSJ opines (click here) , Draghi is likely to not only keep any mention of winding up QE on hold until July but could strike a more dovish tone than we’ve seen of late. Trade tensions (real or imagined), trade weighted Euro remains at multi-year highs, stubbornly low inflation and some unseasonal weather are all fair game.

- Monday’s index extension in Europe is estimated +.11/.12 yrs (depending whose system you use), driven by +.23yrs in Ireland, +.20yrs in Spain, +.16yrs in France and Portugal. This is one of the biggest extensions of the year which favours OATs most given the combination of their share of the index (usually around 24%) and the size of the move.

- Next week is Golden Week in Japan which generally means activity out of Japan dies down sharply. Yesterday dealers reported some dip buying from Japan in USTs, DBRs and OATs which appears to have resumed this morning. With Oats hedged back into JPY at levels last seen in early March, this dip buying could be significant.

- To provide protection (hedges) for some of our bearishly biased positions (like BTPS 48-67s flatteners, DBR and FRTR steepeners in the belly, etc), we suggest a tactical outright long in OATM8 and/or RXM8 or invoice spreads, bull flattening positions like FRTR 3/23 into FRTR 5/27s or BTPS 3/23 into BTPS 8/27s. These may turn out to be 2-3 day positions into month-end but it could be worthwhile insurance if the market becomes more volatile.

RXM8 bouncing off support

OATs seasonals have been working nicely so far this year. Could see one last bounce, however, before selling emerges.

OIL’s steep climb has run out of steam…

RXAISP…

I’ll be in touch…

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

FX UPDATE : USD STRENGTH has started to occur on many crosses but the KEY one remains the EUR USD.

- USD STRENGTH has started to occur on many crosses but the KEY one remains the EUR USD. 1.2168 has been HIT.

- **Chart 2 gives a very MAJOR clue as to how BAD the EURO DEMISE might be.**

- The EUR USD, is still yet to breach the all-important 1.2167.

- USD EM has seen many BLOW OUT scenarios but a TOP might be in for USD RUB and USD TRY.

- USD CAD has been a major call and bounced well, it now looks poised for its next bout of CAD weakness.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

US CURVES : DARE I say we are finally BASING?! It has taken time to BASE and 100% confirmation is looming as month-end approaches.

US CURVES : DARE I say we are finally BASING?!

It has taken time to BASE and 100% confirmation is looming as month-end approaches. Also this is happening with a HIGHER yield bias, which I still have reservations about.

US 2-10 page 4 has held trendline support.

If we do gain confirmation then remember we have significant RSI dislocations, on ALL monthly durations. Last week we established several downside pierces on the daily charts aided by REAL MONEY activity.

** Trade idea : Between myself and David Sansom we have several trade options that are happy to send and discuss. **

I still think this will be a BULL STEEPENER, correlation isn’t great having made this statement BUT preciously it took time to change the yield direction.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

EQUITY UPDATE We are failing at the MAJOR Bollinger averages SO the BIAS remains for LOWER PRICES. Europe has alot of work to do 25.04.2018

NEVER been a BIGGER SET of EQUITY CLOSES for MONTHEND .

We are getting close to a MAJOR LONGTERM “TOP” formations should we CLOSE the month at the LOWS! Europe has a lot more work to do this time as the rolls have reversed.

**Currently there has been a shift from Europe leading the way to the US being the focus. **

Post Mark Zuckerberg HOUSE grilling I was personally was not impressed.

It seemed to blame the public for using the platform and freely offering their details. If banks sold peoples personal information, they’d face millions in fines. Am sure regulation will catch up with this sector as long as that is BALANCED with FREE surveillance for government bodies.

The NASDAQ IS NOW close to EMULATING the 2000 DROP (see page 16).

As mentioned I still fancy an old fashioned stocks DOWN bonds UP and bonds are HOLDING.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

MICROCOSM: Gilts Market - Observations and Ideas w/Charts

GILTS... Some thoughts and observations:

- 53.6% odds of a 25bps hike in May and just 50bps priced in over the next 18 months. Given the tone of Carney’s comments, the tone of the recent data and the state of the Brexit talks, that’s probably about right.

- Theresa May has had a rough week with the House of Lords trying to foist a softer Brexit on her. If this gathers momentum, is it not GOOD for the UK economy if the customs union with the EU remains in all but name? GBP certainly doesn't trade like it feels that way. Here’s an interesting comment in The Independent ‘Brexit minister reveals how MPs can force Theresa May to accept fresh referendum.’ Can the UK reverse Article 50? Have a look.

- The short end has re-steepened (1H 21 v 0H 22 +5bps from May lows) but 22s still not looking cheap enough yet to get back into a flattener. Chart suggests +20 has been key resistance of late which is still ~3bps away.

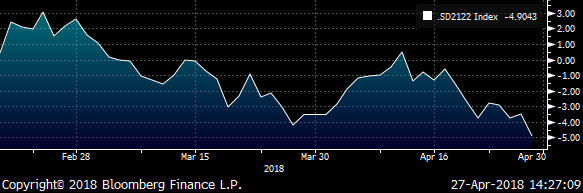

- UKT 0T 7/23s will be tapped May 3rd. Our 7/22-7/23-9/24 fly has stalled in the 5.5-6.0 range for the last 10 days, despite some big gyrations in short sterling/Sonia. As this is the penultimate tap of the issue before an expected new 5yr benchmark in July, there's a coterie of clients who are loathe to part with their UKT 7/23s as they’ll soon stop being tapped. We don’t blame them as they could richen further into July all else equal. For those who want to actively manage their position, however, I think it’s worth taking profits in this zone before the end of this week and look to jump back in after a concession has been priced in. See chart below pls.

- Micro trades still in vogue in gilts while we await the announcement of the new ultra syndication – likely in mid-late May. For example:

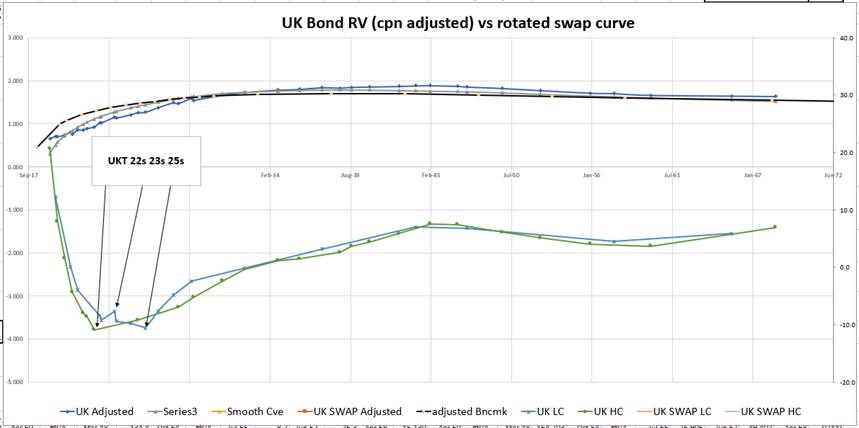

UKT 30-34-38 fly looks too cheap here given the correlation to rates.

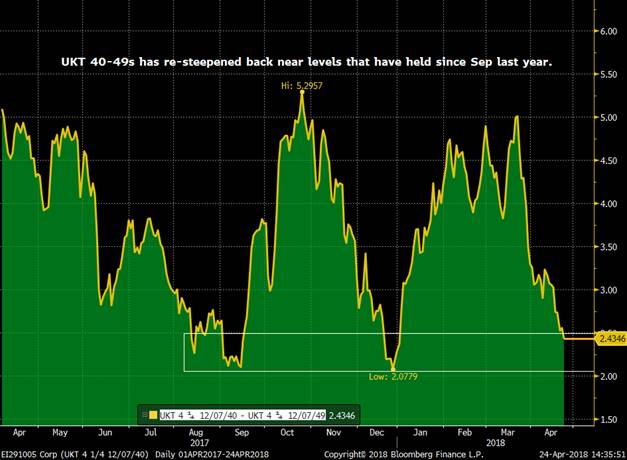

UKT 4Q 40 into UKT 4Q 49 back to key levels that have been good places to get back into flatteners since Sep last year. No 30yr supply due until next qtr at the earliest.

- The ‘elephant in the room’ in May will be the syndicated ultra issue. We don’t know the exact details yet but we do know it’ll have a 2072/73 area maturity and could be in the £4-5bln range. That’s a TON of risk. One development we can draw some comfort from – unless it reverses course soon – is the ~25bps cheapening in ultras yields. That may not sound like much but when you realize that 25bps is almost 17% of the yield on Apr 1st (in absolute terms) and that demand at 1.50% is likely to be a lot different than it’d be at 1.75%, it comes into perspective. When we add in stories like the one about RBS’s likely pension investment needs in May/Jun it makes one think that yes, it’s a ton of risk but somehow the market will find a home for it. That has implications not just for ultras but for the shape of the curve in the long-end which has spent much of the last few weeks dis-inverting. We still like our Long UKT 55s vs 49s and 60s which has richened from -4.2bps to -5.4bps.

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796