BONDS UPDATE Many daily RSI's are LOW so BONDS should rally for the remainder of the week. 24.04.2018.

BONDS UPDATE : BUY BONDS today with a stop below YESTERDAYS lows, BONDS should rally for the remainder of the week.

**Many daily RSI’s in Germany and US are now VERY OVERSOLD so looking for a recovery into the remainder of the week.**

MOST quarterly and monthly BOND YIELD charts are close to confirming a LONGTERM YIELD failure, in a similar fashion to some EQUITY markets.

- Yields are close to breaching levels where we will see a MAJOR DROP.

- Although we have revisited the YIELD highs in many cases the RSI should draw yields lower today.

- (US 5yr and UK 10yr). ALL durations are stretched, quarterly, monthly, weekly and daily… this is RARE!

- Germany 46’s HOLDING previous lows.

4) UK yields have a LOFTY RSI and UKTI POISED to bounce. UK 10yr all eyes on a continued breach of 1.489 (10yr Gilts).

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

FX UPDATE...A BIG day for the USD on many fronts as we approach some KEY BREAK levels. 23.04.2018

- A big day for the USD on many fronts as we approach some KEY BREAK levels.

- The EUR USD, is still yet to breach the all-important 1.2167.

- USD EM has seen many BLOW OUT scenarios but a TOP might be in for USD RUB and USD TRY.

- USD CAD has been a major call and bounced well, it now looks poised for its next bout of CAD weakness.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

US CURVES It looks like we have FINALLY HELD? It has taken time to BASE and to be 100%, ideally wait confirmation at month-end.

US CURVES It looks like we have FINALLY HELD?

It has taken time to BASE and to be 100%, ideally wait confirmation at month-end. Also this is happening with a HIGHER yield bias, which I still have reservations about.

US 2-10 page 4 has held trendline support.

If we do gain confirmation then remember we have significant RSI dislocations, on ALL monthly durations. Last week we established several downside pierces on the daily charts aided by REAL MONEY activity.

** Trade idea : Between myself and David Sansom we have several trade options that are happy to send and discuss. **

I still think this will be a BULL STEEPENER, correlation isn’t great having made this statement BUT preciously it took time to change the yield direction.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

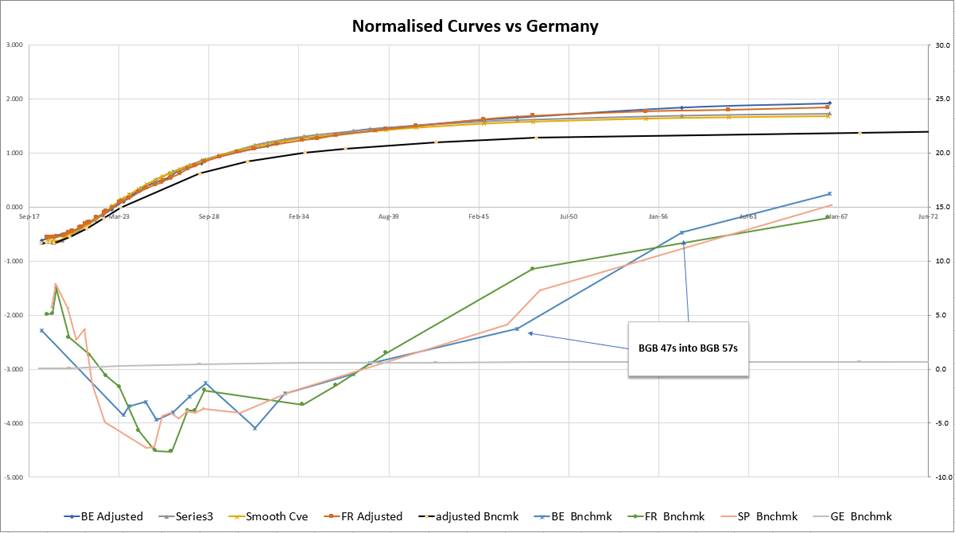

The week ahead - James Rice @Astor Ridge

Monday 23rd April

Monday – Belgian Supply; 24s, 28s, 47s, 57s

Improving credits across the board leave Belgium 47s -57s one of the steepest curves vs Swaps, vol. adjusted

Looking for >+20bp

By applying a linear transformation to all Euro curves we can compare them ‘vol adjusted’ to the German and Swap curves

Structurally, the curves should flatten vs the least risky issuers as credit concerns wane – as represented broadly by the narrowing of France and Italy vs Germany

Normalised Actual and R/C curves vs Germany….

Italy 5y & 10y supply (exact details TBA tonight, Monday)

Tonight Italy will formally announce the Italian supply tonight – I expect the usual 5y and 10y for this Friday

I can’t see any compelling structures there at the moment

Additionally this week we have US supply 2y, 5y & 7y

Next week

5y Germany, Spain and Long Term France

More to follow on general Euro RV

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

How are we doing? Shadow OTC portfolio update

Portfolio since 21st March: USD +560k, Ytd +711k

Summary: A much better month for my shadow portfolio. The UK curve flattened sharply vs the US on MPC rate hike optimism, and thankfully for once I booked the profit: as the box has now sharply reversed following Carney’s unexpectedly dovish comments which stunted the prospects for a May hike. I have kept the 1y expiry CMS trade on GBP 2y-10y vs USD, though it has moved against me, however I have taken the opportunity to add the same trade but on a very short, one-month horizon and using floors (given the risk that the MPC does in fact do nothing in May). Still in the UK, the Gilt market flattened 10-30 into the quarter-/fiscal year-end and this opened up a discrepancy with the prevailing relationship to 2y1y (ie short rate expectations): as advised by my colleague, the 10-30 re-steepened so I booked a quick profit. Finally, the ECB minutes showed a distinct reluctance to confirm a rising path for inflation which led me to set a bear-steepener on 3y1y/5y5y with an expiry before the June ECB meeting. To my mind the down-playing of inflationary risks (eg from a trade war) was significant and likely to keep a cap on 3y1y in the short term, until the ECB likely makes a decision on PSPP2 at the June meeting.

My general portfolio can be characterized as long-term strategic curve plays (flatter in EUR, steeper in GBP) with more tactical event-based trades. In EUR, I see the dynamic as being long-term flattening as accommodation is removed, but in the short-term the market can continue to be disappointed with the pace of moves. In the US, spreads like 2y1y/3y1y has been flirting with negative territory, but has stabilized for now: I am hesitant to put new US steepening into the book until I see that spread sit around zero for some time.

Others will have pointed out the narrowing of the EUR-CHF spread in 5y5y. This has taken place in the context of a sell-off, with CHF 5y5y moving faster than EUR. In an ideal world, one would buy CHF mid-curve receivers on 5y5y and sell EUR. Unfortunately CHF mid-curves are rare beasts, so one alternative would be to create the synthetic mid-curve by buying 2 lots of 3m10y receivers and selling 1 lot of 3m5y (this ignores the correlation risk of 5y & 10y, but is an acceptable short-term proxy).

So the trade I will be looking at on Monday is:

Buy 2 x CHF 3m10y receivers

Sell 1 x CHF 3m5y receivers

Sell 1 x EUR 3m5y5y mid-curve receiver

DV01/FX weighted

Let me know if you’d like more details. CHF vol is not the most liquid market but an opportunity might present itself. Otherwise, have a great weekend!

EUR/CHF 5y5y

Portfolio Changes:

- Closed GBP/USD 2y-10y, 1y fwd for profit

- Opened EUR CMS 10-5 collar

- Opened & closed GBP 10-30 vs 2y1y for profit

- Opened EUR 3y1y/5y5y bear steepener

- Opened GBP/USD 2y-10y, 1m floors

Portfolio since 1st Jan

|

Trade Idea |

Entered |

Level |

Size |

Status |

Exit/Current Level |

Exit Date |

P&L k USD |

|

US 2-10 steepener via CMS caps |

28-Dec-17 |

0 bp |

USD 25 k/bp |

CLOSED |

0 bp |

15-Jan-18 |

0 |

|

RX/UB ASW Box |

28-Dec-17 |

-6.1 bp |

EUR 50 k/bp |

CLOSED |

-5.2 bp |

06-Mar-18 |

-56 |

|

EUR 1y3y/5y5y Mid-curve flattener |

28-Dec-17 |

13.7 bp |

EUR 20 k/bp |

CLOSED |

29 bp |

31-Jan-18 |

380 |

|

GBP 1y1y1y MC Payer spread |

28-Dec-17 |

0.7 bp |

GBP 25 k/bp |

CLOSED |

-1 bp |

31-Jan-18 |

-60 |

|

EUR 9m1y1y/9m1y5y Bear Flattener |

28-Dec-17 |

4.2 bp |

EUR 25 k/bp |

CLOSED |

0 bp |

30-Jan-18 |

-130 |

|

Receive GBP/USD 5y5y xccy basis |

28-Dec-17 |

1 bp |

GBP 40 k/bp |

CLOSED |

6.4 bp |

28-Feb-18 |

-297 |

|

EUR 2-5-10 weighted swap fly |

28-Dec-17 |

-28.1 bp |

EUR 40 k/bp |

CLOSED |

-25 bp |

25-Jan-18 |

-154 |

|

GBP 2y-10y Bull-steepener |

05-Jan-18 |

0 bp |

GBP 20 k/bp |

OPEN |

0 bp |

0 |

|

|

EUR 2y2y/5y10y Bull-Steepener |

30-Jan-18 |

0 bp |

EUR 25 k/bp |

CLOSED |

4 bp |

05-Mar-18 |

123 |

|

USD 2y-10y, 1y fwd steepener |

02-Feb-18 |

22 bp |

USD 25 k/bp |

CLOSED |

20.5 bp |

21-Feb-18 |

-38 |

|

GBP/USD 2y-10y 1y fwd Swaps |

21-Feb-18 |

-25.5 bp |

GBP 25 k/bp |

CLOSED |

-10.8 bp |

23-Mar-18 |

521 |

|

GBP 2y-10y vs USD CMS Caps |

21-Feb-18 |

0 bp |

GBP 25 k/bp |

OPEN |

-0.8 bp |

-29 |

|

|

EUR 3y1y/10y10y flattener |

06-Mar-18 |

124 bp |

EUR 25 k/bp |

CLOSED |

120 bp |

08-Mar-18 |

123 |

|

EUR CMS 10-5 collar |

06-Mar-18 |

0.5 bp |

EUR 40 k/bp |

OPEN |

-0.2 bp |

-35 |

|

|

GBP 10-30 vs 2y1y |

27-Mar-18 |

29 bp |

GBP 40 k/bp |

CLOSED |

33.8 bp |

09-Apr-18 |

271 |

|

EUR 3y1y/5y5y bear steepener |

12-Apr-18 |

0 bp |

EUR 40 k/bp |

OPEN |

1.9 bp |

94 |

|

|

GBP/USD 2y-10y, 1m Floors |

20-Apr-18 |

0.6 bp |

GBP 25 k/bp |

OPEN |

0.5 bp |

-4 |

|

|

Total YTD |

711 |

Note on trade sizing: Each trade is sized to generate approx. USD 150k 2y 99% hist. VaR at inception with no netting

David Sansom

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4180

Mobile: +44 (0) 7976 204490

Email: david.sansom@astorridge.com

Web: www.AstorRidge.com

This marketing was prepared by David Sansom, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

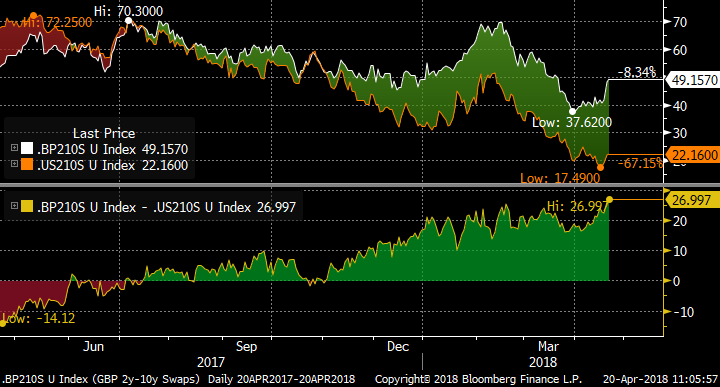

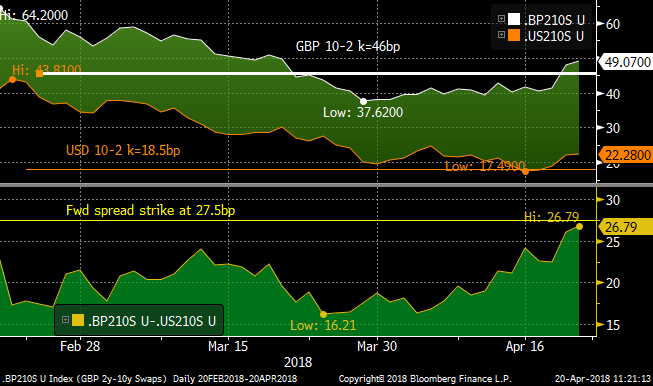

Trade: CMS Floor box GBP 10-2 vs USD 10-2 for a reversal of the Carney-induced UK steepening

Bottom line: This is a trade I have had before, but the Carney-led steepening of the GBP curve relative to the US has brought me back to it: but this time via CMS floors. It is a tactical one month play for a reversal of the steepening, with an expiry that spans the upcoming MPC meeting on 10th May (and the Fed meeting on 2nd May). The GBP/USD 2y-10y box is out of line, but this time I see the risk as further GBP steepening so I am proposing a curve floor structure.

Trade:

Buy GBP 1bn 1m CMS 10-2 floor atmf-2bp (k=46bp)

Sell USD 1.4bn 1m CMS 10-2 floor atmf-2bp (k=18.5bp)

Fwd box strike at 27.5bp, with spot at 26.9bp.

Indicative cost (mid) at 0.6bp running (above notionals are GBP 100k/bp on the underlying curve at expiry).

The spot box: GBP 2y-10y less USD 2y-10y

The strikes displayed graphically on the recent evolution of the US and GBP curves:

Rationale: The UK market had a double-take on Carneys after-hours comments on the likelihood of hikes: with the curve steepening hard on the dovish outlook. This has held today despite Saunders’s repetition of his data-dependent stance. My macro view is that the MPC hikes in May, Carney notwithstanding, but the market’s pricing has the May SONIA at 60bp and the probability of a hike at a shade over 50%.

If there is a hike in May, I’d expect the curve to flatten in GBP, back to (if not through) the 37bp recent low, as long as the statement is not strongly “one and done”. The economic consensus is for UK data to be equivocal at best and we may get a steer that further hikes are not preordained. Even so, the GBP flattening should take the trade through the strike at 46bp.

If May is unchanged, then GBP 2y-10y will steepen further and if recent history is maintained the US curve will steepen in sympathy though to a lesser extent. In this scenario, both floors expire out of the money, but the loss is limited to the premium paid.

During the same one-month period we have the FOMC meeting on 2nd May. The market is pricing a sub-10% chance of a move, though it is possible that the statement may steepen the rate trajectory (we wont get the minutes until after this trade has expired). So there is a small risk of Fed-induce flattening coming out of the US, which is the primary reason for shifting the options 2bp out of the money to take the US curve strike down to the recent flattest in US 2y-10y.

As outlined, the main risk is that the US curve (already very flat) flattens further while the GBP curve does not. If the US flattening is led by a long-end rally (in 10y) then the UK curve should also flatten in the near-term but not by the same amount. The forward strike of the USD floor is 4bp out of the money versus spot and this should mitigate but not eliminate this risk.

As always, any thoughts and comments are appreciated!

Best

David

David Sansom

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4180

Mobile: +44 (0) 7976 204490

Email: david.sansom@astorridge.com

Web: www.AstorRidge.com

This marketing was prepared by David Sansom, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

FX UPDATE...Cable is now looking pretty over stretched and forecasting a reasonable PULLBACK. DXY basing VERY NICELY.!.20.04.2018

- Cable is now looking pretty over stretched and forecasting a reasonable PULLBACK. DXY basing VERY NICELY.

- The EUR USD, is still yet to breach the all-important 1.2167.

- USD EM has seen many BLOW OUT scenarios but a TOP might be in for USD RUB and USD TRY.

- USD CAD has been a major call and bounced well, it now looks poised for its next bout of CAD weakness.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

US CURVE UPDATE ..US CURVES continue to FRUSTRATE but lets see how yesterday PIERCED lows pan out! 19.04.2018

US CURVES continue to FRUSTRATE but let’s see how yesterday PIERCED lows pan out!

It has been very difficult finding a low over the last few weeks DESPITE significant RSI dislocations on ALL monthly durations. Yesterday however we established several downside pierces on the daily charts.

** Trade idea : Between myself and David Sansom we have several trade options that are happy to send and discuss. **

The concern for me is the last 2 days steepening is a reflection of a bearish bond market.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

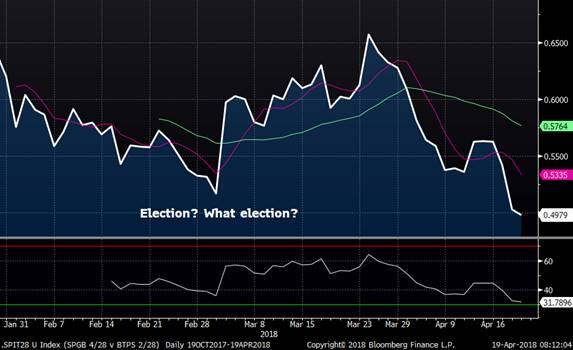

MICROCOSM: SPGBS, FRTRS and UKTs - Quick Preview w/Charts

Quick EGB/UKT Supply Preview:

- Spain will bring 35k RXM8 equivalents at 9:30am Ldn, tapping SPGB .45 10/22s, SPGB 1.4 4/28s and SPGB 2.35 7/33s.

- While Bonos have lagged the impressive move in BTPS this week, they are still just a few bps off the late March yield lows with SPGB-DBR sprds back to the cycle lows. The SPGB 10/22s have cheapened a bit on the curve (4/22-10/22 +2bps this week), the SPGB 4/28s still look on the rich side of fair, as do the 33s.

- We've been fans of the BTPS - SPGB sprd compression trade all week but with the 2/28-4/28 sprd narrowing inside of 50bps this morning, we expect to see some unwinds of long BTPS posns into this am's SPGB 4/28s tap.

SPGB 4/28 v BTPS 2/28

- France's AFT will be bringing 24k RXM8 equivalents in the FRTR 0% 2/21, FRTR 0% 3/23 and FRTR 1.75 11/24.

- Tough to find much 'value' amongst this trio aside from the 11/24s which have backed up on the curve since the announcement of their tap. The 10/22-11/24-11/26 fly is hovering around 7bps this am, the 10/22-11/24 leg steepening into this am's tap, now ~34.6bps mid.

OBL 177 vs FRTR 3/23s – 10bps seems a big level here

FRTR 10/22-11/24-11/26 fly

- The impact of the long awaited EUR 41.7 trillion in C&R flows could be felt a bit in today's auction as the flows officially hit Apr 25th, the settlement of Monday's OATs trades. While most are understandably cautious about fading the move, it seems safe to say the effect of these flows is priced in. Price action in OATM8 has been decidedly dull, RSIs dipping into neutral territory as surging open interest has left the market long. While the fundamental picture for OATs (and EGBs more broadly) doesn’t appear to have any dark clouds on the short term horizon, current yield levels and spreads to bunds leave very little room for error and frankly, I am more comfortable taking off long FRTRs positions here, rolling them into low beta steepeners that should do well if the market chops sideways for a while. Take a look at 5-10/15s steepeners which carry and roll well and are at cycle lows.

- The DMO will tap the UKT 1F 10/28s for the first time at 10:30am, about 24k G M8 equivalents.

- On paper the market should love this issue. It’s the first benchmark longer than the CTD of the gilts contract for a while, it’s got a decent coupon and there’s been enough volatility on the gilts curve to keep the RV guys happy. The trouble is, the 10yr sector looks a bit rich to us and these 10/28s have taken back the pre-tap concession on the curve we saw late last week. For example, the UKT 28-34s flattener we recommended around +17.5bps flattened to +15bps (nice!) then steepened back to +18.8bps on the bounce in G M8 (not nice!) and is opening +18.4bps this am. Same goes for the 26-28-30 fly – cheapened to 15.8bps, now 14.7bps. This tap will get done – they always do – but from an RV perspective they just don’t look as tasty to us.

- More broadly, we think gilts are on rather shaky ground. Yesterday’s CPI data was reason enough to cover shorts (at the very least) but the market focused on the jobs data and with open interest surging 9+% in the last few weeks, there are some skittish positions out there. The charts closed with a bearish and this morning’s open – while likely supply related to a degree – confirms this tone. Tough to chase a rich 10yr sector with this kind of signal.

More to come!

Mark

![]() image009.jpg@01D28D1B.42BD95C0">

image009.jpg@01D28D1B.42BD95C0">

Mark Funsch

O: +44 (0) 203 - 143 - 4177

M: +44 (0) 789 - 996 - 4051

UK: 14-16 Dowgate Hill, London UK EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

This research was prepared by Mark Funsch. He is a consultant with Astor Ridge. A history of his marketing commentaries can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains recommendations, those recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

BOJ's bond buys drop to pre-Kuroda levels

Persistent shortfall from nominal target fuels talk of stealth tapering

April 19, 2018 13:10 JST

The Bank of Japan's purchases of Japanese government bonds have slowed since it shifted its policy focus to yields in 2016. (Photo by Akira Kodaka)

The Bank of Japan's purchases of Japanese government bonds have slowed since it shifted its policy focus to yields in 2016. (Photo by Akira Kodaka)

TOKYO -- The Bank of Japan's purchases of Japanese government bonds have slowed to a pace not seen since the central bank launched its massive monetary easing program, a development that has not escaped the notice of market watchers.

The BOJ reported an increase of just 49.42 trillion yen ($461 billion) in its holdings of long-dated JGBs at the end of March compared with a year earlier, a 13th straight month of slowing growth. This rise also missed the 50 trillion yen target that the central bank set when Gov. Haruhiko Kuroda introduced qualitative and quantitative easing in April 2013. The goal has since been lifted to 80 trillion yen.

New Deputy Gov. Masazumi Wakatabe told upper house lawmakers on Monday that the BOJ is "supplying money to the economy to beat deflation." The outspoken reflation advocate has argued that the bank should aim to lift its JGB holdings by 90 trillion yen a year.

Yet the central bank's long-JGB holdings fell to 426.56 trillion yen at the end of March, down 3.39 trillion yen from a month earlier. This represented the largest monthly decline since June 2008, though the fact that government bonds mature in larger numbers than usual in March played a role, as Mizuho Securities noted.

The BOJ shifted the focus of its monetary policy in 2016 to interest rates rather than the quantity of bonds purchased. Under the yield curve control strategy, the central bank adjusts its JGB purchases to keep long-term interest rates around zero.

The slowdown likely is also an effort to stabilize the market. The BOJ holds 45% of JGBs in circulation, distorting prices and yields.

Its decision to maintain a quantitative bond-buying target despite these factors was a "measure to head off criticism from reflationists," said Takahide Kiuchi of the Nomura Research Institute, who sat on the central bank's policy board until last summer.

The discrepancy between the actual increase in the bank's JGB holdings last fiscal year and the nominal target has been interpreted by some market watchers as a form of stealth tapering.

The BOJ plans to maintain the 80 trillion yen target when the policy board meets April 26 and April 27. Any cuts to this figure would be viewed as a sign of actual tapering, rattling markets. But a widening gap between the target and reality could harm the central bank's credibility.