Many quarterly and monthly BOND YIELD charts are close to confirming a LONGTERM YIELD failure, in a similar fashion to some EQUITY markets.

BONDS UPDATE :

Many quarterly and monthly BOND YIELD charts are close to confirming a LONGTERM YIELD failure, in a similar fashion to some EQUITY markets.

The next BIG TRADE is US STEEPENERS : As mentioned before many RSI’s are WAY over sold and the recent POP to the 61.8% rets served to recognise the BIG BREAK level. If we close above any of the 61.8% rets this should TRIGGER a sustained long-term steepening. Analysing the charts it looks LIKE US 5-30 or 10-30 the ideal steepener in the US.

- Yields are close to breaching levels where we will see a MAJOR DROP

- (US 5yr and UK 10yr). ALL durations are stretched, quarterly, monthly, weekly and daily… this is RARE!

- Looking at the previous Equity piece, European stocks look a LONGTERM failure thus I firmly believe this mean BONDS rally.

3) Germany 26’s bonds based well as do the FUTURES post yesterdays intraday REVERSAL.

4) UK yields have a LOFTY RSI and UKTI POISED to bounce. UK 10yr all eyes on a continued breach of 1.489 (10yr Gilts).

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

FX UPDATE...Cable strength is widening the EUR GBP bollingers. The Euro should fail soon!.17.04.2018

- Cable strength is forcing the EUR GBP bollingers wider confirming this as HUGE trend for the next few years!

- The EUR USD, is still yet to breach the all-important 1.2167.

- USD EM has seen many BLOW OUT scenarios but a TOP might be in for USD RUB and USD TRY.

- USD CAD has been a major call and bounced well from the moving average. This should persist now we are above the 1.300 level.

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Radar Trade - Astor Ridge, James Rice

On my Radar is the following idea

Trade Mechanics

- Sell Btps 4% Feb/37

- Buy Btps 5% Aug/39

- +15% contract curve hedge +RX/-UB

- €50k/DV01, Sell €29.5MM Feb/37 into €25.1MM Aug/39

- And +54 RXM8 contracts & -25 UBM8 contracts

Levels

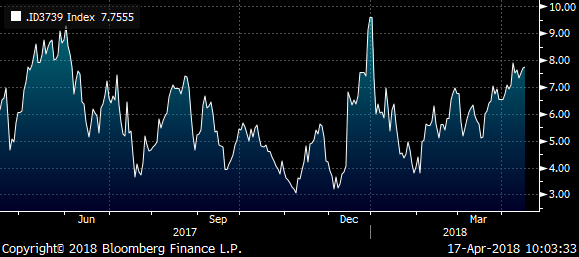

- Current @ +7.8 bp

- Enter @ +8 bp

- Add @ +10 bp

- Target @ +6 bp

- Stop @ +12 bp

Cix & History

100 * ((YIELD[BTPS 5 39 Corp] - YIELD[BTPS 4 2/37 Corp]) - 0.15 * (YIELD[DBR 3.25 7/42 Corp] - YIELD[DBR 0.25 2/27 Corp]))

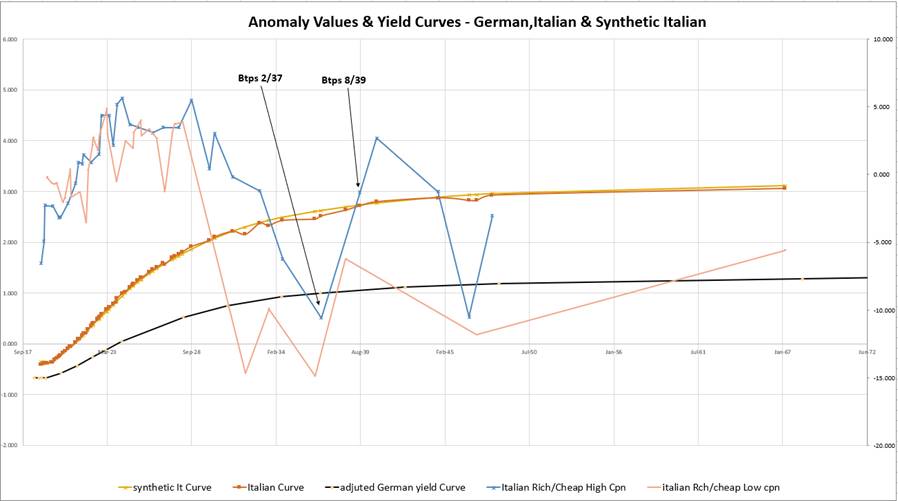

Italian excess return vs Germany

Below is a graph of Anomaly value of Italian curve

- we create this by taking the German curve and multiplying it by a constant and adding a shift – this represents the best fit Italian curve as a marginal excess return function over German bonds

- We then subtract actual Italian bond values from their expected value using this form

- Yields are adjusted to compensate for coupon differences by adding the difference between z-spread and i-spread

Rationale

- After creating a ‘synthetic’ Italian curve using an amplified shape of the German curve we can elucidate the wide range, relative opportunities on the Italian curve

- Generally the Italian curve is approx. 1.8 times as steep as the German curve, and that’s reasonably consistent throughout the curve

- Although the Italian 10s30s segment isn’t quite as steep, we can see that the gradient between high coupon Btps 4% Feb 37 and Btps 5% Aug 39 is significantly steeper than elsewhere

- These specific issues are 1.37 Standard dev rich and 1.16 Standard dev cheap with respect to the Bloomberg GOVY model (Spline Cubic fit, 3M History)

- We use an amount if +RXA vs -UBA to hedge the generic curve movements of European Govt long end -and for hedging efficiency

Carry & Roll

- Btps segment (using 10bp repo spread)

Carry -0.1bp/3mo, Roll -0.3bp/3mo

- RXA/UBA segment (weighted by 15%, using contract implieds)

Carry +0.2bp/3mo, Roll +0.3bp/3mo

- Nett C&R +0.1bp

Risks

- The Btps Feb/37 stay bid due to market shorts

- The Btps Aug/39 stay offered until they hit a wider range notion of cheap

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

Japan's workers win biggest pay raises in 20 years

Logistics and retail lead the way as companies compete for labor

April 16, 2018 13:30 JST

TOKYO -- Japanese workers appear headed for their biggest wage increase in two decades as companies led by the logistics and retail sectors compete for a slice of the country's ever-shrinking workforce.

Businesses lifted wages by an average of 2.41% this year, according to data collected by Nikkei as of April 3. This raise -- made up of base pay and automatic, seniority-based pay -- topped last year's average increase by 0.35 percentage point, the first such growth in three years.

In value terms, monthly pay rose by an average of 7,527 yen ($70), also the highest since 1998.

Rising wages in Japan usually are driven by manufacturers. But nonmanufacturers have taken the lead this year for the first time since 1997. They increased pay by 2.79%, their biggest hike in 21 years and more than half a point above the raises from manufacturers.

Logistics providers and service industry players in particular are working harder to attract employees. Yamato Transport agreed to the full 11,000-yen increase in monthly base pay, or 3.64%, requested by the Yamato Holdings unit's labor union during annual wage negotiations.

The logistics sector enacted an average pay raise of 3.39%, the highest across all industries and the only one with an average increase exceeding 10,000 yen. The industry is struggling to keep pace with the surge in demand for e-commerce shipments.

A Life Corp. supermarket in central Tokyo. The grocery chain will raise wages for both full-time and part-time workers. (Photo by Takuya Imai)

A Life Corp. supermarket in central Tokyo. The grocery chain will raise wages for both full-time and part-time workers. (Photo by Takuya Imai)

Department stores and supermarkets raised wages by 2.53%. Grocery store chain Life Corp. will raise salaries for full-time employees by 3.86%, while also pledging to increase wages for part-time workers.

Manufacturers boosted pay by 2.27%, just 0.18 point more than in 2017. Toyota Motor, which likely posted a record net profit for the fiscal year ended in March, has agreed to a 3.3% pay raise but is not releasing specific yen figures.

Many big electronics makers such as Hitachi and Panasonic are offering just 1,500 yen more in base pay this year. Sony, which is not part of industrywide negotiations with unions, decided on a 5% increase to final yearly pay as the company hopes to attract experts in artificial intelligence and other technologies to boost its competitiveness.

Yet Japanese wages continue to fall in real terms due to rising food and oil prices. The government has urged companies to boost pay for the past five years, and Prime Minister Shinzo Abe gave a specific target for the first time this year, calling for 3% raises.

Businesses are catching on, primarily because they need to secure the talent to compete on the global stage. Many companies are switching away from a seniority-based wage structure and raising starting salaries.

Competition for workers is particularly fierce in the technology sector. Job postings for data scientists have quadrupled in a year, recruitment services provider en-japan said. Companies from China and elsewhere also are luring Japanese graduates away with generous offers.

Some companies are focusing on seniors to overcome labor shortages. West Japan Railway and farm equipment maker Kubota are including post-retirement hires 60 and older in their pay increases. Honda Motor pushed back its retirement age last year and raised pay for senior employees.

The weekends events have done “little” to effect the markets BUT we are failing at the MAJOR bollinger averages therefore the BIAS remains for LOWER.

The weekend’s events have done “little” to effect the markets BUT we are failing at the MAJOR bollinger averages therefore the BIAS remains for LOWER. It will be interesting to see if the bollinger averages work!

** REMEMBER ALL EYES ON EUROPE, ESPECIALLY FTSE, they led the way before **

Post Mark Zuckerberg HOUSE grilling I was personally was not impressed.

It seemed to blame the public for using the platform and freely offering their details. If banks sold peoples personal information, they’d face millions in fines. Am sure regulation will catch up with this sector as long as that is BALANCED with FREE surveillance for government bodies.

The NASDAQ IS NOW close to EMULATING the 2000 DROP (see page 16).

German and UK bonds are helping the cause given they are posting NEW JUNE highs everywhere.

As mentioned I still fancy an old fashioned stocks DOWN bonds UP and bonds are HOLDING.

** KEY CHART FAILURE LEVELS ARE 2, 16 and 17. **

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Week Ahead - James Rice, Astor Ridge

Euro Govts, the week ahead – 16th April to 20th April

Supply

Germany 10y, Wed 18th April - €3Bln 10y

Contract Trade

Seeing 10y as cheap and Rx contracts as rich – like the structure that really revolves around the richness of rx contracts

{DE} +24 -RX +28

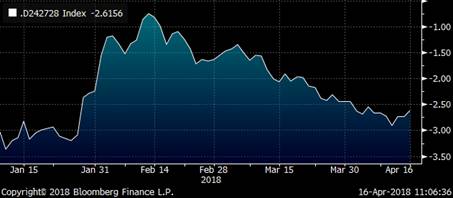

Cix: ((YIELD[DBR 0.25 2/27 Corp] - YIELD[DBR 1.75 2/24 Corp]) - 0.8 * (YIELD[DBR 0.5 2/28 Corp] - YIELD[DBR 1.75 2/24 Corp]))

Weighting: 20/100/80

Currently: -2.6bp,

Target: -3.0 bp, pay the spread

Objective: -1.5bp

Ask for further details and write up

Supply

Spain 4y, 10y & 15y, Thurs 19th April – Est. €4-5Bln

15y trade

15y – micro locally rich on the model, but much better value as a 15y point on the curve relative to Italy or France – generally with an improving credit, the 15y should do well vs 10y and 30y…

For a quick turn like

{ES} -27 +33 -46

cix: 200 * (YIELD[SPGB 2.35 7/33 Corp] - 0.5 * YIELD[SPGB 1.45 10/27 Corp] - 0.5 * YIELD[SPGB 2.9 46 Corp])

Weighting: 100/200/100

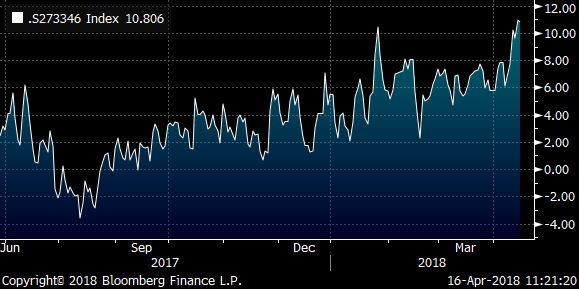

Currently: +11bp

Target: +11.5bp receive the spread, (timing by Wednesday)

Objective: +8bp

Ask for further details and write up

Supply

France 3y, 5y & 6y plus linkers, Thurs 19th April – Est. €6-7Bln

Special tap in Frtr 11/24 (6y)

The 6y to 8y tenor in core trades rich on any fitted curve so not much to say there

France is historically flat 5s10s and on box versus Germany 5s10s, but again this is not wholly inconsistent with ongoing narrowing of the France / Germany credit spread (OAT/RX)

RV 11/24 vs 5/26 trade

Even after accounting for the richness of the German 6y – 8y France still looks over priced here and just see this micro opportunity

{FR} {GE} +frtr nov/24 -frtr May/26 & 28% -OEA/+RX

Cix: 100 * ((YIELD[FRTR 0.5 5/26 Corp] - YIELD[FRTR 1.75 11/24 Corp]) - 0.28 * (YIELD[DBR 0.25 2/27 Corp] - YIELD[DBR 1.5 2/23 Corp]))

Weighting: +100/-100/-28/+28. 24s/26s/oea/rxa

Currently: +5.2bp

Target: +5.0bp pay the spread, (timing by Wednesday)

Objective: +8bp

Ask for further details and write up

More details on the ongoing themes

Love to catch up

James

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su20th Spril

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

**We are entering a potentially explosive situation over the weekend with Syria and MANY equity markets are testing KEY BOLLINGER AVERAGE resistance.**

**We are entering a potentially explosive situation over the weekend with Syria and MANY equity markets are testing KEY BOLLINGER AVERAGE resistance.**

Post Mark Zuckerberg HOUSE grilling I was personally was not impressed.

It seemed to blame the public for using the platform and freely offering their details. If banks sold peoples personal information, they’d face millions in fines. Am sure regulation will catch up with this sector as long as that is BALANCED with FREE surveillance for government bodies.

The NASDAQ IS NOW close to EMULATING the 2000 DROP (see page 16).

German and UK bonds are helping the cause given they are posting NEW JUNE highs everywhere.

As mentioned I still fancy an old fashioned stocks DOWN bonds UP and bonds are HOLDING.

** KEY CHART FAILURE LEVELS ARE 2, 16 and 17. **

-

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

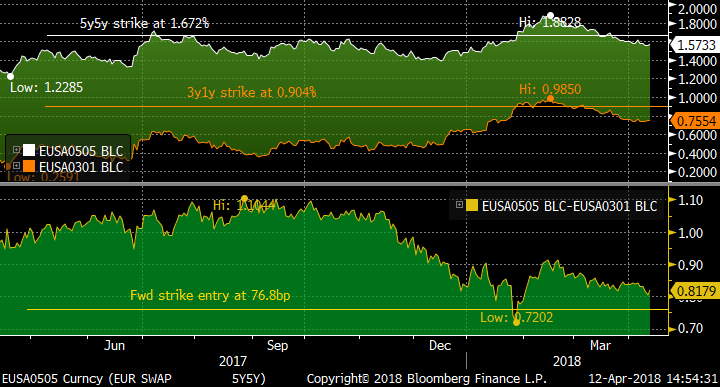

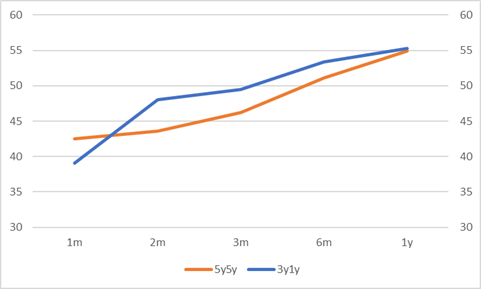

Trade: EUR 3y1y/5y5y tactical bear-steepener based on ECB inaction

Bottom line: Today’s ECB minutes reinforce the reluctance to call an end to accommodation. In light of this, I’m looking at selling the risk of short-rates rising significantly before the June ECB meeting.

Trade:

Sell EUR 995mm 2m3y1y mid-curve payer atmf+10bp (k=0.904%)

Buy EUR 210mm 2m5y5y mid-curve payer atmf+8bp (k=1.672%)

Expiry 14-Jun-18

For zero-cost indicative mid. Equivalent to EUR 100k/bp of the underlying swap.

(ABB 6s on both underlying swaps)

Forward strike entry at 76.8bp, vs spot 3y1y/5y5y at 81.2bp.

Rationale: Over the medium term I see the EUR curve flattening, as the ECB eventually moves to adjusting the deposit rate higher. However today’s Minutes of the 8th March meeting show little indication to rush and if anything reinforce the cautious approach of the majority of board members. To me this was the key section:

“The view was put forward that the Governing Council’s criteria for a sustained adjustment in the path of inflation could be assessed as close to being satisfied over a medium-term horizon. However, the broadly agreed conclusion was that the evidence for a sustained rise in inflation towards levels consistent with the Governing Council’s inflation aim was still not sufficient.”

The next meetings are on 26th April and 14th June, so it is no coincidence that I have chosen a 2m expiry, which comes the morning of the 2nd meeting. The basic premise is that with the ECB sitting on its hands, the realized volatility in the 3y1y rate should undershoot the implied volatility and the realized volatility in longer rates. This reticence is mirrored by the market implied volatility on mid-curve options. The chart shows atm implied volatility for 3y1y and 5y5y mid-curve tails. Implied vol for 1m3y1y is relatively low (certainly lower than 5y5y) and picks up for 2m expiries (to be higher than 5y5y).

Thus it is attractive to sell volatility on 2m3y1y against 2m5y5y. The directionality of the curve has been inconsistent. In the most recent past (ie since mid-Feb) the curve has been bull-flattening. Since the upside to short rates appears capped in the near-term (if my read of the ECB’s intentions is accurate), I am willing to sell payers there and enter a bear-steepener as longer-rates drive the curve.

The vol differential for 2m expiries means that premium can be taken out of the trade. Alternatively, the strike can be set atmf+10bp on the 3y1y and only atmf+8bp on the 5y5y, which gives a further 2bp margin at expiry. In rate terms, the steepener has positive roll-down over the lifetime of the trade. Put together, the forward strike entry is 4.4bp below the spot 3y1y/5y5y spread. In addition, roll-down of the vol surface favours being short vol on 3y1y compared to 5y5y which adds another 0.9bp of rate cushion.

The main risk to the trade is that the market sharply reprices (ie brings forward) the ECB’s tightening of conditions. By moving both payers out of the money (and taking into account the rolldown), I’ve tried to build a buffer but the risk is still there. That said, elsewhere in the ECB statement they nodded to the current risks to global trade so if there were a significant flight to quality move and rally in the belly (eg 5y5y) that might be expected to temper any appetite for rate hikes.

As always, love to hear your thoughts!

Best,

David Sansom

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4180

Mobile: +44 (0) 7976 204490

Email:

Web: www.AstorRidge.com

This marketing was prepared by David Sansom, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796