FX UPDATE...This has been a quiet sector but the EURO still KEY. USD RUB and USD TRY might now have a high. 12.04.2018

- FX UPDATE... The only focus is the EUR USD, which is still yet to breach the all-important 1.2167.

- USD EM has seen many BLOW OUT scenarios but a TOP might be in for USD RUB and USD TRY.

- USD CAD has been a major call and bounced well from the moving average. This should persist now we are above the 1.300 level.

- The EURO is on the brink of a MAJOR statement should we breach the 1.2167.

-

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

US CURVE UPDATE.. FRUSTRATING could be one word, the RSI's remain HISTORICALLY dislocated, we HAVE to BASE soon. .12.042018

US CURVE continue to tease!

This remains well and truly on the RADAR given the MULTI YEAR RSI dislocations and ALL rejected major 61.8% retracements on the last steepening. It is and will be the trade to be in for the next few years, just hard picking a base lately.

The BIGGEST issue is timing and location to PUT ON THE STEEPENER, it has to be soon!

** Trade idea : Between myself and David Sansom we have

3 trade options that are happy to send and discuss. **

Does a stock failure lead to a steepening? I have added an inverse Nasdaq to some charts.

-

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Equity UPDATE .PRE earnings season and Post Mr. Zuckerberg. Stocks have recovered BUT technically need to fail during earnings season to vindicate the quarterly signals. .. . .12.04.2018

Stocks have recovered this month as expected BUT technically need to fail during earnings season to vindicate the quarterly signals.

Post Mark Zuckerberg HOUSE grilling I was personally was not impressed.

It seemed to blame the public for using the platform and freely offering their details. If banks sold peoples personal information, they’d face millions in fines. Am sure regulation will catch up with this sector as long as that is BALANCED with FREE surveillance for government bodies.

The NASDAQ IS NOW close to EMULATING the 2000 DROP (see page 16).

German and UK bonds are helping the cause given they are posting NEW JUNE highs everywhere.

As mentioned I still fancy an old fashioned stocks DOWN bonds UP and bonds are HOLDING.

** KEY CHART FAILURE LEVELS ARE 1, 16 and 17. **

-

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Equity UPDATE .PRE earnings season. Stocks have recovered well BUT technically need to fail during earnings season to vindicate the quarterly signals. .. . .10.04.2018

Equity update as we approach earnings season.

Stocks have recovered well as expected BUT technically need to fail during earnings season to vindicate the quarterly signals. ALL TO PLAY FOR HERE.

The “TECH” sector is the worrying sector.

The NASDAQ IS NOW close to EMULATING the 2000 DROP (see page 16).

German and UK bonds are helping the cause given they are posting NEW JUNE highs everywhere.

As mentioned I still fancy an old fashioned stocks DOWN bonds UP and bonds are HOLDING.

** KEY CHART FAILURE LEVELS ARE 8 and 17. **

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

Bond UPDATE .. ALARM BELLS are ringing. MANY long-term yield charts last month left major UPSIDE BOLLINGER PIERCES, quarterly’s especially. . 10.04.2018.

BONDS UPDATE :

ALARM BELLS are ringing. MANY long-term yield charts last month left major UPSIDE BOLLINGER PIERCES, quarterly’s especially. The US needs a little MORE clarification whilst GERMANY seems ONE WAY already.

Germany and UK, although its quiet the quarterly charts are VERY terminal, we have two MASSIVE reversal rejections. German yields look ONE WAY i.e. LOWER (see page 26).

The next BIG TRADE is US STEEPENERS : As mentioned before many RSI’s are WAY over sold and the recent POP to the 61.8% rets served to recognise the BIG BREAK level.

*****Analysing the charts it looks LIKE US 5-30 or 10-30 the ideal steepener in the US.*****

image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

- UK: 14-16 Dowgate Hill, London EC4R 2SU

- US: 245 Park Ave, 39th Floor, NY, NY, 10167

- Office: +44 (0) 203 143 4174

- Mobile: +44 (0) 7980708683

- Email: chris.williams@astorridge.com

- Web: www.AstorRidge.com

- • I provide our research notification below for your convenience:

- •

- • Research Unbundling:

- •

- • Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

- •

- • If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

- •

- •

- •

- • I also direct you to our disclaimer on our email footer:

- • This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

- •

- • You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

- •

- • Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

- • Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

- • Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

- • Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

- • Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

- •

- •

- • If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

- •

- • Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

- •

- • Many thanks,

- •

- • Chris

BOJ's Kuroda rules out tapering, aims for inflation 'overshoot'

Reappointed central bank chief will monitor impact on private banks' profitability

April 09, 2018 21:52 JST

Governor of the Bank of Japan, Haruhiko Kuroda, speaks at a news conference in Tokyo on April 9.

Governor of the Bank of Japan, Haruhiko Kuroda, speaks at a news conference in Tokyo on April 9.

TOKYO -- Bank of Japan Governor Haruhiko Kuroda began his second term on Monday by declaring he would continue the unprecedented run of monetary easing, even as the U.S. Federal Reserve steadily withdraws its own fiscal stimulus policy.

In a news conference held after he was formally reappointed for a second five-year term by Prime Minister Shinzo Abe, Kuroda said that "it is way too early" to discuss exiting the monetary easing campaign.

He emphasized that the central bank had pledged to keep expanding the country's monetary base even after inflation hits 2%. "It is important to commit to an inflation overshoot," the governor said at a press conference.

Kuroda, who is the first BOJ chief to serve two consecutive terms in 57 years, began his second term amid criticism that he has failed to keep the promise he made in 2013 to achieve 2% inflation in two years. He is also facing complaints from the banking industry for introducing negative interest rates, a decision he made in 2016 that has led to a collapse in interest rates and has made it difficult for commercial banks to earn interest income from their lending operations.

Kuroda said he was aware of the plight the commercial banks face. He said he would "keep a close watch on the effects of the prolonged monetary easing on the health of the banking system." But he stood by his easing measures and the elusive 2% target.

He argued that 2% inflation was a reasonable goal widely adopted by central banks around the world, and stressed that the target had helped bring much-needed stability to the nation's foreign exchange rate.

On Monday, the Japanese yen was trading at about 107 to the U.S. dollar.

Kuroda maintained that the central bank was "making steady progress toward the inflation target." But consumer inflation, excluding volatile fresh food prices, stood at just 1% in February.

The governor's efforts will likely face more challenges ahead. In the near term, the market is concerned about a flare-up of a trade war between the United States and China.

Next year, the nation's sales tax rate will finally be raised to 10% from 8% after two postponements, potentially putting a damper on private consumption. In 2020, the economy is expected to cool after the nation hosts the summer Olympics.

However, Kuroda played down such concerns. According to him, the sales tax increase of 2 percentage points should not produce as big a drag on the economy as it did in 2014, when the tax rate was increased by 3 percentage points to 8%. Consumer necessities, such as food, will also be exempted from the next tax increase, he noted.

He predicted that private-sector investment would pick up the slack in public-sector investment, which has been running high as preparations are made for the Olympics.

Earlier on Monday, Prime Minister Abe met with Kuroda and asked him to "mobilize all policy tools available" to lift the country out of its decades-long deflation. Kuroda responded by promising to "make maximum efforts."

Kuroda said that Abe made no specific policy requests during their meeting.

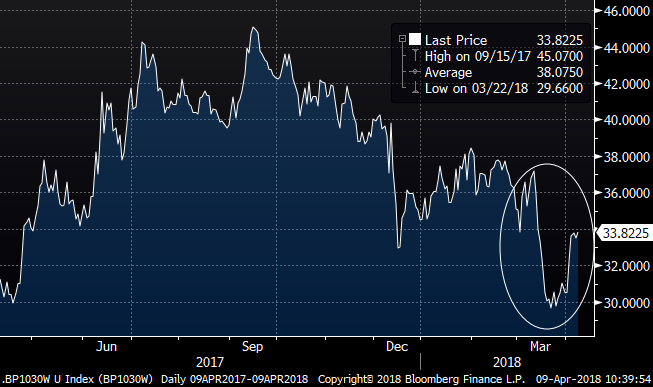

Portfolio update: Closing out "Tactical Year-end Trade: GBP 10-30 steepener hedged with short-rates"

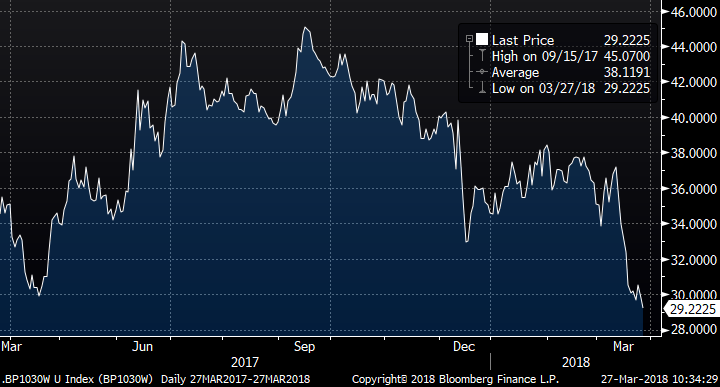

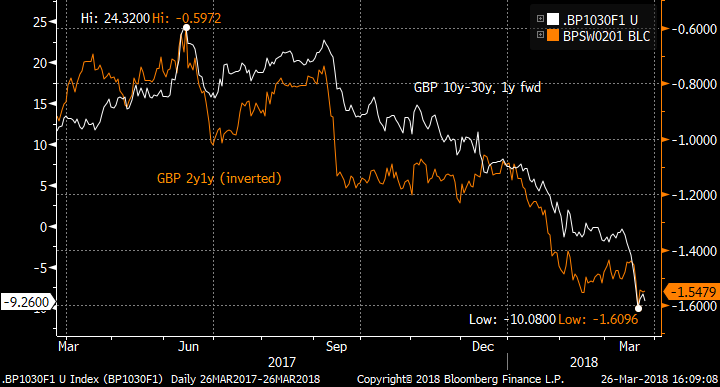

At the tail-end of March, I suggested fading the idiosyncratic flattening of the GBP 10-30 curve, as it was out of line with short rate expectations (eg the 2y1y rate) on the run-in to the fiscal year-end in the UK.

The trade has reverted a good deal since then, and with the 30y Gilt auction tomorrow I’m booking the gains here at 33.8 bp, having entered at 29bp.

Thanks to George Whitehead for his sage advice on the Gilt market, and the flows driving it.

Best wishes,

David

The original write-up:

Bottom-line: GBP 10-30 has flattened too far relative to short-rate expectations, as demand of long-end UK paper has outstripped supply in the thin market ahead of fiscal year-end. Set a tactical steepener, hedged with a regression-weighted amount of short-rates. One to look at today, ahead of this afternoon’s long-end APF.

Trade:

Recv GBP 107mm 1y10y swap

Pay GBP 40.5mm 1y30y swap

Pay 255mm 2y1y swap

(equivalent to GBP 100k/bp on the 10y-30y and 25k/bp of 2y1y)

Positive rolldown of +0.5bp over the first 3m.

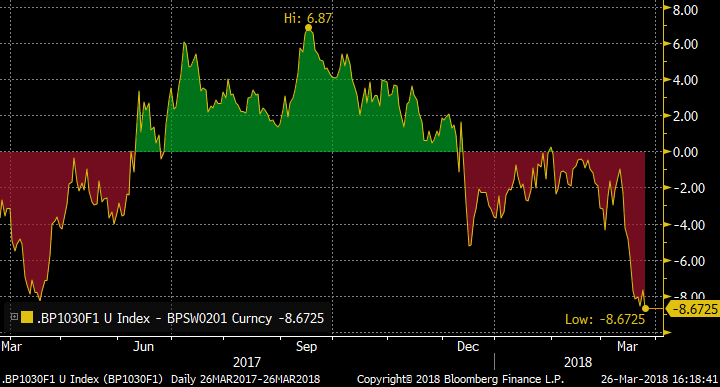

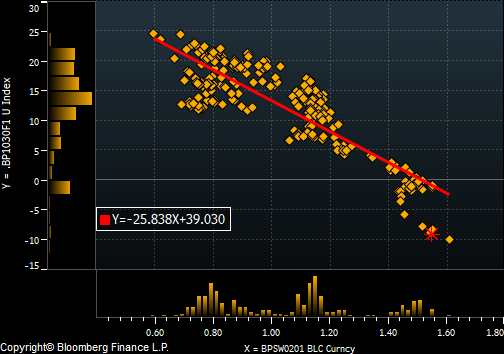

Bloomberg CIX for the relationship:

100 * (BPSW0130 Curncy - BPSW0110 Curncy) + 25 * BPSW0201 Curncy

On this index, enter at 29. Target 36bp. Stop at 26.5bp.

The residual of the 10-30 vs 25% 2y1y regression (using the 1:0.25 weights):

Rationale: For the past year, as the UK has moved towards a hiking cycle, the long-end curve slope has been correlated with the short rate (as exemplified by 2y1y) as it has in the US. However in the past month, the 10-30 curve has flattened further as supply/demand in the 30y sector of the Gilt market takes over. With month- / quarter- / fiscal year-end approaches in the next few days, long-end paper has gone “missing” and liquidity has drained away. End-users have petitioned the DMO for more long-end supply, and the GEMMs asking for the next long-end auction (of the 1t 57) to be brought forward: which it has been by a week to 10th April.

The catalyst for a reversal of this long-end richness could come today with the long-end APF, where the street is likely to offer in 57s in decent size (going short to cover at the auction). Once the year-end is done, the squeeze should abate further as the coming supply looms.

This is a tactical trade for the short-term, as factors exogenous to the UK could drive a further flattening. The 2y1y hedge might break down if there are major changes in rate expectations, so the stop is tight and the horizon of the trade should be one to two weeks.

The level regression has an R^2 of 77%.

Love to hear your thoughts!

Best wishes

David

David Sansom

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4180

Mobile: +44 (0) 7976 204490

Email: david.sansom@astorridge.com

Web: www.AstorRidge.com

This marketing was prepared by David Sansom, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

: Gilts £2bn 1t2057 A Cheap issue-Flytime sell 2h65s into 1t57 & 3h68s...

April has started with a healthy correction in Super-Longs yields from the sub 1.50% level for end of Q1 as the BOE approaches the end of their current reinvestment with 2 Long operations left tomorrow & next Tuesday. Tomorrow the DMO offer £2bn 1t2057s a cheap issue which has been left behind with an outperformance of 20 year & 50 year during the QE reinvestment,now seems a good time to shuffle the deckchairs & sell 2h65s which led the super-long charge in March into 1t57s & 3h68s or merely move 15/20 year into 57s tomorrow & end up closer to the destination new 2070/2073 issue which is likely to be Opened by Syndication mid/Late May. Fly Details:  Entry +5.2 Target:2.5bps.. Stop 6bps.

Entry +5.2 Target:2.5bps.. Stop 6bps.

This marketing was prepared by George Whitehead, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

<< "The Past Is The Future Back To Basics" 02031434182-www.astorridge.com >>

Bank of Japan overtakes foreign investors as top buyer of stocks

Central bank accounts for highest net purchases in Abenomics era

April 06, 2018 06:37 JST

The Bank of Japan, headquarters above, has become a major support for Tokyo Stock Exchange equities. (Photo by Kaisuke Ota)

The Bank of Japan, headquarters above, has become a major support for Tokyo Stock Exchange equities. (Photo by Kaisuke Ota)

TOKYO -- The Bank of Japan has surpassed overseas investors to become the largest net buyer of Japanese stocks since the launch of Abenomics in late 2012, suggesting the market's heavy dependence on the central bank.

Foreigners bought about 12 trillion yen ($111 billion at current rates) more in Japanese stocks than they sold between November 2012 and the end of March 2018, according to Tokyo Stock Exchange operator Japan Exchange Group. The BOJ purchased about 18 trillion yen in exchange-traded funds over this period, central bank data shows.

The stock market rally under Abenomics, the signature economic program of Prime Minister Shinzo Abe, was initially driven by bullish overseas investors. But they began pulling back in mid-2015, with net stock purchases since November 2012 peaking at more than 20 trillion yen that May. Net sales by foreign investors came to 625.5 billion yen last fiscal year.

Japanese stocks look like a relative bargain, said Emmanuel Bourdeix, CEO of Seeyond, part of the Natixis group, based in France. But fears of a global economic slowdown and uncertainty about the pace of U.S. interest rate hikes have spurred a sharp drop in overall stock weightings, he said.

Japan's stock market is heavy on exporters, which tend to be sensitive to global economic conditions. Concern that the yen's continued strength against the dollar will weigh on previously strong corporate earnings has fueled the outflow of foreign capital. And recent scandals have shaken the faith in the stability of Abe's government that had underpinned the Abenomics rally, prompting hedge funds to turn instead to emerging markets and elsewhere.

The BOJ, which buys exchange-traded funds as part of its campaign to lift inflation to 2%, is filling the void. Its annual purchases have risen gradually from 1 trillion yen in 2013, just after the start of its massive monetary easing program, to a record 6.17 trillion yen in fiscal 2017. The central bank's ETF holdings stood at an estimated 24 trillion yen at fiscal year-end based on current market value -- nearly 4% of the total market capitalization of Japanese stocks.

Since the BOJ tends to buy on dips, it is unlikely to do much to drive share prices higher. Rekindled interest among foreign investors, who account for the majority of trading, will be needed to bring back real upward momentum.

Some overseas market players with long time horizons see promise in Japanese stocks. Daniel Farley, chief investment officer of the investment solutions group at State Street Global Advisors in the U.S., expects monetary easing to continue and corporate governance to improve. A softer yen may also lure back foreign money on hopes of renewed earnings growth.

BOJ Gov. Haruhiko Kuroda has stressed that the ETF purchases have played a major role in bolstering the economy and inflation. But the stock market's growing reliance on central bank activity has some analysts worried about pricing distortions.

The PSPP2 data for Germany for March-18. Estimated WAM of Bund purchases at 7.9 years in the month.

Yesterday, the ECB released the PSPP2 data for March purchasing. The main points taken from my PSPP2 model:

- The WAM of German purchases fell back to 7.7 years in March, from 9.1 years in February;

- The estimated volume on Lander (or non-KFW) also reduced back to the more usual level (2.2bn down to 1.4bn)

- I estimate 0.85bn of redemption reinvestment flows in March

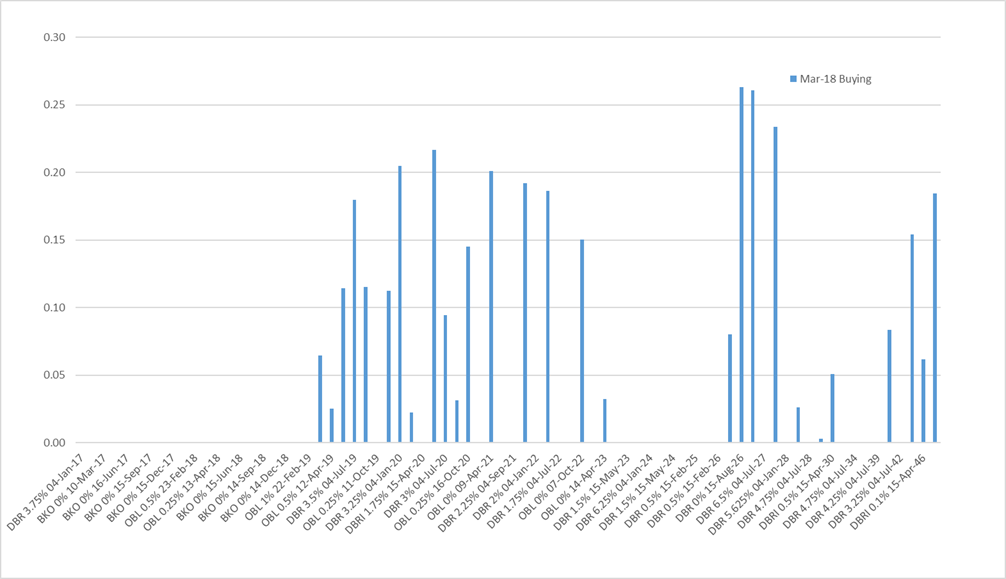

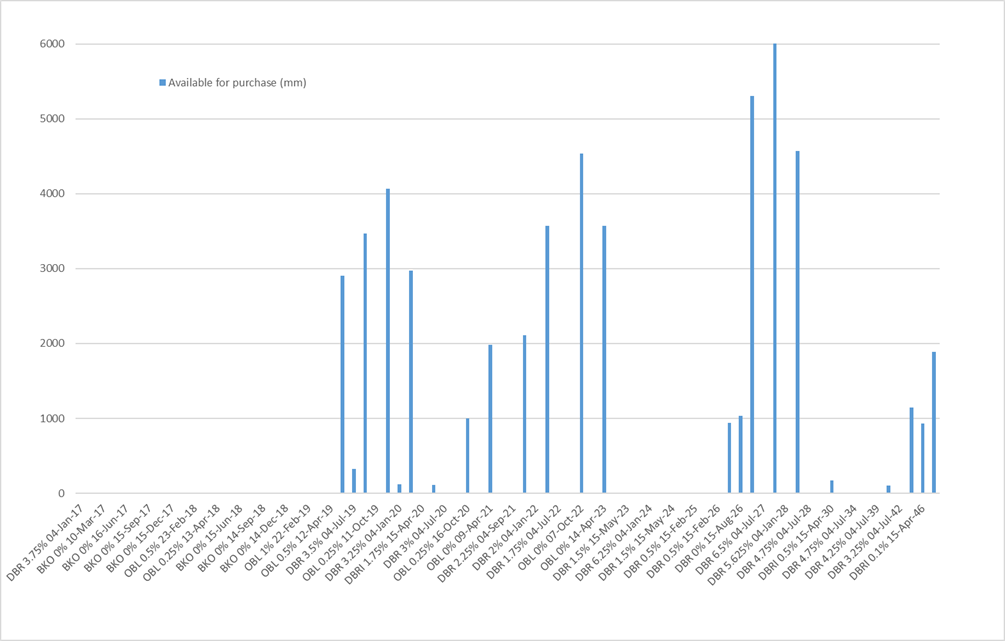

- Again, the largest per-issue purchases came in the 10y sector

- The model still shows minimal buying of the current 30y (Aug-48)

- The new Schatz (BKO 0% Mar-20) appeared in the Buba’s repo list at the end of March, so they have bought some (my model has 20mm)

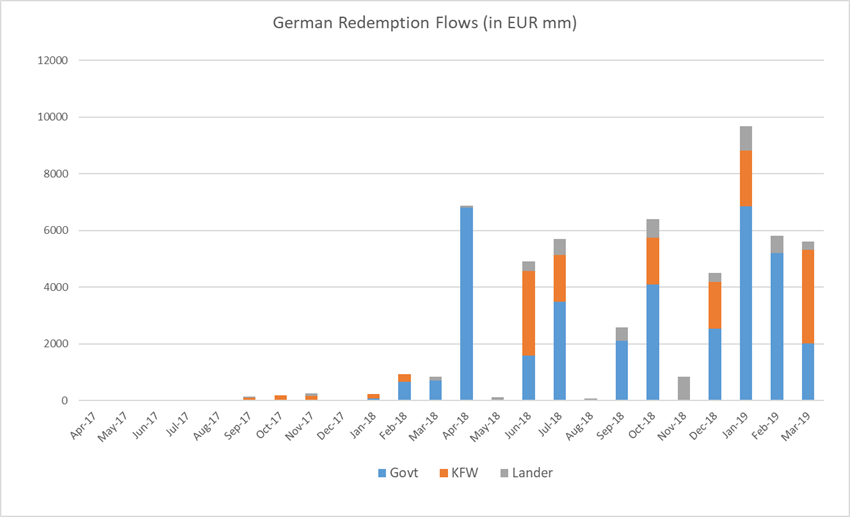

The jury is still out on the impact of new month’s redemptions. My model suggests that nearly 6.8bn of Bunds will come out of the portfolio in April. Some of this will come from the OBL 0.25% Apr-18 (my estimate is 2.1bn) but the bulk is from the OBLei Apr-18 linker (4.7bn). Unfortunately all we know about the Buba and linkers is that they have bought at least some (the securities are available for lending), but that’s about it. Because they have been eligible for purchase from Day One of QE, my model has them bought all the way to the 33% issue limit, however the Buba may have a different treatment (also the treatment of the inflation uplift is unclear: does the Buba retain the inflation uplift in principal or does it get reinvested?).

The model’s results in detail:

The estimate for the WAM for purchases in January for the various categories of paper are as follows:

|

Category |

Notional |

WAM |

|

German Govt |

3.5 |

7.9 |

|

KFW |

0.5 |

8.1 |

|

Others (Lander) |

1.4 |

7.2 |

|

All Purchases |

5.4 |

7.7 |

The per-issue charts for monthly purchases, and available notional left to purchase:

Given the model’s estimates for purchasing, here is how I see the redemption flows in Bunds currently. Numbers for Apr-19 onwards will continue to rise as more purchases are made.

|

Redemptions |

||||

|

Govt |

KFW |

Lander |

Total |

|

|

Apr-17 |

0 |

0 |

0 |

0 |

|

May-17 |

0 |

0 |

0 |

0 |

|

Jun-17 |

0 |

0 |

0 |

0 |

|

Jul-17 |

0 |

0 |

0 |

0 |

|

Aug-17 |

0 |

0 |

0 |

0 |

|

Sep-17 |

0 |

101 |

47 |

148 |

|

Oct-17 |

6 |

188 |

0 |

193 |

|

Nov-17 |

0 |

164 |

90 |

254 |

|

Dec-17 |

0 |

0 |

0 |

0 |

|

Jan-18 |

73 |

153 |

0 |

226 |

|

Feb-18 |

657 |

278 |

0 |

935 |

|

Mar-18 |

710 |

0 |

137 |

847 |

|

Apr-18 |

6800 |

0 |

71 |

6871 |

|

May-18 |

0 |

0 |

114 |

114 |

|

Jun-18 |

1596 |

2970 |

340 |

4906 |

|

Jul-18 |

3478 |

1650 |

580 |

5708 |

|

Aug-18 |

0 |

0 |

81 |

81 |

|

Sep-18 |

2112 |

0 |

466 |

2579 |

|

Oct-18 |

4100 |

1650 |

650 |

6400 |

|

Nov-18 |

0 |

0 |

850 |

850 |

|

Dec-18 |

2540 |

1650 |

321 |

4511 |

|

Jan-19 |

6847 |

1980 |

860 |

9687 |

|

Feb-19 |

5196 |

0 |

626 |

5822 |

|

Mar-19 |

2010 |

3300 |

305 |

5615 |

|

Apr-19 |

5280 |

272 |

765 |

6316 |

|

May-19 |

0 |

0 |

561 |

561 |

|

Jun-19 |

1389 |

0 |

493 |

1882 |

|

Jul-19 |

7594 |

495 |

97 |

8186 |

|

Aug-19 |

0 |

660 |

336 |

996 |

|

Sep-19 |

818 |

0 |

642 |

1461 |

|

Oct-19 |

5280 |

1650 |

1921 |

8851 |

|

Nov-19 |

0 |

0 |

357 |

357 |

|

Dec-19 |

226 |

0 |

500 |

725 |

|

Jan-20 |

7141 |

3300 |

1583 |

12024 |

|

Feb-20 |

0 |

16 |

596 |

612 |

|

Mar-20 |

0 |

0 |

1298 |

1298 |

|

Apr-20 |

11771 |

0 |

113 |

11885 |

|

May-20 |

0 |

0 |

330 |

330 |

|

Jun-20 |

0 |

1650 |

543 |

2193 |

|

Jul-20 |

7259 |

0 |

1555 |

8814 |

|

Aug-20 |

0 |

0 |

481 |

481 |

|

Sep-20 |

5280 |

0 |

702 |

5982 |

|

Oct-20 |

5273 |

495 |

533 |

6301 |

|

Nov-20 |

0 |

0 |

1062 |

1062 |

|

Dec-20 |

0 |

0 |

740 |

740 |

|

Jan-21 |

6270 |

3630 |

939 |

10839 |

Or, in chart form:

Finally, here are the per-issue estimates for Bunds:

|

Bond |

Opened |

O/S (bn) |

Purchasable |

Market Yield |

Purchased |

% Purchased |

Remaining |

Margin of Error |

MV Remaining |

Mar-18 Buying |

|

DBR 3.75% 04-Jan-17 |

Nov-06 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

OBL 0.75% 24-Feb-17 |

Jan-12 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

BKO 0% 10-Mar-17 |

Feb-15 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

OBL 0.5% 07-Apr-17 |

May-12 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

BKO 0% 16-Jun-17 |

May-15 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

DBR 4.25% 04-Jul-17 |

May-07 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

BKO 0% 15-Sep-17 |

Aug-15 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

OBL 0.5% 13-Oct-17 |

Sep-12 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

+/- 45% |

0.0 |

0.0 |

|

BKO 0% 15-Dec-17 |

Nov-15 |

0.0 |

0.0 |

|

0.0 |

|

0.0 |

|

0.0 |

0.0 |

|

DBR 4% 04-Jan-18 |

Nov-07 |

0.0 |

0.0 |

|

0.1 |

|

0.0 |

+/- 9% |

0.0 |

0.0 |

|

OBL 0.5% 23-Feb-18 |

Jan-13 |

0.0 |

0.0 |

0.7 |

0.0 |

+/- 3% |

0.0 |

0.0 |

||

|

BKO 0% 16-Mar-18 |

Feb-16 |

0.0 |

0.0 |

0.7 |

0.0 |

+/- 4% |

0.0 |

0.0 |

||

|

OBL 0.25% 13-Apr-18 |

May-13 |

17.0 |

0.0 |

-0.752 |

2.1 |

0.0 |

+/- 2% |

0.0 |

0.0 |

|

|

OBLI 0.75% 15-Apr-18 |

Apr-11 |

15.0 |

0.0 |

4.7 |

0.0 |

+/- 1% |

0.0 |

0.0 |

||

|

BKO 0% 15-Jun-18 |

May-16 |

14.0 |

0.0 |

-0.680 |

1.6 |

0.0 |

+/- 3% |

0.0 |

0.0 |

|

|

DBR 4.25% 04-Jul-18 |

May-08 |

21.0 |

0.0 |

-0.700 |

3.5 |

0.0 |

+/- 1% |

0.0 |

0.0 |

|

|

BKO 0% 14-Sep-18 |

Aug-16 |

13.0 |

0.0 |

-0.671 |

2.1 |

0.0 |

+/- 2% |

0.0 |

0.0 |

|

|

OBL 1% 12-Oct-18 |

Sep-13 |

17.0 |

0.0 |

-0.678 |

4.1 |

0.0 |

+/- 2% |

0.0 |

0.0 |

|

|

BKO 0% 14-Dec-18 |

Nov-16 |

13.0 |

0.0 |

-0.670 |

2.5 |

0.0 |

+/- 2% |

0.0 |

0.0 |

|

|

DBR 3.75% 04-Jan-19 |

Nov-08 |

24.0 |

0.0 |

-0.710 |

6.8 |

0.0 |

+/- 1% |

0.0 |

0.0 |

|

|

OBL 1% 22-Feb-19 |

Jan-14 |

16.0 |

0.0 |

-0.675 |

5.2 |

0.0 |

+/- 1% |

0.0 |

0.0 |

|

|

BKO 0% 15-Mar-19 |

Mar-17 |

13.0 |

0.0 |

-0.677 |

2.0 |

|

0.0 |

+/- 2% |

0.0 |

0.1 |

|

OBL 0.5% 12-Apr-19 |

May-14 |

16.0 |

5.3 |

-0.674 |

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

BKO 0% 14-Jun-19 |

May-17 |

13.0 |

4.3 |

-0.648 |

1.4 |

32% |

2.9 |

+/- 2% |

2.9 |

0.1 |

|

DBR 3.5% 04-Jul-19 |

May-09 |

24.0 |

7.9 |

-0.648 |

7.6 |

96% |

0.3 |

+/- 1% |

0.4 |

0.2 |

|

BKO 0% 13-Sep-19 |

Aug-17 |

13.0 |

4.3 |

-0.646 |

0.8 |

19% |

3.5 |

+/- 3% |

3.5 |

0.1 |

|

OBL 0.25% 11-Oct-19 |

Sep-14 |

16.0 |

5.3 |

-0.633 |

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

BKO 0% 13-Dec-19 |

Nov-17 |

13.0 |

4.3 |

-0.631 |

0.2 |

5% |

4.1 |

+/- 6% |

4.1 |

0.1 |

|

DBR 3.25% 04-Jan-20 |

Nov-09 |

22.0 |

7.3 |

-0.633 |

7.1 |

98% |

0.1 |

+/- 1% |

0.1 |

0.2 |

|

BKO 0% 13-Mar-20 |

Feb-18 |

9.0 |

3.0 |

-0.596 |

0.0 |

0% |

3.0 |

|

3.0 |

0.0 |

|

DBRI 1.75% 15-Apr-20 |

Jun-09 |

16.0 |

5.3 |

|

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 17-Apr-20 |

Jan-15 |

20.0 |

6.6 |

-0.582 |

6.5 |

98% |

0.1 |

+/- 1% |

0.1 |

0.2 |

|

DBR 3% 04-Jul-20 |

Apr-10 |

22.0 |

7.3 |

-0.559 |

7.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.1 |

|

DBR 2.25% 04-Sep-20 |

Aug-10 |

16.0 |

5.3 |

-0.541 |

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0.25% 16-Oct-20 |

Jul-15 |

19.0 |

6.3 |

-0.534 |

5.3 |

84% |

1.0 |

+/- 1% |

1.0 |

0.2 |

|

DBR 2.5% 04-Jan-21 |

Nov-10 |

19.0 |

6.3 |

-0.496 |

6.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 09-Apr-21 |

Feb-16 |

21.0 |

6.9 |

-0.451 |

4.9 |

71% |

2.0 |

+/- 1% |

2.0 |

0.2 |

|

DBR 3.25% 04-Jul-21 |

Apr-11 |

19.0 |

6.3 |

-0.410 |

6.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 2.25% 04-Sep-21 |

Aug-11 |

16.0 |

5.3 |

-0.371 |

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 08-Oct-21 |

Jul-16 |

19.0 |

6.3 |

-0.361 |

4.2 |

66% |

2.1 |

+/- 2% |

2.1 |

0.2 |

|

DBR 2% 04-Jan-22 |

Nov-11 |

20.0 |

6.6 |

-0.321 |

6.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 08-Apr-22 |

Feb-17 |

18.0 |

5.9 |

-0.277 |

2.4 |

40% |

3.6 |

+/- 2% |

3.6 |

0.2 |

|

DBR 1.75% 04-Jul-22 |

Apr-12 |

24.0 |

7.9 |

-0.256 |

7.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1.5% 04-Sep-22 |

Sep-12 |

18.0 |

5.9 |

-0.222 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 07-Oct-22 |

Jul-17 |

17.0 |

5.6 |

-0.188 |

1.1 |

19% |

4.5 |

+/- 3% |

4.6 |

0.2 |

|

DBR 1.5% 15-Feb-23 |

Jan-13 |

18.0 |

5.9 |

-0.151 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

OBL 0% 14-Apr-23 |

Feb-18 |

11.0 |

3.6 |

-0.090 |

0.1 |

2% |

3.6 |

+/- 10% |

3.6 |

0.0 |

|

DBRI 0.1% 15-Apr-23 |

Mar-12 |

16.0 |

5.3 |

|

5.3 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1.5% 15-May-23 |

May-13 |

18.0 |

5.9 |

-0.101 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 2% 15-Aug-23 |

Sep-13 |

18.0 |

5.9 |

-0.055 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 6.25% 04-Jan-24 |

Jan-94 |

10.3 |

3.4 |

-0.004 |

3.4 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1.75% 15-Feb-24 |

Jan-14 |

18.0 |

5.9 |

0.022 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1.5% 15-May-24 |

May-14 |

18.0 |

5.9 |

0.056 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1% 15-Aug-24 |

Sep-14 |

18.0 |

5.9 |

0.091 |

5.9 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 0.5% 15-Feb-25 |

Jan-15 |

23.0 |

7.6 |

0.151 |

7.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 1% 15-Aug-25 |

Jul-15 |

23.0 |

7.6 |

0.204 |

7.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 0.5% 15-Feb-26 |

Jan-16 |

26.0 |

8.6 |

0.269 |

8.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBRI 0.1% 15-Apr-26 |

Mar-15 |

13.5 |

4.5 |

|

3.5 |

79% |

0.9 |

+/- 2% |

1.1 |

0.1 |

|

DBR 0% 15-Aug-26 |

Jul-16 |

25.0 |

8.3 |

0.333 |

7.2 |

88% |

1.0 |

+/- 1% |

1.0 |

0.3 |

|

DBR 0.25% 15-Feb-27 |

Jan-17 |

26.0 |

8.6 |

0.389 |

3.3 |

38% |

5.3 |

+/- 1% |

5.2 |

0.3 |

|

DBR 6.5% 04-Jul-27 |

Jul-97 |

11.2 |

3.7 |

0.380 |

3.7 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 0.5% 15-Aug-27 |

Jul-17 |

25.0 |

8.3 |

0.452 |

1.2 |

14% |

7.1 |

+/- 2% |

7.1 |

0.2 |

|

DBR 5.625% 04-Jan-28 |

Jan-98 |

14.5 |

4.8 |

0.450 |

4.8 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 0.5% 15-Feb-28 |

Jan-18 |

14.0 |

4.6 |

0.513 |

0.1 |

1% |

4.6 |

+/- 11% |

4.6 |

0.0 |

|

DBR 4.75% 04-Jul-28 |

Oct-98 |

11.3 |

3.7 |

0.495 |

3.7 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 6.25% 04-Jan-30 |

Jan-00 |

9.3 |

3.1 |

0.571 |

3.1 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBRI 0.5% 15-Apr-30 |

Apr-14 |

10.0 |

3.3 |

|

3.1 |

95% |

0.2 |

+/- 2% |

0.2 |

0.0 |

|

DBR 5.5% 04-Jan-31 |

Oct-00 |

17.0 |

5.6 |

0.649 |

5.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 4.75% 04-Jul-34 |

Jan-03 |

20.0 |

6.6 |

0.823 |

6.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 4% 04-Jan-37 |

Jan-05 |

23.0 |

7.6 |

0.915 |

7.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 4.25% 04-Jul-39 |

Jan-07 |

14.0 |

4.6 |

0.973 |

4.6 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 4.75% 04-Jul-40 |

Jul-08 |

16.0 |

5.3 |

0.988 |

5.2 |

98% |

0.1 |

+/- 1% |

0.2 |

0.1 |

|

DBR 3.25% 04-Jul-42 |

Jul-10 |

15.0 |

5.0 |

1.051 |

5.0 |

100% |

0.0 |

+/- 0% |

0.0 |

0.0 |

|

DBR 2.5% 04-Jul-44 |

Apr-12 |

23.5 |

7.8 |

1.106 |

6.6 |

85% |

1.1 |

+/- 1% |

1.5 |

0.2 |

|

DBRI 0.1% 15-Apr-46 |

Jun-15 |

7.0 |

2.3 |

|

1.4 |

60% |

0.9 |

+/- 2% |

1.1 |

0.1 |

|

DBR 2.5% 15-Aug-46 |

Feb-14 |

23.0 |

7.6 |

1.125 |

5.7 |

75% |

1.9 |

+/- 1% |

2.6 |

0.2 |

|

DBR 1.25% 15-Aug-48 |

Sep-17 |

7.0 |

2.3 |

1.166 |

0.2 |

9% |

2.1 |

+/- 5% |

2.2 |

0.0 |

|

Italic = index-linked |

Total |

57.8 |

3.5 |

|||||||

|

Yield below Depo Floor |

||||||||||

|

Yield above Depo Floor |

Bund WAM |

7.9 |

David Sansom

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4180

Mobile: +44 (0) 7976 204490

Email: david.sansom@astorridge.com

Web: www.AstorRidge.com

This marketing was prepared by David Sansom, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796