• Equities starting to liven up as some QUARTERLY charts look TERMINAL.

• Equities starting to liven up as some QUARTERLY charts look TERMINAL.

• I.E. Quarterly CAC, FTSE and especially DAX, others like DOW and NASDAQ look positive.

• ** SEE DAX CHART PAGE 11! **

• MANY bounces have been VERY LAME.

• US stocks remain the most over bought and many have recovered MORE than 200% of the 2008-2009 correction.

• The DOW and S&P have major RSI dislocations spread across monthly, weekly and daily durations! This is a DANGEROUS combination.

• Some RSI’s surpass 1950 and 1980 levels.

• US stocks highlight the most CONCERN.

• ** HAPPY TO DISCUSS ANY CHARTS **

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4174

Mobile: +44 (0) 7980708683

Email: chris.williams@astorridge.com

Web: www.AstorRidge.com

• I provide our research notification below for your convenience:

•

• Research Unbundling:

•

• Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

•

• If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

•

•

•

• I also direct you to our disclaimer on our email footer:

• This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

•

• You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

•

• Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

• Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

• Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

• Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

• Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

•

•

• If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

•

• Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

•

• Many thanks,

•

• Chris

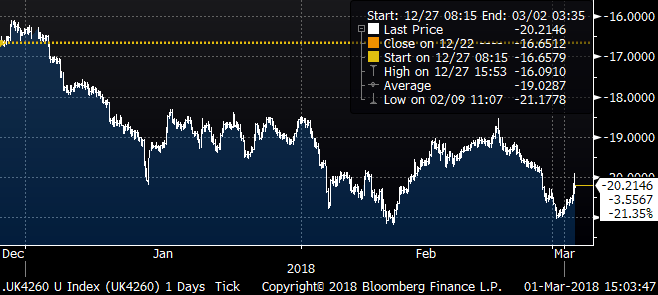

UKT 42s60s Steepener

From: Jim Lockard

Sent: 01 March 2018 18:48

|

UKT SPREAD |

|

YIELD |

|

|

|

|

|

OAS |

|

|

|

|

|

YY |

|

29-Jun |

|

|

|

Spot |

Frwrd |

Carry |

Roll |

RV |

NET |

Spot |

Frwrd |

Carry |

Roll |

RV |

NET |

Spot |

Fwrd |

REPO |

|

4.5 12/42 |

Buy |

1.881 |

1.908 |

2.7 |

0.0 |

0.2 |

2.8 |

-21.5 |

-22.2 |

0.9 |

0.1 |

0.1 |

1.2 |

-20.9 |

-21.8 |

0.525 |

|

4 1/60 |

Sell |

1.679 |

1.694 |

-1.5 |

0.3 |

0.0 |

-1.2 |

-11.8 |

-12.1 |

-0.5 |

0.1 |

0.0 |

-0.4 |

-14.6 |

-15.2 |

0.525 |

|

|

|

-20.21 |

-21.35 |

1.14 |

0.30 |

0.20 |

1.64 |

-9.70 |

-10.05 |

0.37 |

0.21 |

0.14 |

0.72 |

-6.27 |

-6.6 |

|

Entry: -20.0 bps or better

Target: -14 to -16 bps

Stop: -22.0 bps

We’ve held current levels post Brexit referendum in June 2016, during massive de-risking episode, and 4 times since:

2018 tic chart:

RATIONALE:

- 20yr point set to outperform in 2018 due to Solvency II rollback post Brexit (which will incentivise UK insurers to repatriate liability hedges concentrated in 15-30yr back to Gilts; currently Gilts are not eligible for EU CSA collateral)

- LDI needs shortening with flexible drawdown pensions

- Ultras are being richened by the dealer community in anticipation of APF reinvestment later this month

- The 42s60s has exhibited mean reverting behaviour with the 2yr range mostly between -13 to -21 bps

- The -20/21 area has previously held 4 times, the last time during November’s massive linker index extension; it also held in the aftermath of Brexit

- The trade earns positive carry of nearly 1bp per quarter (i.e. UKT 42s60s 1yr forward = -24.0 bps)

- The 42s are near the peak of the curve and enjoy positive roll, whereas 60s roll negatively and are the richest ultra long on Z spread:

|

|

SETTLE |

02-Mar-18 |

|

|

04-Jun-18 |

=3m |

|

|

|

ASSET SWAP |

|

|

MM SWAP SPREAD - Semi6's |

|

|

|

122.55 |

122.55 |

|

|

0.555 |

29-Mar-18 |

=Futures |

|

|

OAS |

|

YY |

|

LIBOR |

|

|

|

BOND |

PRICE |

YIELD |

CHNG |

0.525 |

29-Jun-18 |

CARRY |

ROLL |

RV |

NET |

Spot |

Frwrd |

Spot |

Chnge |

Carry |

Roll |

|

1.75 9/37 |

97.979 |

1.874 |

-7.7 |

|

|

2.7 |

0.5 |

0.7 |

3.9 |

-17.7 |

-18.3 |

-18.1 |

-0.9 |

0.7 |

0.4 |

|

4.75 12/38 |

149.856 |

1.848 |

-8.4 |

|

|

3.0 |

0.4 |

(0.0) |

3.3 |

-17.1 |

-17.8 |

-15.6 |

-0.3 |

0.9 |

0.4 |

|

4.25 9/39 |

142.085 |

1.866 |

-8.4 |

|

|

2.8 |

0.3 |

0.5 |

3.6 |

-18.7 |

-19.4 |

-17.6 |

-0.3 |

1.0 |

0.3 |

|

4.25 12/40 |

143.770 |

1.878 |

-8.6 |

|

|

2.8 |

0.2 |

0.2 |

3.1 |

-20.3 |

-20.9 |

-19.4 |

-0.2 |

0.9 |

0.2 |

|

4.5 12/42 |

151.506 |

1.887 |

-8.6 |

|

|

2.7 |

(0.0) |

0.2 |

2.8 |

-21.9 |

-22.5 |

-21.3 |

-0.3 |

0.9 |

0.1 |

|

3.25 1/44 |

127.490 |

1.901 |

-8.8 |

|

|

2.5 |

(0.1) |

0.5 |

2.9 |

-23.3 |

-23.9 |

-23.3 |

-0.1 |

0.9 |

0.1 |

|

3.5 1/45 |

133.580 |

1.899 |

-8.8 |

|

|

2.4 |

(0.2) |

0.2 |

2.4 |

-23.6 |

-24.3 |

-23.7 |

-0.1 |

0.9 |

(0.0) |

|

4.25 12/46 |

152.250 |

1.888 |

-8.3 |

|

|

2.4 |

(0.3) |

0.1 |

2.2 |

-23.4 |

-24.0 |

-23.5 |

-0.5 |

0.9 |

(0.1) |

|

1.5 7/47 |

91.600 |

1.873 |

-8.4 |

|

|

1.9 |

(0.4) |

0.4 |

1.9 |

-22.1 |

-22.5 |

-22.5 |

-0.4 |

0.5 |

(0.1) |

|

4.25 12/49 |

158.050 |

1.832 |

-8.5 |

|

|

2.1 |

(0.5) |

(0.2) |

1.5 |

-19.4 |

-19.9 |

-20.2 |

-0.2 |

0.7 |

(0.2) |

|

3.75 7/52 |

150.200 |

1.789 |

-8.2 |

|

|

1.9 |

(0.5) |

(0.0) |

1.4 |

-17.2 |

-17.6 |

-18.4 |

-0.5 |

0.7 |

(0.3) |

|

4.25 12/55 |

169.652 |

1.730 |

-8.2 |

|

|

1.7 |

(0.5) |

(0.1) |

1.1 |

-13.7 |

-14.0 |

-15.8 |

-0.5 |

0.6 |

(0.3) |

|

1.75 7/57 |

101.210 |

1.708 |

-8.8 |

|

|

1.4 |

(0.4) |

(0.1) |

0.8 |

-14.5 |

-14.8 |

-15.1 |

0.1 |

0.3 |

(0.2) |

|

4 1/60 |

169.380 |

1.685 |

-8.5 |

|

|

1.5 |

(0.4) |

(0.0) |

1.2 |

-12.2 |

-12.6 |

-15.1 |

-0.1 |

0.6 |

(0.1) |

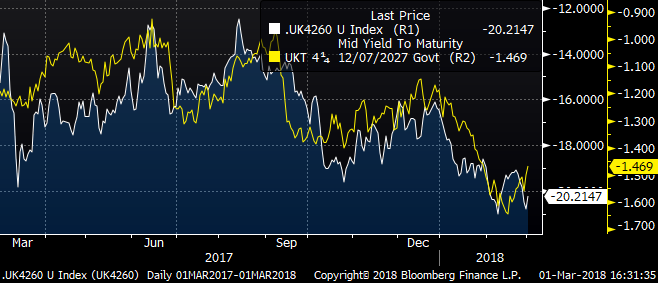

RISK: Over the last year there has been some correlation between 42s60s and Gilt futures (i.e. steepener has bullish bias):

White line – 42s60s

Yellow line – CTD 4q27 yield (inverted)

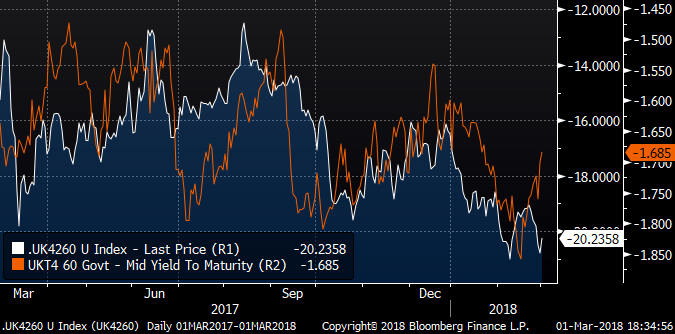

However the 42s60s curve looks too flat vs UKT 60s yield:

White line – 42s60s

Orange line – UKT 4 60 yield (inverted)

Jim Lockard

Founder / Managing Partner

![]() image001.jpg@01D21F14.8E7A1C60">

image001.jpg@01D21F14.8E7A1C60">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 -143 - 4172

Mobile: +44 (0) 7795-027-865

Email: jim.lockard@astorridge.com

Website: www.astorridge.com

This commentary was prepared by Jim Lockard, a Managing Partner at Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and it should be treated as a marketing communication even if it contains a research recommendation. A history of his commentary can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge does not engage in market making or proprietary trading, and has no position in any security discussed in this e-mail. The views in this e-mail are those of the author(s) and are subject to change.. Any recommendations contained herein reflect solely those of the author and were prepared independently of Astor Ridge or its affiliates. This publication does not constitute personal investment advice and may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate recommendations discussed herein. Actual investment returns may fluctuate as a result of changes in economic and market conditions (including market liquidity). Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by us is owned by us.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

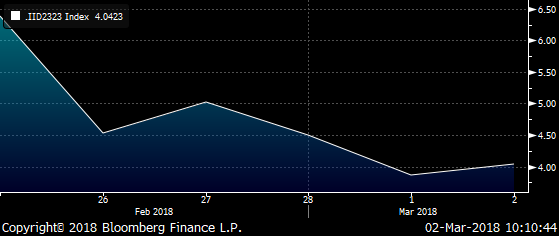

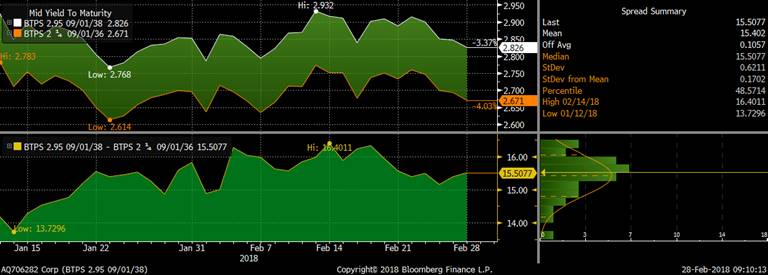

FW: Italy 5y anomaly, Trade Idea - James Rice @Astor Ridge

Italy Trade Idea –

Markets struggles to absorb new 5y Btps 0.95% Mar/01/2023

Trade

Sell Btps 0.65% 10/23 to Buy new 5y Btps 0.95% 3/23

Mechanics

- Sell Btps 0.65% 10/23 to buy New 5y Btps 03/01/2023

- 17% Hedge -OEA/+RXA

- Weighting +1/-1 in the Btp spread plus -0.17/+0.17 in the contract German Hedge

- Cix on OLD 5 YR Mar/15/23 (same coupon, maturity 2 weeks longer) history not available on new issue (trades approx +0.5bp over the old 5y)

100 * ((YIELD[BTPS 0.65 10/23 Corp] - YIELD[BTPS 0.95 3/15/23 Corp]) - 0.17 * (YIELD[DBR 0.25 2/27 Corp] - YIELD[OB176 Corp]))

- Cix on actual structure with new 5y issue

100 * ((YIELD[BTPS 0.65 10/23 Corp] - YIELD[BTPS 0.95 3/1/23 Corp]) - 0.17 * (YIELD[DBR 0.25 2/27 Corp] - YIELD[OB176 Corp]))

History

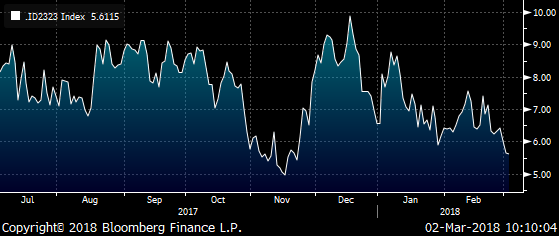

- Bloomberg Graph of CIX using Old 5y

- Using the actual new 5y that we propose…

Trade levels

- Current level @ +4.05bp (mid)

- Pay the Spread @ +4.1bp (50% size)

- Add @ +3bp

- Stop @ +1bp

- Final Target @ +7.5bp (approx. 4bp profit from average level)

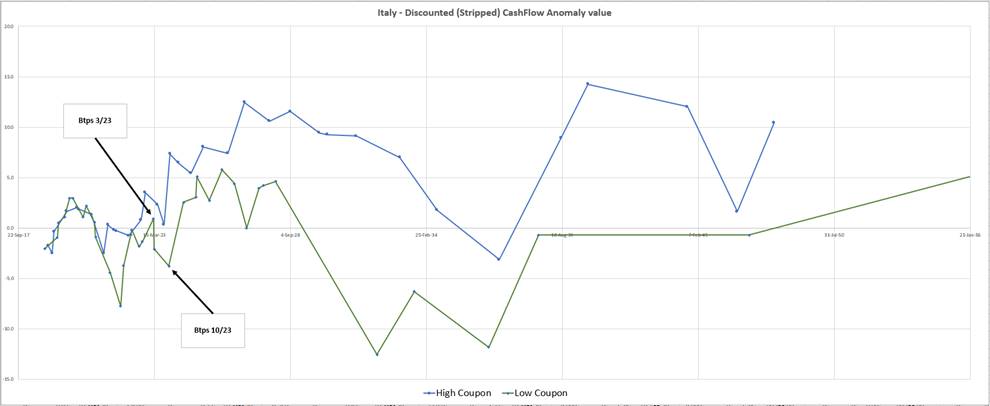

Relative Value vs Smoothed Btps Zero Curve

Relative Z-spreads

- Btps 10/23: +50.3bp, +96.1bp vs interp. German z-sprd curve

- Btps 3/23: +45.9bp, +92.8bp vs interp. German z-sprd curve

Relative Z-spreads to German curve -3.3bp

Rationale

- The new 5y 0.95% Mar/01/23 continues to trade cheaply as it seems not to have been well placed after Tuesday’s auction and the bond remains offered

- The theme we’re trying to pursue is to always shorten from longer into shorter tenors at near to, or similar anomaly value vs the stripped curve and as close to as flat as the German curve

- The best Roll and Carry resides in the 5yr sector – 5yrs roll toward the richer 3y segment

- With Italian elections looming this weekend and a possible hung parliament, this is a bearish structure on the Italy/Germany spread – however on relative Z-spread analysis this is only 3.3bp steeper in z-spread terms than the Italian curve – used to determine the stop

Carry & Roll

- Carry/3mo: -0.4bp (on the Italian side assuming 10bp spread)

- Roll/3mo: +0.6bp (Italian side)

- Carry and Roll on hedge/3mo: -0.3bp (assuming 10bp on hedges & 50% delta in hedge)

- Total Package Roll & Carry /3mo: -0.1bp

Rich/Cheap, Z-score – Bloomberg GOVY Cubic Spline Model, 3mo. History

- Btps 1.5% 10/23, Z-score -0.7

- Btps 0.95% Mar/01/2023, insignificant number of observations since first issue Tuesday

- old 7yr Btps 0.95% Mar/15/2023, Z-score -0.1

Risks

- A positive environment for the Italian credit (post-election) causes a narrowing of spreads and a flattening of Italy vs Germany

- The Btps 3/23 stays as a cheap issue on the curve

- The Btps 10/23 richens in terms of anomaly

Always love to hear your feedback

Will also be taking a look at analysing the futures rolls – let me know if you’d like to see that too

James

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

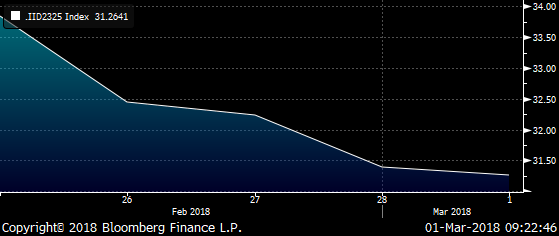

Italy 5s 7s steepener, Trade Idea - James Rice @Astor Ridge

Italy Trade Idea – Thursday, March 1st 2018

Absorbing Tuesday’s 5y supply, preparing for the new 7y in two weeks’ time

Sell 7y Btps 1.5% 6/25 to buy new 5y Btps 0.95% 3/23

Mechanics

- Sell Btps 1.5% 6/25 to buy New 5y Btps 03/01/2023

- 50% Hedge -OEA/+RXA

- Weighting +1/-1 in the spread plus -0.5/+0.5 in the contract German Hedge

- Cix on OLD 7 YR 03/23 (same coupon, maturity 2 weeks longer) history not available on new issue (trades approx +0.5bp over the old 7y)

100 * ((YIELD[BTPS 1.5 6/25 Corp] - YIELD[BTPS 0.95 3/15/23 Corp]) - 0.5 * (YIELD[DBR 0.25 2/27 Corp] - YIELD[OB176 Corp]))

- Cix on actual structure with new 7y issue

100 * ((YIELD[BTPS 1.5 6/25 Corp] - YIELD[BTPS 0.95 3/1/23 Corp]) - 0.5 * (YIELD[DBR 0.25 2/27 Corp] - YIELD[OB176 Corp]))

History

- Bloomberg Graph of CIX using Old 7y

- Using the actual new 5y that we propose…

Trade levels

- Current level @ +31.3bp (mid)

- Pay the Spread @ +30.5bp (50% size)

- Add @ +26.5bp

- Stop @ +24bp

- Final Target @ +34.25bp (approx. 3.7bp profit from first entry level)

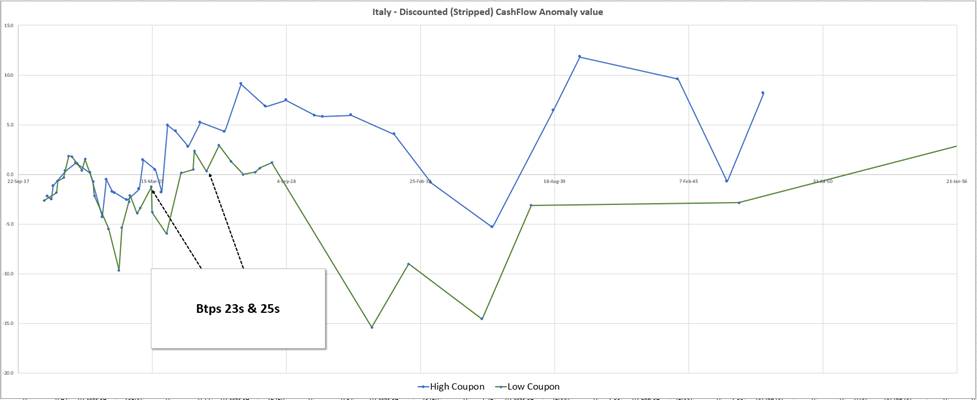

Relative Value vs Smoothed Btps Zero Curve

Rationale

- The new 5y 0.95% Mar/01/23 continues to trade cheaply as it seems not to have been well placed after Tuesday’s auction and the sector remains offered

- The theme we’re trying to pursue is to always shorten from longer into shorter tenors at near to, or similar anomaly value vs the stripped curve – (trade target is set for this to equate to less that give 1bp)

- The best Roll and Carry resides in the 5yr sector

- In two weeks’ time we have a new low coupon (expected given current yields), 7yr - Btps XX% May 2025 as per the Tesoro announcement Dec 21st 2017, so we expect the lower coupon 7 years may soften into this supply

- With Italian elections looming this weekend and a possible hung parliament, this is a fundamentally bearish structure on the Italy/Germany spread – a widening in the country spreads would also imply a relative steepening of the Italian curve vs the German hedge

Carry & Roll

- Carry/3mo: -0.7bp (on the Italian side assuming 10bp spread)

- Roll/3mo: +2.0bp (Italian side)

- Carry and Roll on hedge/3mo: -0.9bp (assuming 10bp on hedges & 50% delta in hedge)

- Total Package Roll & Carry /3mo: +0.4bp

Rich/Cheap – Bloomberg GOVY Cubic Spline Model, 3mo. History

- Btps 1.5% 6/25, z-score -0.5

- Btps 0.95% Mar/01/2023, insignificant number of observations since fist issue Tuesday

- For comparison the old 7yr Btps 0.95% Mar/15/2023, z-score -0.12

Risks

- A positive environment for the Italian credit (post-election) causes a narrowing of spreads and a flattening of Italy vs Germany

- The Btps 3/23 stays as a cheap issue on the curve

- The Btps 6/25 continues to stay rich on the curve

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

BOND and US CURVE MONTHLY UPDATE. Yields are topping out. I think its an OLD FASHIONED STOCKS DOWN BONDS UP. 28.2.2018.

BONDS UPDATE : US 5yr yield drop could be a BIG ONE.

1) Yields are close to breaching levels where we will see a MAJOR DROP (US 5yr and UK 10yr). ALL durations are stretched, quarterly, monthly, weekly and daily… this is RARE!

2) Looking at the previous Equity piece, European stocks look a LONGTERM failure thus I firmly believe this mean BONDS rally.

3) Germany 26’s bonds are basing finally.

4) UK yields have a LOFTY RSI and UKTI POISED to bounce, all eyes on a breach of 1.489 (10yr Gilts).

5) US 10 Breakevens have a LOFTY WEEKLY and DAILY RSI.

6) Nearly ALL US curves rejected the recent steepening BIAS at MAJOR MULTI YEAR 61.8% ret, the RSI’s remain low however. If the 61.8% ret’s are breached we steepen in a BIG WAY.

• ** HAPPY TO DISCUSS ANY CHARTS **

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4174

Mobile: +44 (0) 7980708683

Email: chris.williams@astorridge.com

Web: www.AstorRidge.com

• I provide our research notification below for your convenience:

•

• Research Unbundling:

•

• Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

•

• If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

•

•

•

• I also direct you to our disclaimer on our email footer:

• This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

•

• You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

•

• Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

• Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

• Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

• Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

• Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

•

•

• If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

•

• Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

•

• Many thanks,

•

• Chris

Trade Idea - France high coupon opportunity

France Trade Idea – Wednesday, February 28th 2018

High Coupon Structure –

Sell Frtr 3.5% Apr 26 to buy High Coupon Frtr 6% Oct 25 and OAT contracts

Mechanics

- Sell Frtr 3.5% 4/26

- Buy Frtr 6% 10/25 & OAT contracts (CTD Frtr 2.75% 10/27)

- Weighting: +1.5/-2/+0.5

- Cix: 200 * (YIELD[FRTR 3.5 4/26 Corp] - 0.75 * YIELD[FRTR 6 10/25 Corp] - 0.25 * YIELD[FRTR 2.75 10/27 Corp])

Trade levels

- Pay the Spread @ -3bp (50% size)

- Add @ -4.5bp

- Stop @ -7bp

- Final Target @ +4bp (approx. 8bp profit)

History

- Bloomberg Graph

- Relative Value vs Smoothed Frtr Zero Curve

Nota Bene:

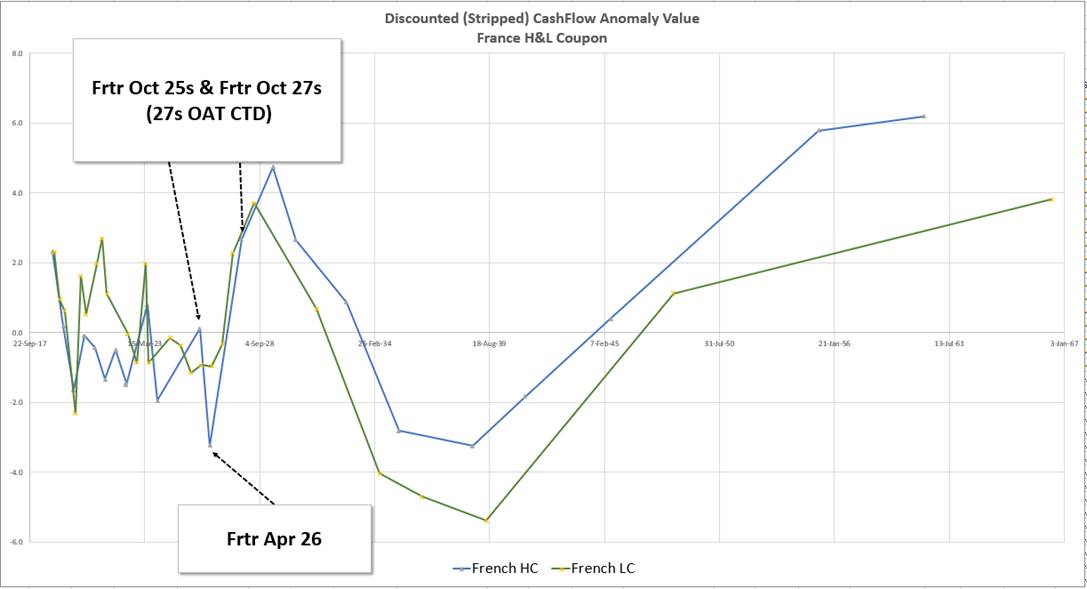

Under this analysis, we correctly see that the high coupons that appear rich in yield space, now appear cheap in discounted cashflow space, due to the steep curve. Implying this methodology is a valid way of explaining much of the confusing rich/cheap analysis when applied simply to yields rather than cashflows

Rationale

- The high coupon Frtr 3.25 % 4/26 have traded rich since their period as CTD to the OAT contract up until September 2017 (OATU7 – Eurex ), they actually sit on the high coupon curve (avg. coupon for the curve 2.5%)

- The bond then richened after falling out as CTD, it would appear that possibly were considerable macro shorts that failed to roll and the bond surfed into the richer, index matching 7yr segment

- Other high coupons have since cheapened on the yield curve (see graph on yield vs Average over last 6 months) possibly as a change in the dynamic of PSPP this year. Frtr apr 26s as a relatively high coupon bond are now exposed as rich on true anomaly value

- The Tresor are tapping similar maturity Frtr 0.5% 5/26 tomorrow, Thursday Mar 1st. In pursuit of an orderly market there is a chance of a tap of the Frtr 3.5% 4/26 going forward

Yields vs Average yield over last 6 months

- Below is the current yield on each bond, minus the average yield for the last 6 months (expressed in bp’s). It shows how the higher coupon issues, such as Frtr 6% Oct 25 & Frtr 5.5% Apr 29 have underperformed and we could possibly expect the same now for Frtr 4/26

Carry & Roll

- Carry -0.1bp /3mo (repo spread of 10bp on front leg & implied of -0.75% Jun contract)

- Roll 0.0bp /3mo

- Sum: C&R -0.1bp /3mo

Rich/Cheap – Bloomberg GOVY Cubic Spline Model, 3mo. History

- Frtr 3.25% 4/26, z-score -2.8

- Frtr 6% 10/25, z-score +2.0

- Frtr 2.75% 10/25, z-score -1.6

Risks

- The Frtr 3.25% 4/26 continue to trade rich as close the index modified duration

- The Frtr 4/26 get much richer on repo that mitigates their richness

- The Frtr 10/27 and 10/25 stay cheap on the curve, relatively

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

** WORTH A READ AS MONTH END LOOMING ..Equities A VERY conflicting set of charts, some QUARTERLY'S are TERMINAL on paper . 28.02.2018

• A VERY conflicting set of charts, some though are TERMINAL on paper.

• I.E. Quarterly CAC, FTSE and especially DAX, others like DOW and NASDAQ look positive.

• ** SEE DAX CHART PAGE 10! **

• MANY bounces have been VERY LAME.

• US stocks remain the most over bought and many have recovered MORE than 200% of the 2008-2009 correction.

• The DOW and S&P have major RSI dislocations spread across monthly, weekly and daily durations! This is a DANGEROUS combination.

• Some RSI’s surpass 1950 and 1980 levels.

• US stocks highlight the most CONCERN.

• ** HAPPY TO DISCUSS ANY CHARTS **

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4174

Mobile: +44 (0) 7980708683

Email: chris.williams@astorridge.com

Web: www.AstorRidge.com

• I provide our research notification below for your convenience:

•

• Research Unbundling:

•

• Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

•

• If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

•

•

•

• I also direct you to our disclaimer on our email footer:

• This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

•

• You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

•

• Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

• Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

• Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

• Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

• Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

•

•

• If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

•

• Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

•

• Many thanks,

•

• Chris

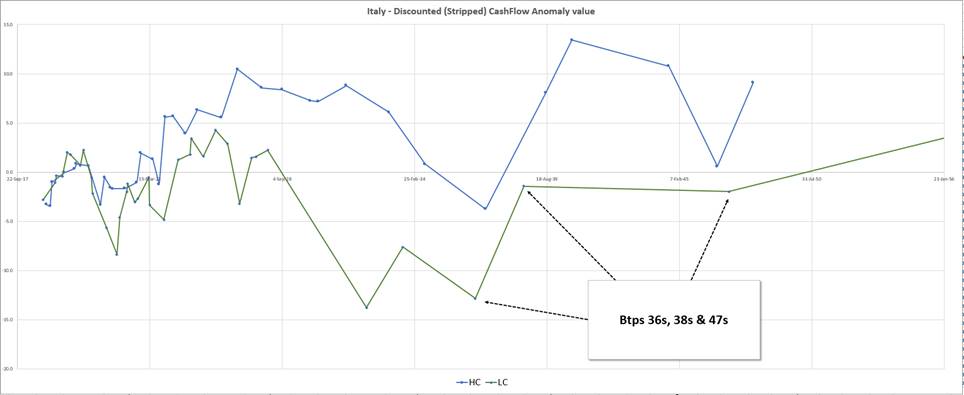

Trade Idea - Italy low coupon ahead of elections

Italy Trade Idea – Wednesday, February 28th 2018

Buy Italy 20y vs selling old 20y and old 30y, curve weighted

Mechanics

- Buy Btps 2.95% 9/38

- Sell Btps 2.25% 9/36 & Btps 2.7 3/47

- Weighting: -1.34/+2/-0.66

- Cix:

200 * (YIELD[BTPS 2.95 9/38 Corp] - 0.67 * YIELD[BTPS 2.25 9/36 Corp] - 0.33 * YIELD[BTPS 2.7 3/47 Corp])

Trade levels

- First Entry @+9.5bp (1/2 size)

- Second Entry @ +10.5bp (1/2 size)

- Target @+4bp

- Stop @+13bp

History

- Bloomberg graph – history limited to issue date of 9/38s on 9th January 2018

- Relative Value vs Smoothed Btp Zero Curve

Italian anomaly value using smooth zero curve – Green – Low coupons, Blue High Coupons.

Note that under this analysis we correctly see that the high coupons that appear rich in yield space now appear cheap in discounted cashflow space, due to the steep curve. Very rarely do we see a low coupon genuinely cheap to high coupons under this metric. That would imply the default option as approx zero cost relative to High coupons

Rationale

- The New btps 38s have struggled to place well in the curve as a new issue. They haven’t flattened vs Btps 36s (see spread graph), which trade richer, despite a generic flattening of 10s30s in European curve

- To capture value in low coupons, we have to constrain ourselves to low coupon issues, if we are at all concerned about a spread widening after the Italian elections (Sunday 4th March)

- The relative RV suggests that the pricing of the 38s is now at a point to be not too distant from the High coupon Btps 4% 2/37 – a loose boundary condition

- Now that we’ve had a couple of month’s pricing and with month end flows we could see cash being placed in the new Btps 38s

- Btps 47s were traditionally cheap (given their low coupon) but have now richened pulling away from the High coupon curve and provide an anchor (33% weighting) to give the trade curve balance

- The trade is weighting according to the shape of the fitted curve – such that, curvature is hedged and expected to increase in steeper curves and vice versa in a flatter one environment

Bloomberg Spread History

Carry & Roll

- Carry +0.4bp /3mo (repo spread of 10bp)

- Roll 0.0bp /3mo

- Sum: C&R +0.4bp /3mo

Risks

- The Btps 38s continues to trade cheaply as an ongoing tap issue

- The Sep36 and Mar47 – continue to richen as older issues with lower float

James Rice

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London ec4r 2su

US: 245 Park Ave 39th Fl, New York NY 10167

Office: +44 (0) 203 - 143 - 4178

Mobile: +44 (0) 754 - 011 - 7705

Email: James.Rice@AstorRidge.com

Web: www.AstorRidge.com

This marketing was prepared by James Rice, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

FX UPDATE AND EM BONDS : A quiet set of markets at the moment BUT we do remain in some VERY dislocated situations.. Awaiting a break on many fronts.

• A quiet set of markets at the moment BUT we do remain in some VERY dislocated situations.. Awaiting a break on many fronts.

• The USD INDEX is FINALLY BASING especially on the monthly chart.

• EUR USD continues to cause heartache around its KEY retracement SUPPORT 1.2167.

• EUR GBP weekly is COILING for a major move.

• USD JPY hitting SUPPORT at the 61.8% ret 106.54.

• USD ZAR is now struggling to hold major support.

![]() image001.jpg@01D21F13.B69A4950">

image001.jpg@01D21F13.B69A4950">

UK: 14-16 Dowgate Hill, London EC4R 2SU

US: 245 Park Ave, 39th Floor, NY, NY, 10167

Office: +44 (0) 203 143 4174

Mobile: +44 (0) 7980708683

Email: chris.williams@astorridge.com

Web: www.AstorRidge.com

• I provide our research notification below for your convenience:

•

• Research Unbundling:

•

• Astor Ridge does not provide independent research. We have no dedicated or paid strategists, research portals, or research subscriptions. However, you may receive unsolicited marketing communications from our Introducing Brokers from time to time, which may refer to specific trade recommendations. These recommendations are based solely on the opinion of the author, and are not official research recommendations of Astor Ridge.We have considered guidance from ESMA, and any written material from our Introducing Brokers that might fall within the scope of the rules will be provided for free, and made publicly available on our website, to any EU Investment firm that registers for it.

•

• If you are a MiFID firm and do not agree with our approach, and instead believe that you must pay for written commentary or trade recommendations, then Astor Ridge will accept payments determined by you.

•

•

•

• I also direct you to our disclaimer on our email footer:

• This marketing was prepared by Christopher Williams, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

•

• You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

•

• Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

• Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

• Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

• Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

• Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

•

•

• If there is anything else you require from us to continue receiving our market communications, or prefer a different medium for access (e.g. publicly available password protected access on the Astor Ridge website), please do let me know.

•

• Otherwise, if you are more comfortable to deem consent by simply acknowledging receipt of this email, and continuing our trading relationship under our updated terms of business below, without registering your disapproval, we are happy to proceed on that basis.

•

• Many thanks,

•

• Chris

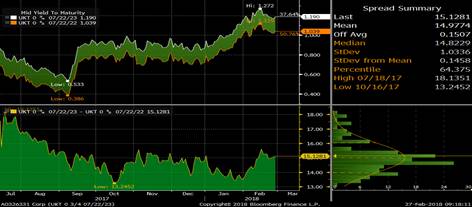

Gilts 1st March-£2.75bn 0.75% 2023 Auction-Cheap Issue On Many Angles.

The new month sees a re-opening of the very cheap 0.75% 7/2023s with a few different angles to buy this bond. The expression I would highlight is selling 0.5%/7/22s & 2.75% 2024s to buy 23s with a current pick up of around 8.5 bps this looks attractive into the supply & the BOE 5 18 cash reinvestment as the BOE currently hold less than £300 million of the 23s as we are up to around 75% for this issue before the DMO likely move to issue a new 2024 maturity probaly in July& the issue will go under 5 years maturity & benfit from the upcoming redmptions . Chart below : Entry 8.5bp .. Target:5bps.. Stop 11. ![]() Alternatively a trade out of h 22 into 7/23s @+15 bps looks worthwhile:

Alternatively a trade out of h 22 into 7/23s @+15 bps looks worthwhile:  Entry +15. Target +10.. Stop +18. or the steepening trade out of 2t 24 into t 23 dropping 6.4 bps.. Entry -6.3 Target:-11. Stop -4.

Entry +15. Target +10.. Stop +18. or the steepening trade out of 2t 24 into t 23 dropping 6.4 bps.. Entry -6.3 Target:-11. Stop -4.

This marketing was prepared by George Whitehead, a consultant with Astor Ridge. It is not appropriate to characterize this e-mail as independent investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a trade recommendation. A history of marketing materials and research reports can be provided upon request in compliance with the European Commission’s Market Abuse Regulation. Astor Ridge takes no proprietary trading risk, has no market making facilities, and has no position in any security we discuss in this e-mail. The views in this e-mail are those of the author(s) and are subject to change, and Astor Ridge has no obligation to update its opinions or the information in this publication. If this e-mail contains opinions or recommendations, those opinions or recommendations reflect solely and exclusively those of the author, and such opinions were prepared independently of any other interests, including those of Astor Ridge and/or its affiliates. This publication does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the those who receive it. The securities discussed herein may not be suitable for all investors. Astor Ridge recommends that investors independently evaluate each issuer, security or instrument discussed herein, and consult any independent advisors they believe necessary. The value of, and income from, any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

You should not use or disclose to any other person the contents of this e-mail or its attachments (if any), nor take copies. This e-mail is not a representation or warranty and is not intended nor should it be taken to create any legal relations, contractual or otherwise. This e-mail and any files transmitted with it are confidential, may be legally privileged, and are for the sole use of the intended recipient. Copyright in this e-mail and any accompanying document created by Astor Ridge LLP is owned by Astor Ridge LLP.

Astor Ridge LLP is regulated by the Financial Conduct Authority (FCA): Registration Number 579287

Astor Ridge LLP is Registered in England and Wales with Companies House: Registration Number OC372185

Astor Ridge NA LLP is a member of FINRA/SIPC: CRD Number 282626

Astor Ridge NA LLP is a member of the National Futures Association (NFA): Firm ID Number 0499303

Astor Ridge NA LLP is Registered in England and Wales with Companies House: Registration Number OC401796

<< "The Past Is The Future Back To Basics" 02031434182-www.astorridge.com >>